Advertisement

- Canada

- /

- Oil and Gas

- /

- TSXV:ORC.B

Orca Energy (TSXV:ORC.B) Profit Margin Jumps to 14.9%, Raising Questions on Earnings Durability

Simply Wall St

Reviewed by Simply Wall St

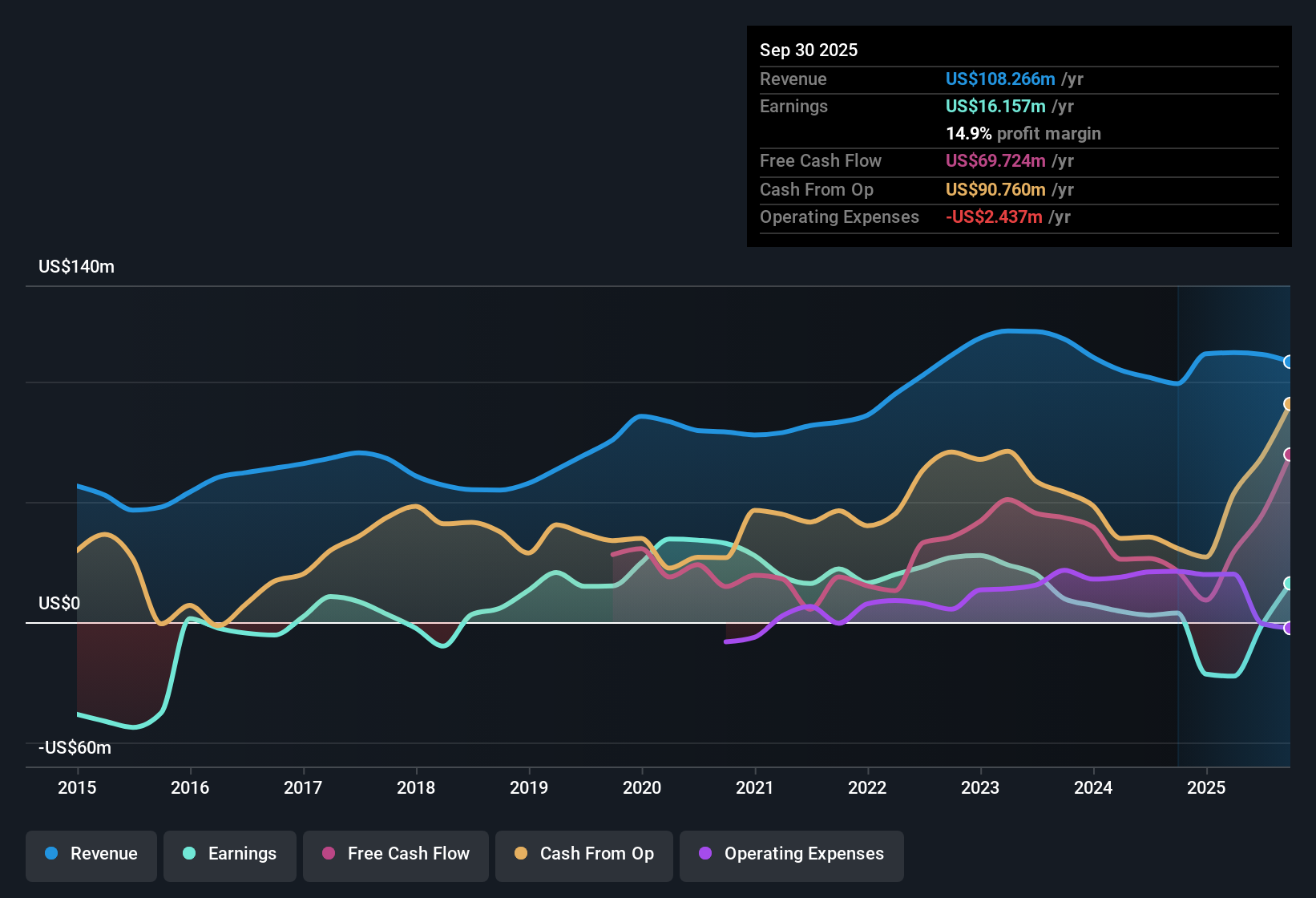

Orca Energy Group (TSXV:ORC.B) posted Q3 2025 financial results with total revenue of $21.7 million and EPS of $0.99. Looking at recent trends, the company saw revenue slip from $24.8 million in Q3 2024, though EPS moved up from $0.11. For investors, profit margins remain in focus as the overall results reflect a period of shifting earnings power.

See our full analysis for Orca Energy Group.Next, we will examine how the latest numbers compare to prevailing investor narratives and where expectations may be redefined.

Curious how numbers become stories that shape markets? Explore Community Narratives

Profit Margin Jumps to 14.9% for the Year

- Trailing twelve-month data shows Orca Energy Group’s net profit margin improved to 14.9%, up from 3.8% the prior year.

- Despite a record period of profit growth at 324.6% over the last twelve months, analysts draw attention to the unusual spike compared to the five-year average, with prior earnings having fallen 40.4% per year.

- This sharp uptick creates a notable contrast with the company’s longer trend of shrinking profits, raising questions about how sustainable this momentum is.

- The major swing in margins and earnings is largely attributable to a single one-off loss of $48.4 million earlier in the period, underlying why the durability of these results remains up for debate.

Shares Priced 28% Below DCF Fair Value

- The current share price of $3.35 trades at a 28.1% discount to the company’s DCF fair value estimate of $4.66, suggesting an apparent value opportunity based on discounted cash flow analysis.

- Market opinion notes that the low Price-To-Earnings ratio of 2.9x, well below the Canadian oil and gas industry average of 14.8x, points to a valuation gap, but critics caution that this may not fully reflect persistent profitability volatility and an unstable dividend history.

- While the company’s price appears attractive using traditional ratios, the presence of non-recurring items and uneven earnings complicates the investment case and could justify the market’s discounted pricing.

- Investors debating the valuation will want to see whether future results show more consistency without the noise of one-time impacts.

Revenue Shrink Continues Despite Price Stability

- Quarterly revenue has declined from $25.39 million in Q1 2025 to $21.75 million in Q3 2025, while the realized gas price held steady near $5.08 over recent quarters.

- The prevailing market perspective notes that, although Orca’s sales pricing environment stayed strong, ongoing revenue declines reinforce the cautious view that growth headwinds remain, even during periods when profit metrics look favorable.

- The flat realized gas price highlights that revenue weakness is not driven by commodity pricing, but potentially by volumes or contract dynamics, suggesting limited upside absent new catalysts.

- Consensus narrative points out that without a rebound in revenue growth or major shifts in operating trends, recent margin improvements could prove difficult to sustain over the longer term.

Orca’s latest numbers challenge expectations. See how community narratives balance the group’s rebound against ongoing risks in the full consensus narrative. 📊 Read the full Orca Energy Group Consensus Narrative.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Orca Energy Group's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

Despite the recent rebound in profit margin, Orca Energy Group faces ongoing revenue declines and volatile earnings. These factors raise questions about long-term stability.

If you’re looking for companies that consistently expand their revenue and profits year after year, check out stable growth stocks screener (2075 results) for steady performers even when broader trends shift.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSXV:ORC.B

Orca Energy Group

Engages in the exploration, development, production, and supply of petroleum and natural gas to the power and industrial sectors in Tanzania.

Excellent balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

29 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

137 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7924.0% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative