- Canada

- /

- Capital Markets

- /

- TSX:SEC

Undiscovered Canadian Gems Including Senvest Capital And Two Promising Small Caps

Reviewed by Simply Wall St

As we navigate the evolving landscape of 2025, marked by shifts in political regimes and central-bank policies impacting bond yields, the Canadian market presents unique opportunities for investors seeking to balance growth and value investments. In this context, identifying promising small-cap stocks like Senvest Capital and others can be pivotal; such stocks often stand out due to their strong fundamentals and potential for resilience amid broader market uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| TWC Enterprises | 6.24% | 12.63% | 23.89% | ★★★★★★ |

| Reconnaissance Energy Africa | NA | 9.16% | 15.11% | ★★★★★★ |

| Minsud Resources | NA | nan | -29.01% | ★★★★★★ |

| Maxim Power | 25.01% | 12.79% | 17.14% | ★★★★★☆ |

| Mako Mining | 10.21% | 38.44% | 58.78% | ★★★★★☆ |

| Grown Rogue International | 24.92% | 19.37% | 188.55% | ★★★★★☆ |

| Corby Spirit and Wine | 65.79% | 7.46% | -5.76% | ★★★★☆☆ |

| Petrus Resources | 19.44% | 17.20% | 46.03% | ★★★★☆☆ |

| Queen's Road Capital Investment | 8.87% | 13.76% | 16.18% | ★★★★☆☆ |

| DIRTT Environmental Solutions | 58.73% | -5.34% | -5.43% | ★★★★☆☆ |

Let's dive into some prime choices out of from the screener.

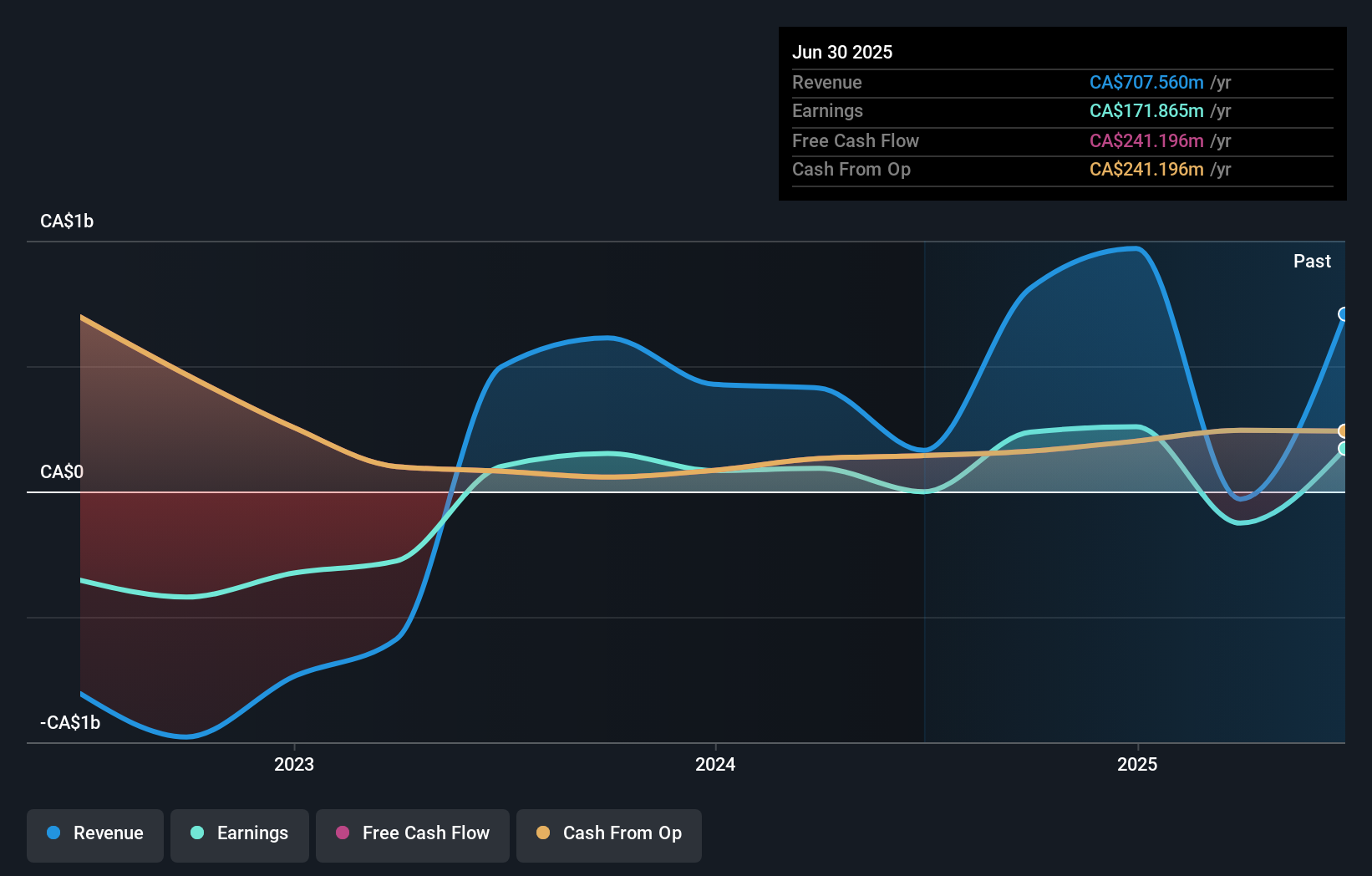

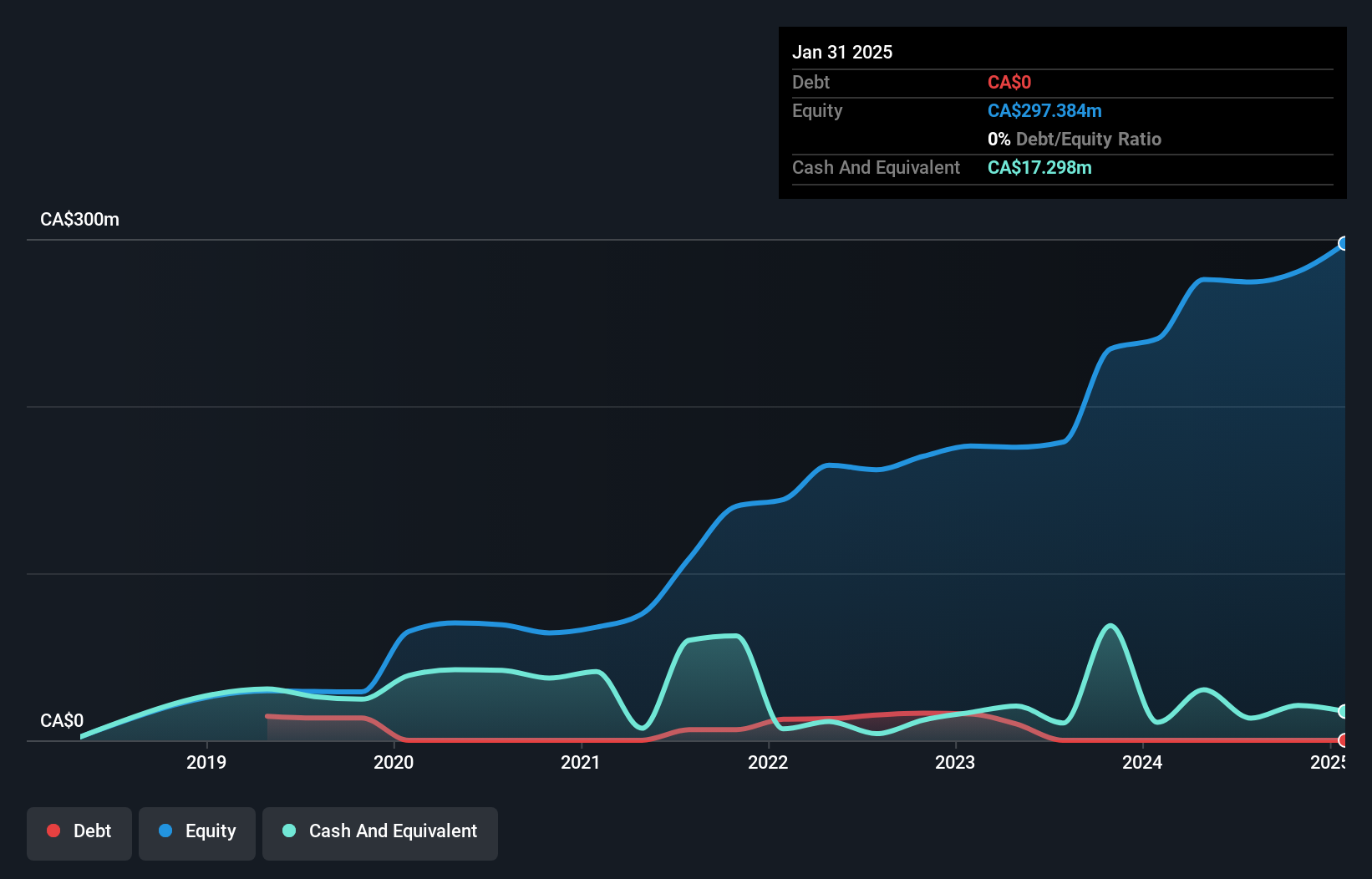

Senvest Capital (TSX:SEC)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Senvest Capital Inc., headquartered in Montreal, Quebec, Canada, is a privately owned investment manager with a market cap of CA$934.61 million.

Operations: Senvest Capital generates revenue primarily through the management of its own investments and those of the funds, amounting to CA$810.05 million. The financial performance is reflected in its market capitalization, which stands at CA$934.61 million.

Senvest Capital, a small but intriguing player in the Canadian market, has shown impressive financial resilience and growth. Its interest payments are well covered by EBIT at 8.2 times, indicating strong earnings quality. Over the past year, earnings surged by 56%, outpacing the industry average of 7.2%. The price-to-earnings ratio stands at a compelling 3.9x against the Canadian market's 14.7x average, suggesting potential value for investors. Recent buybacks include repurchasing 25,400 shares for CAD 8.44 million and another tranche of 39,400 shares for CAD 12.08 million in total buybacks this year under its ongoing program.

- Click here to discover the nuances of Senvest Capital with our detailed analytical health report.

Explore historical data to track Senvest Capital's performance over time in our Past section.

Uranium Royalty (TSX:URC)

Simply Wall St Value Rating: ★★★★★★

Overview: Uranium Royalty Corp. operates as a pure-play uranium royalty company with a market cap of CA$432.84 million.

Operations: The company generates revenue primarily through acquiring and assembling a portfolio of royalties, with reported earnings of CA$38.29 million.

Uranium Royalty Corp. stands out with its debt-free status, a notable shift from a 46.2% debt-to-equity ratio five years ago. The company's earnings surged by 259.5% over the past year, significantly outperforming the Oil and Gas industry's -20.2%. Despite this growth, shareholders faced dilution recently, while the stock trades at 63.7% below estimated fair value, offering potential upside for investors seeking undervalued opportunities in uranium royalties. Recent strategic moves include acquiring a royalty interest in Saskatchewan's Millennium and Cree Extension Uranium Projects for $6 million CAD, enhancing its foothold in one of the world's top mining regions.

Westshore Terminals Investment (TSX:WTE)

Simply Wall St Value Rating: ★★★★★☆

Overview: Westshore Terminals Investment Corporation operates a coal storage and unloading/loading terminal at Roberts Bank, British Columbia, with a market capitalization of CA$1.36 billion.

Operations: Westshore generates revenue primarily from its transportation infrastructure segment, amounting to CA$382.57 million. The company's market capitalization stands at CA$1.36 billion.

Westshore Terminals Investment, a player in the Canadian infrastructure scene, is debt-free and boasts a price-to-earnings ratio of 13x, which is below the market average of 14.5x. Over the past year, its earnings have grown by 11.1%, outpacing the infrastructure industry’s growth rate of 9.3%. Recent financials show third-quarter revenue at C$103 million with net income at C$34 million, slightly up from last year’s figures. The company also repurchased over 675,000 shares for C$15.56 million in recent months and declared a dividend of C$0.375 per share for early January payout to shareholders.

Taking Advantage

- Click here to access our complete index of 47 TSX Undiscovered Gems With Strong Fundamentals.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:SEC

Senvest Capital

A privately owned investment manager was founded in 1968 and is headquartered in Montreal, Quebec, Canada.

Solid track record with adequate balance sheet.