Advertisement

- Canada

- /

- Energy Services

- /

- TSX:TVK

TerraVest Industries (TSE:TVK) Takes On Some Risk With Its Use Of Debt

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We note that TerraVest Industries Inc. (TSE:TVK) does have debt on its balance sheet. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for TerraVest Industries

What Is TerraVest Industries's Debt?

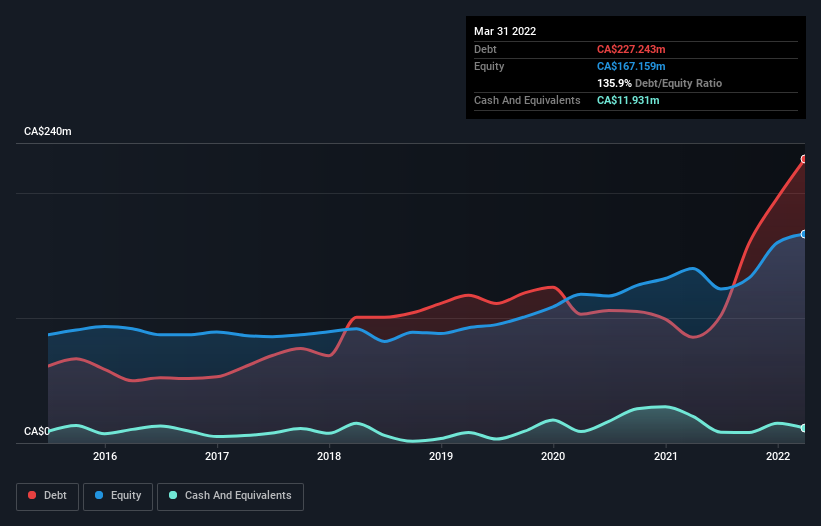

You can click the graphic below for the historical numbers, but it shows that as of March 2022 TerraVest Industries had CA$227.2m of debt, an increase on CA$84.6m, over one year. However, it also had CA$11.9m in cash, and so its net debt is CA$215.3m.

How Healthy Is TerraVest Industries' Balance Sheet?

The latest balance sheet data shows that TerraVest Industries had liabilities of CA$142.7m due within a year, and liabilities of CA$225.3m falling due after that. Offsetting this, it had CA$11.9m in cash and CA$90.5m in receivables that were due within 12 months. So its liabilities total CA$265.6m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of CA$430.3m, so it does suggest shareholders should keep an eye on TerraVest Industries' use of debt. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With net debt to EBITDA of 3.3 TerraVest Industries has a fairly noticeable amount of debt. But the high interest coverage of 7.1 suggests it can easily service that debt. Importantly TerraVest Industries's EBIT was essentially flat over the last twelve months. Ideally it can diminish its debt load by kick-starting earnings growth. There's no doubt that we learn most about debt from the balance sheet. But it is TerraVest Industries's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we always check how much of that EBIT is translated into free cash flow. During the last three years, TerraVest Industries produced sturdy free cash flow equating to 52% of its EBIT, about what we'd expect. This cold hard cash means it can reduce its debt when it wants to.

Our View

Both TerraVest Industries's net debt to EBITDA and its level of total liabilities were discouraging. At least its interest cover gives us reason to be optimistic. Looking at all the angles mentioned above, it does seem to us that TerraVest Industries is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that TerraVest Industries is showing 2 warning signs in our investment analysis , and 1 of those is a bit concerning...

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if TerraVest Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:TVK

TerraVest Industries

Manufactures and sells goods and services to agriculture, mining, energy production and distribution, chemical, utilities, transportation and construction, and other markets in Canada, the United States, and internationally.

High growth potential with solid track record.

Market Insights

Advertisement

Community Narratives

Pole position to benefit from GENIUS Act

Fair Value US$233.04|58.8% undervalued

CH

Community Contributor

IREN will transform from bitcoin miner to leader in AI infrastructure

Fair Value US$21.48|17.5% undervalued

KA

Community Contributor

Behind the Assay: XRF Scientific’s Role in Modern Mining Economics

Fair Value AU$2.10|2.4% undervalued

RO

Community Contributor