Advertisement

- Canada

- /

- Diversified Financial

- /

- TSX:PAY

September 2024's Top TSX Growth Companies With High Insider Ownership

Simply Wall St

Reviewed by Simply Wall St

In the last week, the Canadian market has been flat, with the Healthcare sector experiencing a 5.0% drop. Over the past 12 months, however, the market has risen by 13%, and earnings are forecast to grow by 15% annually. In this context, growth companies with high insider ownership can be particularly attractive as they often signal strong confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In Canada

| Name | Insider Ownership | Earnings Growth |

| Vox Royalty (TSX:VOXR) | 12.6% | 70.7% |

| Allied Gold (TSX:AAUC) | 22.5% | 73.6% |

| Almonty Industries (TSX:AII) | 17.7% | 117.6% |

| goeasy (TSX:GSY) | 21.3% | 17.1% |

| Alvopetro Energy (TSXV:ALV) | 19.4% | 72.4% |

| Propel Holdings (TSX:PRL) | 40% | 37.2% |

| Ivanhoe Mines (TSX:IVN) | 12.4% | 72.4% |

| Medicenna Therapeutics (TSX:MDNA) | 15.4% | 57.2% |

| Alpha Cognition (CNSX:ACOG) | 17.9% | 69.5% |

| ROK Resources (TSXV:ROK) | 16.6% | 161.8% |

Let's review some notable picks from our screened stocks.

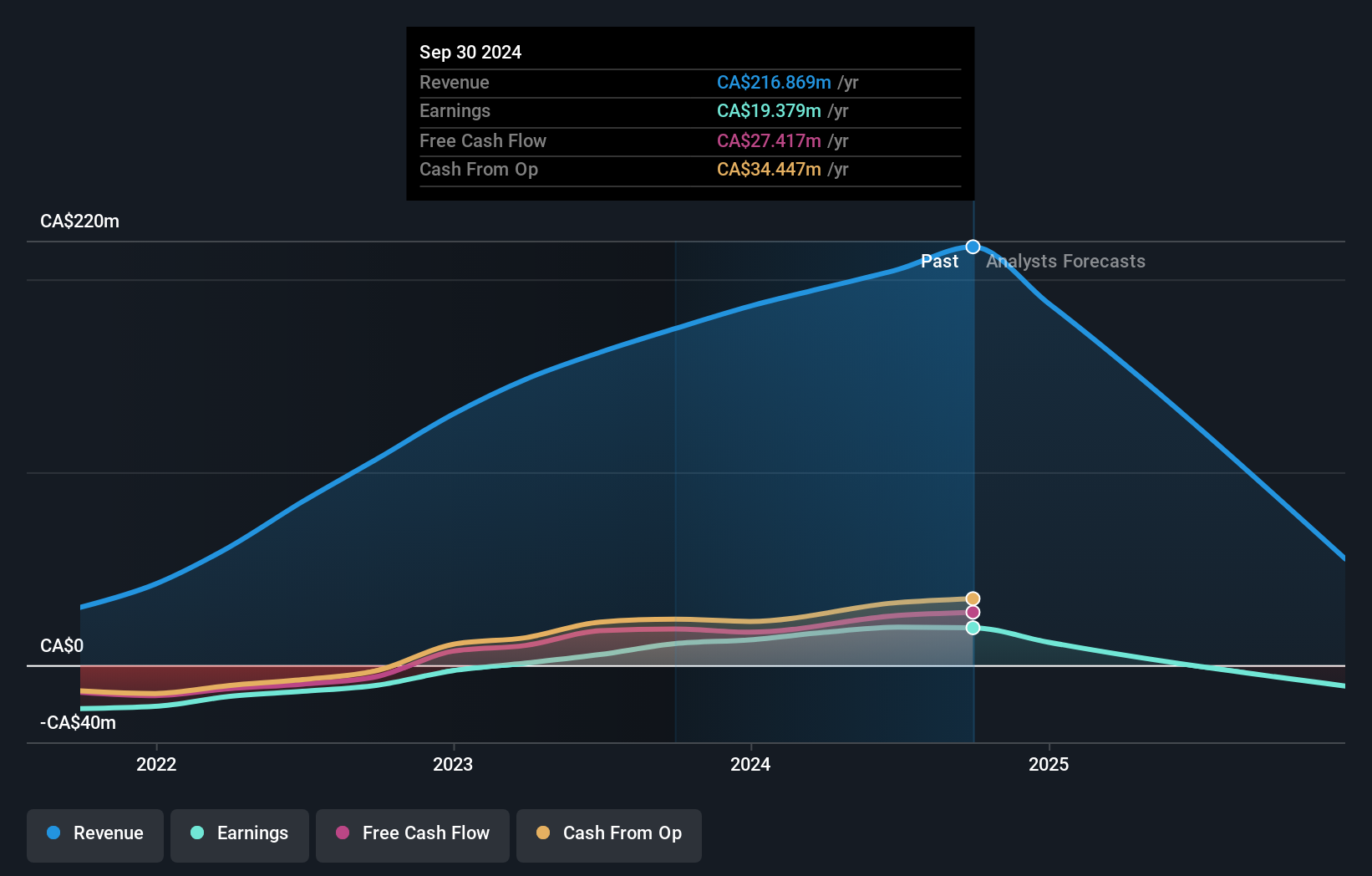

Payfare (TSX:PAY)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Payfare Inc. is a financial technology company that offers instant payout and digital banking solutions to gig economy workers in Canada, the United States, and Mexico, with a market cap of CA$417.92 million.

Operations: Revenue from Internet Software & Services amounts to CA$205.11 million.

Insider Ownership: 14.7%

Revenue Growth Forecast: 23.1% p.a.

Payfare Inc. demonstrates strong growth potential with significant insider ownership, evidenced by a 259.9% earnings increase over the past year and revenue forecasted to grow at 23.1% annually, outpacing the Canadian market. Recent product enhancements with Lyft Direct, including high-yield savings and cashback rewards, bolster its appeal among gig economy workers. Additionally, Payfare's Q2 2024 earnings showcased robust performance with CAD 55.99 million in sales and CAD 4.9 million net income, reflecting solid financial health and strategic expansion initiatives.

- Dive into the specifics of Payfare here with our thorough growth forecast report.

- Our valuation report here indicates Payfare may be overvalued.

Propel Holdings (TSX:PRL)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Propel Holdings Inc. operates as a financial technology company with a market cap of CA$1.04 billion.

Operations: Propel Holdings generates revenue of $382.44 million by providing lending-related services to borrowers, banks, and other institutions.

Insider Ownership: 40%

Revenue Growth Forecast: 23.5% p.a.

Propel Holdings showcases strong growth potential with high insider ownership, evidenced by a 74% earnings increase over the past year and forecasted annual earnings growth of 37.25%. Recent financial results highlight this momentum, with Q2 sales rising to US$106.75 million from US$71.69 million year-over-year and net income doubling to US$11.12 million. Despite substantial insider selling in the last quarter, Propel's revenue is projected to grow faster than the Canadian market at 23.5% annually.

- Delve into the full analysis future growth report here for a deeper understanding of Propel Holdings.

- The analysis detailed in our Propel Holdings valuation report hints at an inflated share price compared to its estimated value.

TerraVest Industries (TSX:TVK)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: TerraVest Industries Inc. manufactures and sells goods and services to the energy, agriculture, mining, transportation, and other markets in Canada and the United States with a market cap of CA$1.89 billion.

Operations: The company's revenue segments include Service (CA$201.78 million), Processing Equipment (CA$117.58 million), Compressed Gas Equipment (CA$243.77 million), and HVAC and Containment Equipment (CA$292.90 million).

Insider Ownership: 21.9%

Revenue Growth Forecast: 12.2% p.a.

TerraVest Industries demonstrates significant growth potential with high insider ownership, despite recent substantial insider selling. The company has forecasted annual earnings growth of 21.06%, outpacing the Canadian market's 15.4%. Recent financials show robust performance, with Q3 revenue at C$238.13 million and net income at C$11.92 million, up from C$150.36 million and C$7.97 million respectively a year ago. However, shareholders faced dilution over the past year and the company carries a high level of debt.

- Click to explore a detailed breakdown of our findings in TerraVest Industries' earnings growth report.

- In light of our recent valuation report, it seems possible that TerraVest Industries is trading beyond its estimated value.

Key Takeaways

- Dive into all 37 of the Fast Growing TSX Companies With High Insider Ownership we have identified here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:PAY

Payfare

A financial technology company, provides instant payout and digital banking solutions to gig economy workers in Canada, the United States, and Mexico.

Outstanding track record with flawless balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor