Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that Fission Uranium Corp. (TSE:FCU) does use debt in its business. But should shareholders be worried about its use of debt?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Fission Uranium

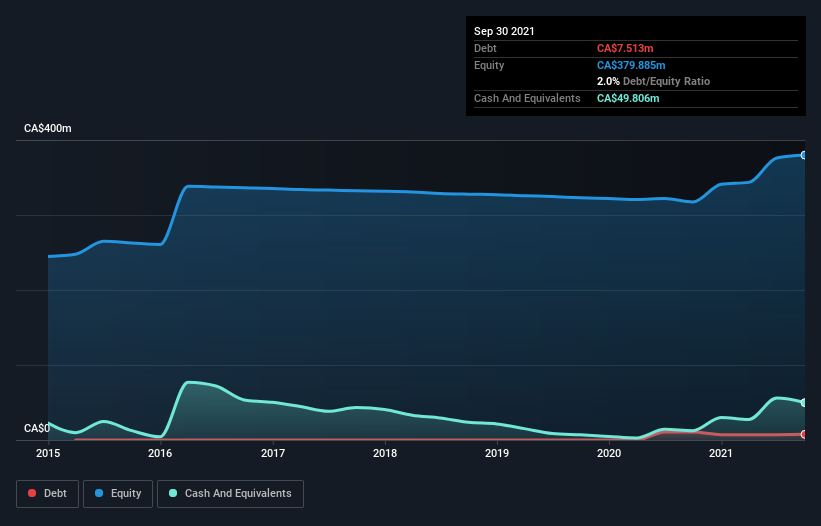

What Is Fission Uranium's Net Debt?

The image below, which you can click on for greater detail, shows that Fission Uranium had debt of CA$7.51m at the end of September 2021, a reduction from CA$10.6m over a year. However, it does have CA$49.8m in cash offsetting this, leading to net cash of CA$42.3m.

How Strong Is Fission Uranium's Balance Sheet?

The latest balance sheet data shows that Fission Uranium had liabilities of CA$2.06m due within a year, and liabilities of CA$10.2m falling due after that. On the other hand, it had cash of CA$49.8m and CA$491.0k worth of receivables due within a year. So it actually has CA$38.0m more liquid assets than total liabilities.

This surplus suggests that Fission Uranium has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that Fission Uranium has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Fission Uranium can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Given its lack of meaningful operating revenue, Fission Uranium shareholders no doubt hope it can fund itself until it can sell some combustibles.

So How Risky Is Fission Uranium?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And the fact is that over the last twelve months Fission Uranium lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of CA$22m and booked a CA$9.7m accounting loss. With only CA$42.3m on the balance sheet, it would appear that its going to need to raise capital again soon. Even though its balance sheet seems sufficiently liquid, debt always makes us a little nervous if a company doesn't produce free cash flow regularly. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 5 warning signs for Fission Uranium (1 is a bit unpleasant!) that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:FCU

Fission Uranium

Engages in the acquisition, exploration, and development of uranium resource properties in Canada.

Flawless balance sheet low.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor