Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:ERF

The Compensation For Enerplus Corporation's (TSE:ERF) CEO Looks Deserved And Here's Why

Key Insights

- Enerplus will host its Annual General Meeting on 4th of May

- Total pay for CEO Ian Dundas includes US$504.5k salary

- Total compensation is similar to the industry average

- Enerplus' EPS grew by 100% over the past three years while total shareholder return over the past three years was 454%

We have been pretty impressed with the performance at Enerplus Corporation (TSE:ERF) recently and CEO Ian Dundas deserves a mention for their role in it. The pleasing results would be something shareholders would keep in mind at the upcoming AGM on 4th of May. This would also be a chance for them to hear the board review the financial results, discuss future company strategy and vote on any resolutions such as executive remuneration. We think the CEO has done a pretty decent job and we discuss why the CEO compensation is appropriate.

Check out our latest analysis for Enerplus

How Does Total Compensation For Ian Dundas Compare With Other Companies In The Industry?

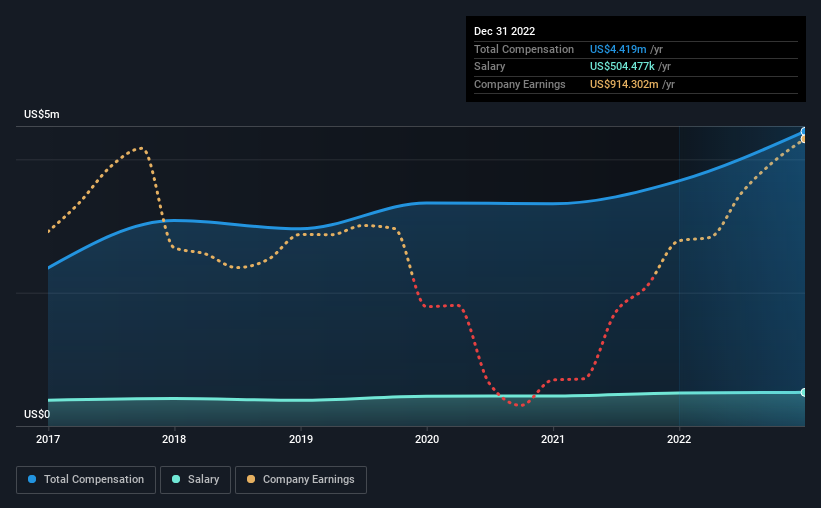

According to our data, Enerplus Corporation has a market capitalization of CA$4.2b, and paid its CEO total annual compensation worth US$4.4m over the year to December 2022. That's a notable increase of 20% on last year. While we always look at total compensation first, our analysis shows that the salary component is less, at US$504k.

For comparison, other companies in the Canadian Oil and Gas industry with market capitalizations ranging between CA$2.7b and CA$8.7b had a median total CEO compensation of US$3.5m. This suggests that Enerplus remunerates its CEO largely in line with the industry average. Furthermore, Ian Dundas directly owns CA$6.7m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | US$504k | US$496k | 11% |

| Other | US$3.9m | US$3.2m | 89% |

| Total Compensation | US$4.4m | US$3.7m | 100% |

On an industry level, roughly 36% of total compensation represents salary and 64% is other remuneration. It's interesting to note that Enerplus allocates a smaller portion of compensation to salary in comparison to the broader industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Enerplus Corporation's Growth Numbers

Over the past three years, Enerplus Corporation has seen its earnings per share (EPS) grow by 100% per year. It achieved revenue growth of 58% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's great to see that revenue growth is strong, too. These metrics suggest the business is growing strongly. Historical performance can sometimes be a good indicator on what's coming up next but if you want to peer into the company's future you might be interested in this free visualization of analyst forecasts.

Has Enerplus Corporation Been A Good Investment?

Most shareholders would probably be pleased with Enerplus Corporation for providing a total return of 454% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Seeing that the company has put in a relatively good performance, the CEO remuneration policy may not be the focus at the AGM. In fact, strategic decisions that could impact the future of the business might be a far more interesting topic for investors as it would help them set their longer-term expectations.

Whatever your view on compensation, you might want to check if insiders are buying or selling Enerplus shares (free trial).

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Enerplus might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:ERF

Enerplus

Explores and develops crude oil and natural gas in the United States.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.9% undervalued

TO

Community Contributor