Advertisement

- Canada

- /

- Oil and Gas

- /

- TSX:CCO

Will Cameco’s (TSX:CCO) Nuclear Platform Push at Resourcing Tomorrow Change Its Investment Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- Cameco Corporation recently presented at the Mines and Money @ Resourcing Tomorrow conference in London, with Global Managing Director Dominic Kieran outlining the company’s role across uranium supply, fuel services, and Westinghouse-linked technologies.

- This appearance highlighted how Cameco is increasingly positioned as a multi-layered nuclear energy supplier, tying together long-duration reactor demand, fuel security, and value-added services within one integrated platform.

- We’ll now explore how Cameco’s expanding role across uranium, fuel services, and Westinghouse exposure could reshape its existing investment narrative.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Cameco Investment Narrative Recap

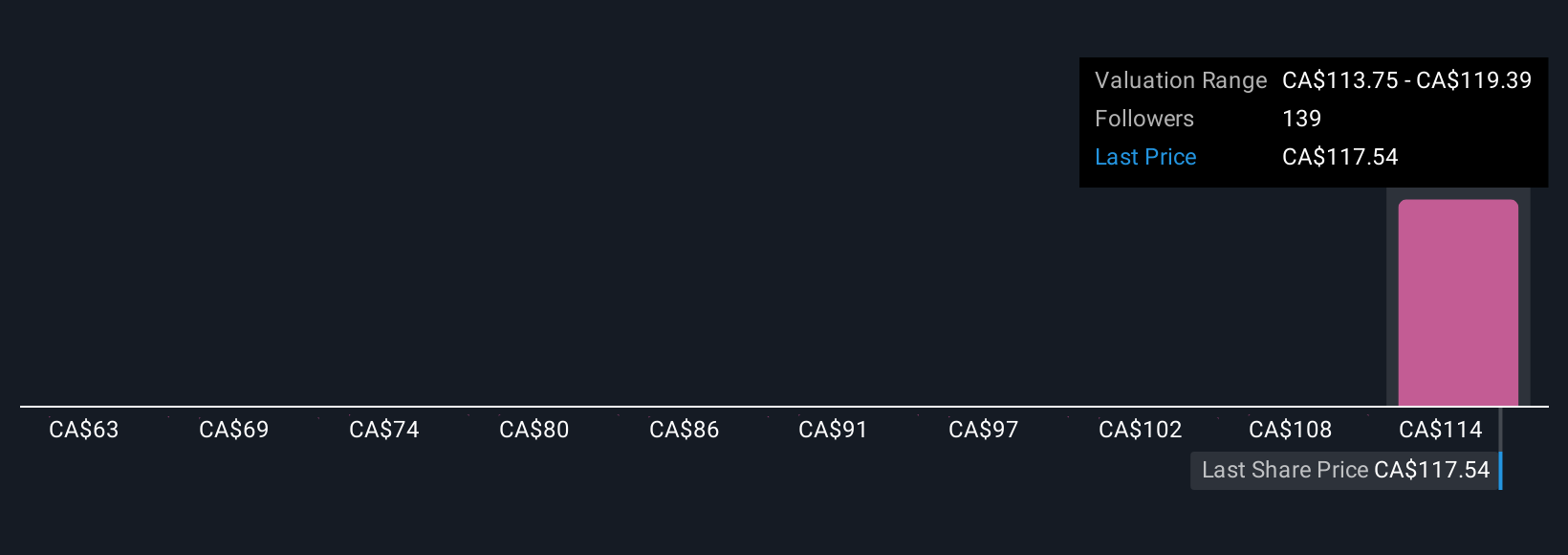

To own Cameco, you need to believe nuclear power will remain central to long term energy plans and that utilities will keep prioritizing secure Western fuel supply. The London Mines and Money presentation reinforces Cameco’s role across uranium, fuel services and Westinghouse, but does not materially change the near term picture, where the key catalyst is renewed long term utility contracting and the biggest risk remains delays or cancellations in new reactor final investment decisions.

Among recent announcements, the 5 November 2025 update on uranium and fuel services production feels most relevant here, because it shows how Cameco’s integrated platform is already translating into multiple operating “legs.” While nine month uranium volumes were lower year over year, fuel services output edged higher, underlining how a broader nuclear services mix could help soften the impact of any timing-related swings in uranium demand or pricing as the contracting cycle evolves.

Yet even with this broader footprint, investors should be aware that project delays and slower reactor approvals could still...

Read the full narrative on Cameco (it's free!)

Cameco’s narrative projects CA$3.9 billion revenue and CA$1.2 billion earnings by 2028. This requires 2.6% yearly revenue growth and an earnings increase of about CA$666 million from CA$533.6 million today.

Uncover how Cameco's forecasts yield a CA$151.75 fair value, a 20% upside to its current price.

Exploring Other Perspectives

Fourteen fair value estimates from the Simply Wall St Community span roughly CA$50.81 to CA$151.75, showing how widely individual views can differ. Against that backdrop, the big swing factor many of these community members are weighing is whether delayed nuclear reactor FIDs eventually convert into firm projects, or keep revenue and earnings under pressure for longer.

Explore 14 other fair value estimates on Cameco - why the stock might be worth as much as 20% more than the current price!

Build Your Own Cameco Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Cameco research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Cameco research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Cameco's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are the new gold rush. Find out which 36 stocks are leading the charge.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CCO

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative