Advertisement

- Canada

- /

- Diversified Financial

- /

- TSX:TF

TSX Stocks Investors May Be Undervaluing In August 2025

Simply Wall St

Reviewed by Simply Wall St

Amidst a backdrop of shifting monetary policies and economic uncertainties, both the U.S. Federal Reserve and the Bank of Canada are navigating complex landscapes with interest rate adjustments aimed at balancing inflation and labor market dynamics. As Canadian investors assess these evolving conditions, identifying undervalued stocks on the TSX could present opportunities for growth, particularly in sectors resilient to economic fluctuations.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Vitalhub (TSX:VHI) | CA$12.75 | CA$20.83 | 38.8% |

| Versamet Royalties (TSXV:VMET) | CA$1.45 | CA$2.47 | 41.2% |

| TerraVest Industries (TSX:TVK) | CA$143.44 | CA$273.23 | 47.5% |

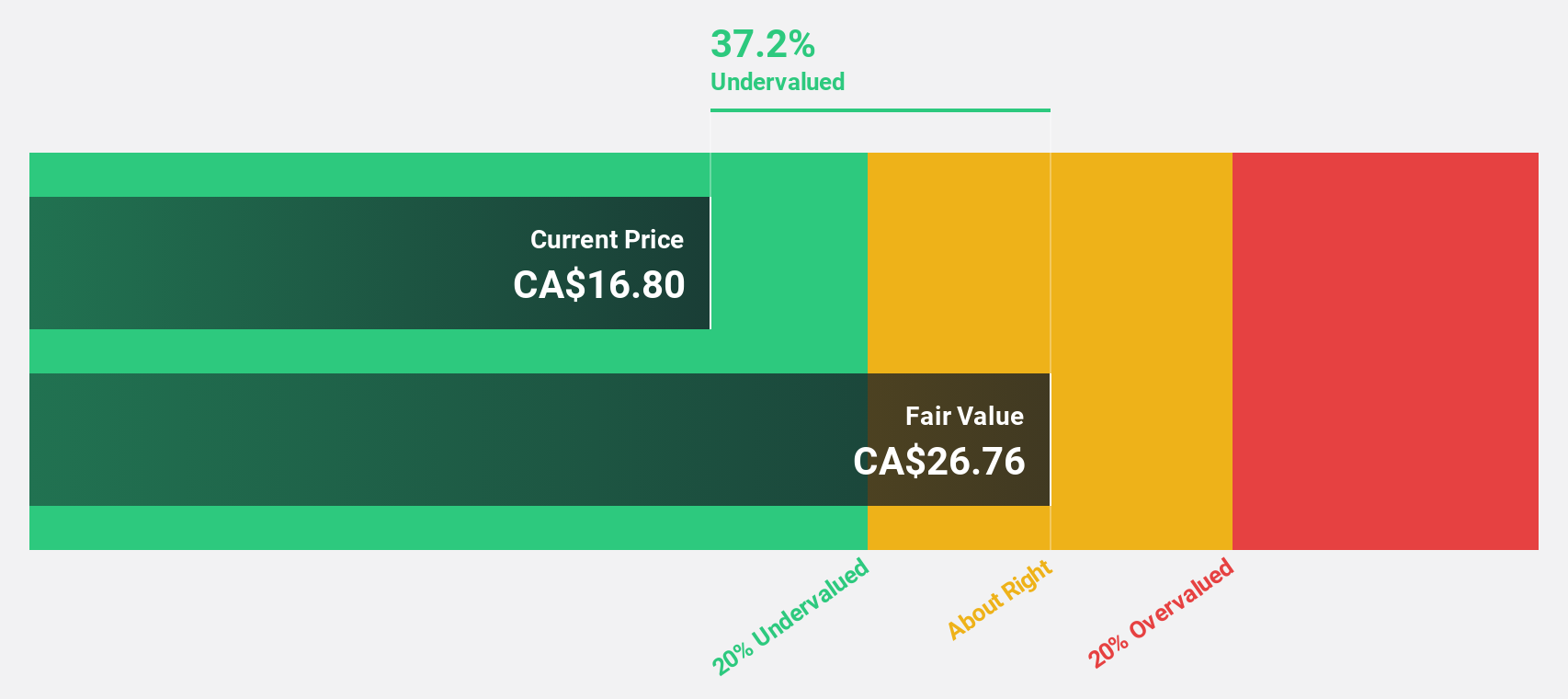

| Magellan Aerospace (TSX:MAL) | CA$15.55 | CA$28.54 | 45.5% |

| K92 Mining (TSX:KNT) | CA$15.42 | CA$27.91 | 44.8% |

| Ivanhoe Mines (TSX:IVN) | CA$11.61 | CA$19.79 | 41.3% |

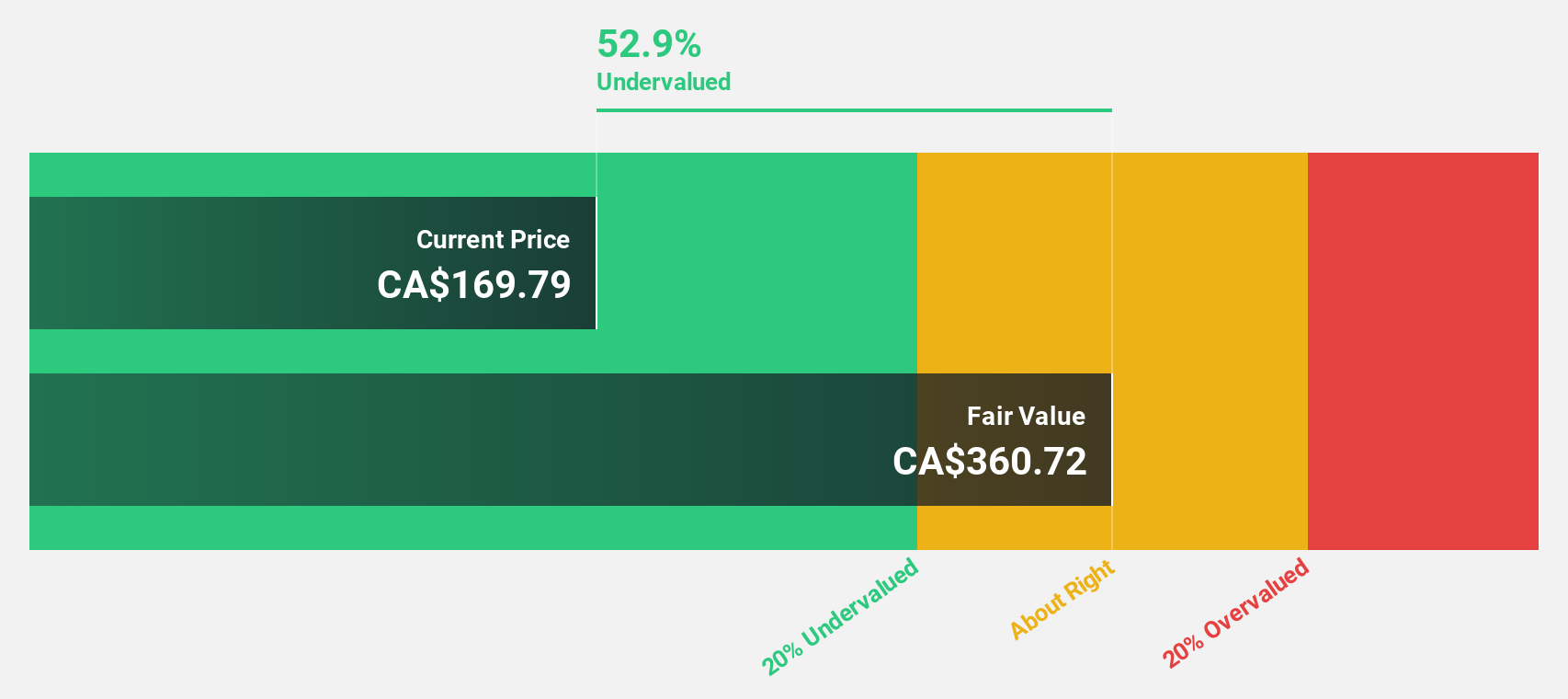

| goeasy (TSX:GSY) | CA$212.76 | CA$381.39 | 44.2% |

| Exchange Income (TSX:EIF) | CA$72.61 | CA$112.16 | 35.3% |

| Endeavour Mining (TSX:EDV) | CA$47.77 | CA$71.91 | 33.6% |

| Boyd Group Services (TSX:BYD) | CA$223.85 | CA$331.56 | 32.5% |

Let's dive into some prime choices out of the screener.

goeasy (TSX:GSY)

Overview: goeasy Ltd. operates in Canada, offering non-prime leasing and lending services through its easyhome, easyfinancial, and LendCare brands, with a market cap of CA$3.42 billion.

Operations: The company's revenue is derived from its Easyhome segment, generating CA$150.03 million, and its Easyfinancial segment, contributing CA$1.45 billion.

Estimated Discount To Fair Value: 44.2%

goeasy is trading at CA$212.76, significantly below its estimated fair value of CA$381.39, indicating potential undervaluation based on cash flows. Despite a high forecasted revenue growth rate of 30.2% per year, the company's dividend yield of 2.74% isn't well covered by free cash flows, and debt coverage by operating cash flow remains inadequate. Recent upsized debt offerings totaling approximately US$450 million and CAD 175 million aim to refinance existing obligations and support corporate purposes.

- Our comprehensive growth report raises the possibility that goeasy is poised for substantial financial growth.

- Get an in-depth perspective on goeasy's balance sheet by reading our health report here.

Magellan Aerospace (TSX:MAL)

Overview: Magellan Aerospace Corporation, with a market cap of CA$890.22 million, engineers and manufactures aeroengine and aerostructure components for aerospace markets in Canada, the United States, and Europe.

Operations: The company generates revenue of CA$974.91 million from its aerospace segment, which includes engineering and manufacturing components for aeroengines and aerostructures across markets in Canada, the United States, and Europe.

Estimated Discount To Fair Value: 45.5%

Magellan Aerospace is trading at CA$15.55, significantly below its estimated fair value of CA$28.54, highlighting potential undervaluation based on cash flows. The company forecasts robust annual earnings growth of 33.2%, outpacing the Canadian market's 10.8%. Recent earnings show a slight decline in quarterly net income to CAD 5.37 million, but six-month figures improved to CAD 16.19 million year-over-year, supporting its value proposition amidst industry challenges and strategic buybacks enhancing shareholder returns.

- Insights from our recent growth report point to a promising forecast for Magellan Aerospace's business outlook.

- Dive into the specifics of Magellan Aerospace here with our thorough financial health report.

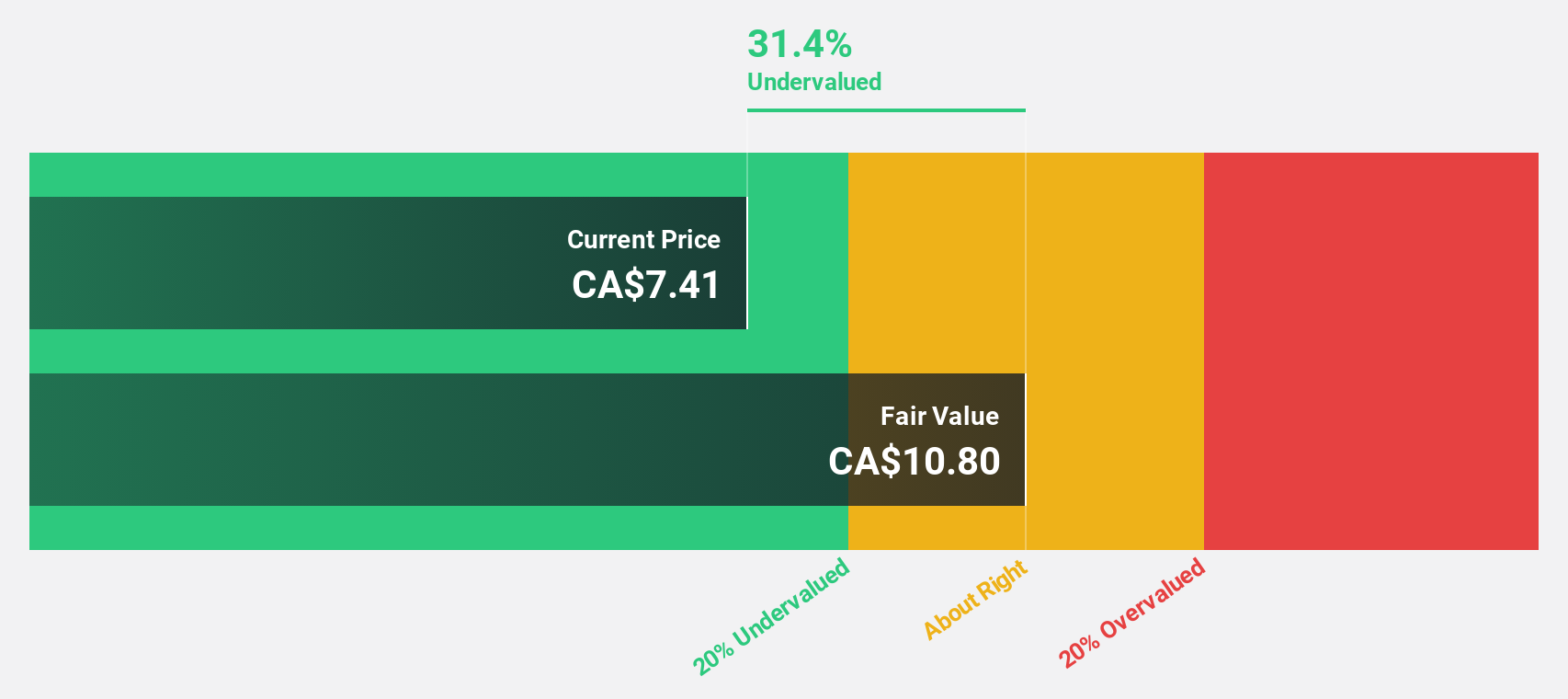

Timbercreek Financial (TSX:TF)

Overview: Timbercreek Financial Corp. offers shorter-duration structured financing solutions to commercial real estate investors in Canada, with a market cap of CA$641.34 million.

Operations: The company's revenue is primarily generated from its Financial Services - Mortgage segment, amounting to CA$67.32 million.

Estimated Discount To Fair Value: 30.1%

Timbercreek Financial trades at CA$7.75, below its estimated fair value of CA$11.08, suggesting undervaluation based on cash flows. Despite a recent drop in quarterly net income to CAD 12.37 million, the company forecasts annual earnings growth of 18.81%, surpassing the Canadian market's 10.9%. However, debt coverage by operating cash flow is weak and dividends are not well covered by earnings or free cash flows, indicating potential financial constraints despite strategic credit facility enhancements and buyback plans.

- Our expertly prepared growth report on Timbercreek Financial implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of Timbercreek Financial with our detailed financial health report.

Seize The Opportunity

- Access the full spectrum of 22 Undervalued TSX Stocks Based On Cash Flows by clicking on this link.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Timbercreek Financial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:TF

Timbercreek Financial

Provides shorter-duration structured financing solutions to commercial real estate investors in Canada.

Good value with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|48.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|6.4% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|19.4% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|51.6% overvalued

RO

Community Contributor