Advertisement

Tornado Infrastructure Equipment (TSXV:TGH) Q3 Profit Jump Supports Bullish Margin-Improvement Narrative

Simply Wall St

Reviewed by Simply Wall St

Latest Quarterly Snapshot

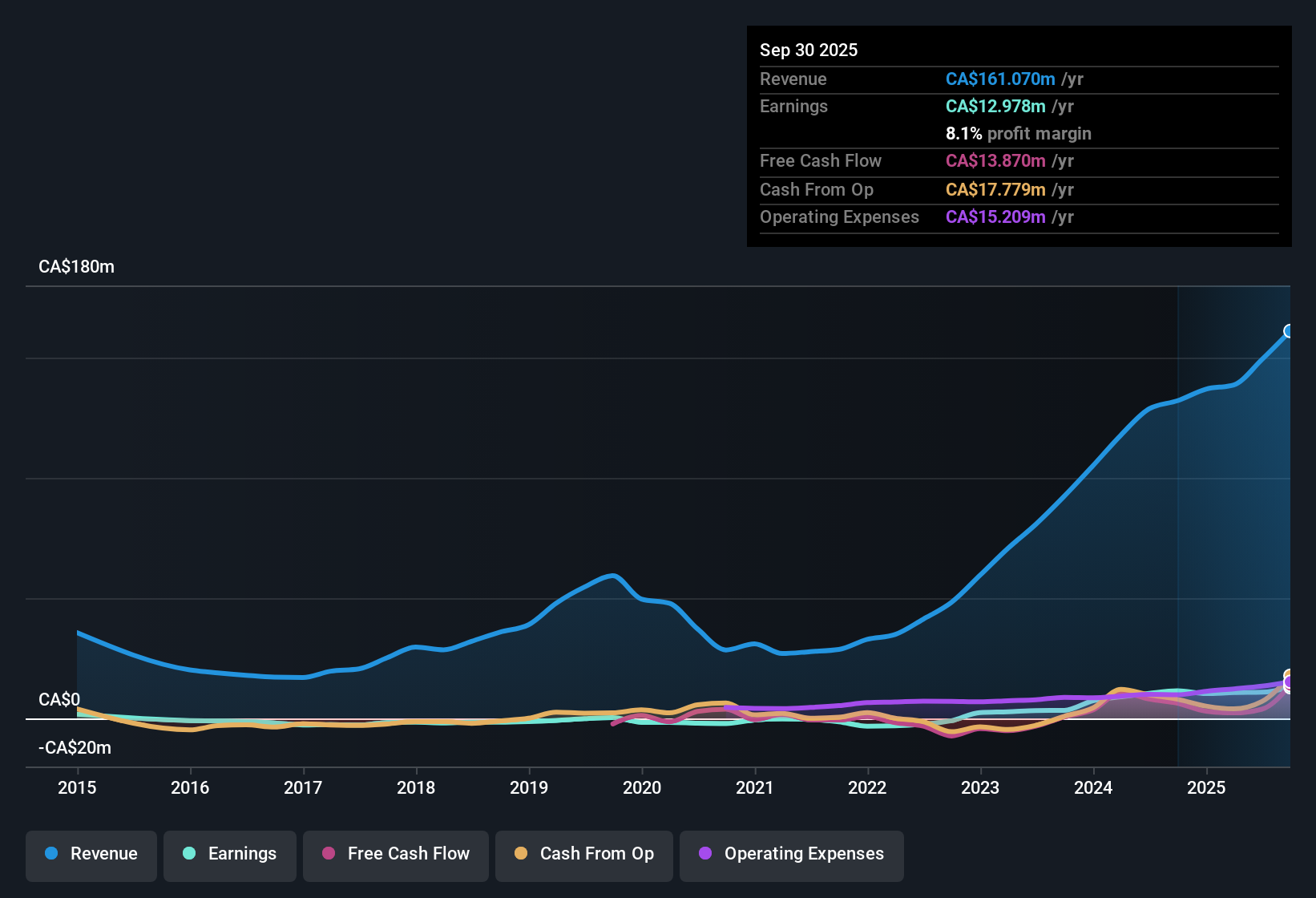

Tornado Infrastructure Equipment (TSXV:TGH) has just posted its Q3 2025 numbers, with revenue of CA$42.3 million, basic EPS of CA$0.029 and net income of CA$4.1 million setting the tone for the quarter. The company has seen quarterly revenue move from CA$30.5 million in Q3 2024 to CA$42.3 million in Q3 2025, while net income shifted from CA$2.0 million to CA$4.1 million over the same period, alongside trailing twelve month EPS of roughly CA$0.09. This helps frame the latest results in a broader earnings trend. With those figures on the table, the focus now is on how sustainably the business can defend and build its margins as growth opportunities unfold.

See our full analysis for Tornado Infrastructure Equipment.With the headline numbers laid out, the next step is to see how they compare with the dominant narratives around Tornado Infrastructure Equipment and whether the latest margin and growth patterns support or challenge those stories.

Curious how numbers become stories that shape markets? Explore Community Narratives

13% earnings growth but softer margin

- Over the last 12 months, net income reached about CA$13.0 million on CA$161.1 million of revenue, giving an 8.1% net margin compared with 8.7% the year before.

- Bulls point out that 13% earnings growth over the past year still backs a growth story, yet the slip in net margin from 8.7% to 8.1% shows profitability is not keeping pace with the stronger 22.4% revenue growth forecast, which is less aggressive than the 64.8% per year earnings growth seen over five years.

- This combination supports the bullish view that the business is scaling, but also highlights that recent profit expansion is slower than its longer term track record.

- For a beginner investor, it means the company is growing and profitable, though the pace of improvement is more moderate than in earlier years.

Valuation sits well below DCF fair value

- The shares trade at CA$1.91 with a trailing P E of 20.4 times, versus an industry average of 24.3 times, and below a DCF fair value estimate of roughly CA$4.28.

- Supporters argue that paying below both the industry P E and the DCF fair value, with the stock about 55% under that CA$4.28 level, strongly supports a bullish case that the market is not fully crediting forecast revenue growth of 22.4% a year and the recent 13% earnings increase.

- The gap between the current price and DCF fair value suggests potential upside if the company simply maintains its recent profitability profile.

- At the same time, the discount might also reflect that margins have edged down from 8.7% to 8.1%, so the valuation is balancing growth with execution risk.

Q3 profit lift versus recent quarters

- Within this year, net income moved from CA$2.68 million in Q2 2025 to CA$4.08 million in Q3 2025, even though revenue dipped slightly from CA$45.0 million to CA$42.3 million across those quarters.

- What stands out for a cautiously bullish read is that higher quarterly profit on slightly lower revenue suggests some improvement in how each dollar of sales turns into earnings, especially compared with Q4 2024 net income of CA$3.37 million on CA$38.1 million of revenue.

- This pattern can support the idea that management is working on efficiency, even as the broader twelve month margin is a bit lower year over year.

- Investors can watch future quarters to see whether this better quarterly conversion holds up alongside the forecast 22.4% annual revenue growth.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on Tornado Infrastructure Equipment's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

Explore Alternatives

Despite solid top line growth and a discount to DCF, Tornado Infrastructure Equipment is seeing net margins soften and profit expansion trail its longer term earnings trajectory.

If that margin pressure makes you cautious, shift your focus to stable growth stocks screener (2073 results) to quickly find companies already proving they can grow steadily without sacrificing profitability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tornado Infrastructure Equipment might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSXV:TGH

Tornado Infrastructure Equipment

Through its subsidiaries, designs, fabricates, manufactures, and sells hydrovac trucks in North America.

Excellent balance sheet and good value.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

9 followersusers have followed this narrative

5 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Marvell Technology ·

The Great Strategy Swap – Selling "Old Auto" to Buy "Future Light"

Fair Value:US$155.3740.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9238.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.6% undervalued

946 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.2% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative