Advertisement

3 TSX Stocks That Could Be Undervalued Based On Current Estimates

Simply Wall St

Reviewed by Simply Wall St

In the last week, the Canadian market has been flat, but it is up 13% over the past year with earnings expected to grow by 15% per annum. In this context, identifying undervalued stocks that have strong growth potential can be a strategic move for investors looking to capitalize on current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| goeasy (TSX:GSY) | CA$184.27 | CA$359.78 | 48.8% |

| Computer Modelling Group (TSX:CMG) | CA$12.13 | CA$22.28 | 45.6% |

| Alvopetro Energy (TSXV:ALV) | CA$5.08 | CA$9.07 | 44% |

| Calian Group (TSX:CGY) | CA$44.36 | CA$72.65 | 38.9% |

| Africa Oil (TSX:AOI) | CA$1.91 | CA$3.70 | 48.4% |

| Kinaxis (TSX:KXS) | CA$147.96 | CA$280.68 | 47.3% |

| Viemed Healthcare (TSX:VMD) | CA$10.45 | CA$20.08 | 48% |

| Triple Flag Precious Metals (TSX:TFPM) | CA$21.40 | CA$33.37 | 35.9% |

| NanoXplore (TSX:GRA) | CA$2.31 | CA$4.20 | 45% |

| Opsens (TSX:OPS) | CA$2.90 | CA$4.64 | 37.5% |

Underneath we present a selection of stocks filtered out by our screen.

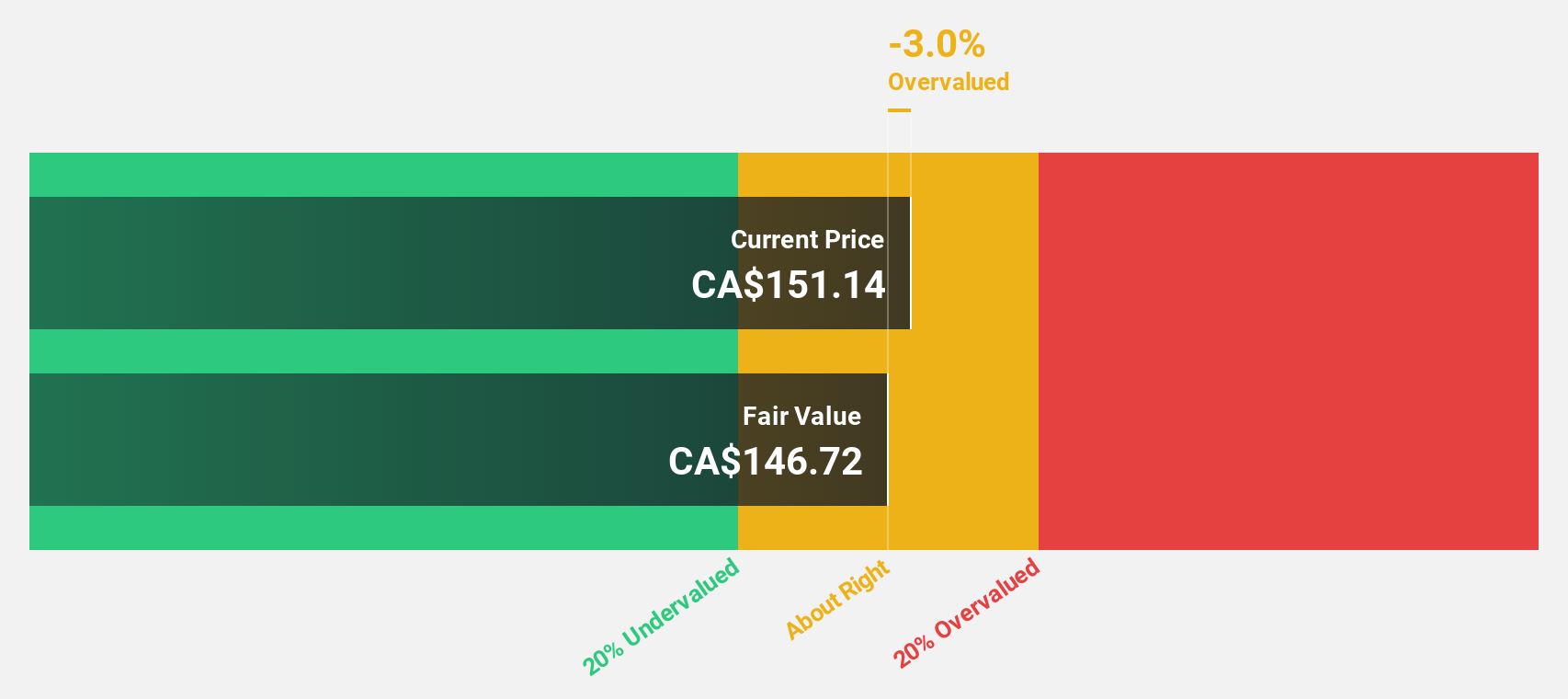

Docebo (TSX:DCBO)

Overview: Docebo Inc. is a learning management software company that offers an AI-powered learning platform across North America and internationally, with a market cap of CA$1.75 billion.

Operations: The company's revenue segment is primarily derived from its educational software, generating $200.24 million.

Estimated Discount To Fair Value: 22.4%

Docebo Inc. is trading 22.4% below its estimated fair value, with a current price of CA$57.48 compared to a fair value of CA$74.09. Recent earnings show significant improvement, with Q2 sales at US$53.05 million and net income at US$4.7 million, reversing a loss from the previous year. Earnings are forecast to grow 34% annually over the next three years, outpacing both revenue growth and market averages in Canada.

- According our earnings growth report, there's an indication that Docebo might be ready to expand.

- Get an in-depth perspective on Docebo's balance sheet by reading our health report here.

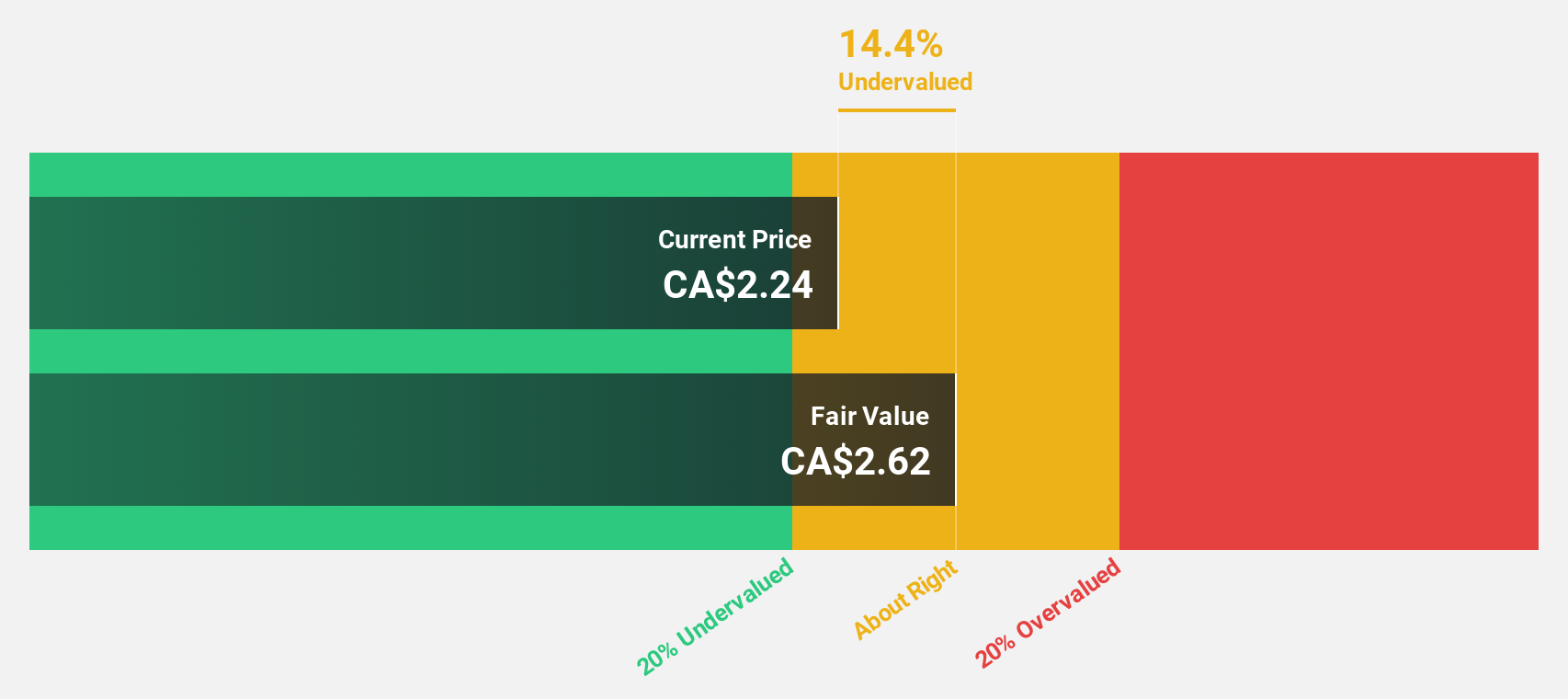

NanoXplore (TSX:GRA)

Overview: NanoXplore Inc. is a graphene company that manufactures and supplies graphene powder for industrial markets, with a market cap of CA$371.93 million.

Operations: NanoXplore generates revenue from manufacturing and supplying graphene powder for various industrial markets.

Estimated Discount To Fair Value: 45%

NanoXplore Inc. is trading at CA$2.31, significantly below its estimated fair value of CA$4.20, indicating it may be undervalued based on cash flows. Despite having less than a year of cash runway, the company is forecast to grow revenues by 22.8% annually and become profitable within three years, outpacing market averages in Canada. The recent addition of Ms. Hélène V. Gagnon to the Board could enhance governance and sustainability efforts, potentially boosting investor confidence.

- Our comprehensive growth report raises the possibility that NanoXplore is poised for substantial financial growth.

- Navigate through the intricacies of NanoXplore with our comprehensive financial health report here.

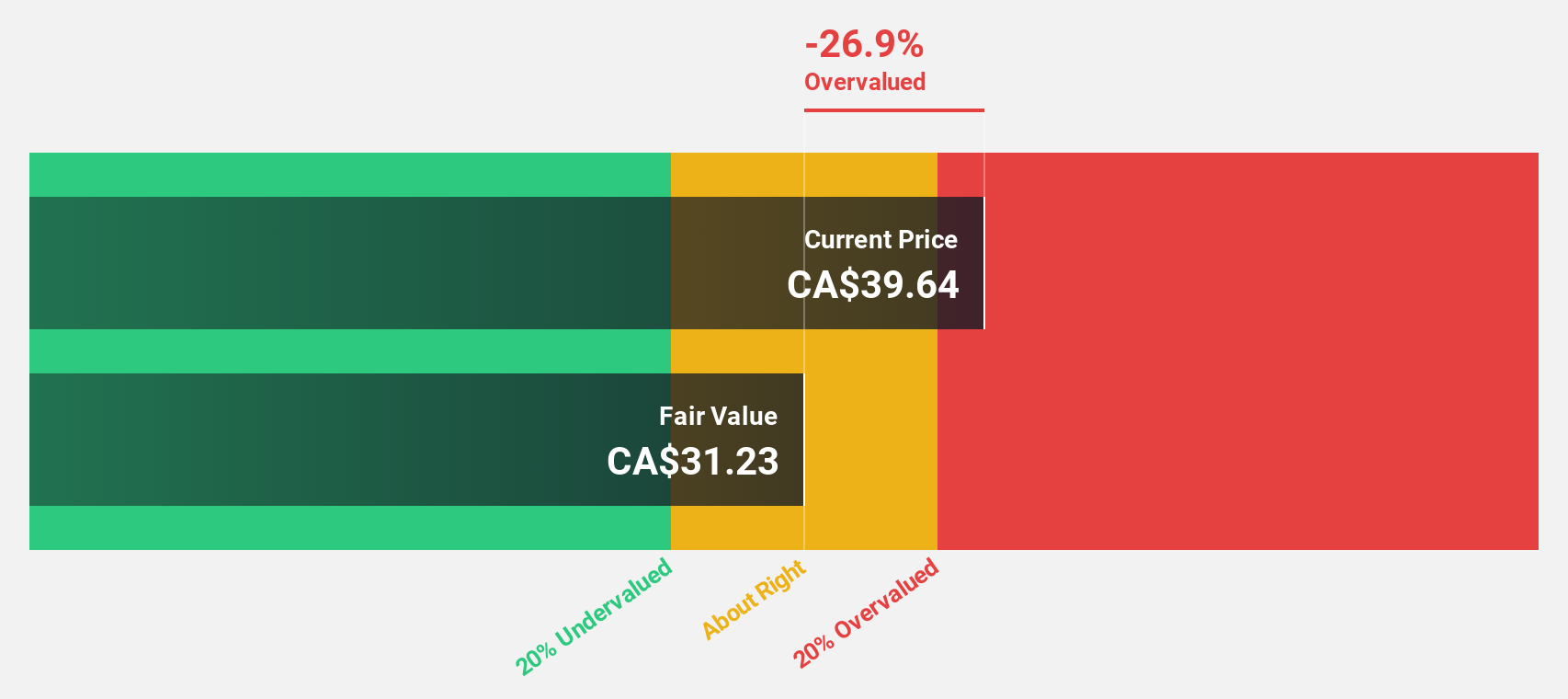

Stantec (TSX:STN)

Overview: Stantec Inc. offers professional services for infrastructure and facilities to both public and private sectors across Canada, the United States, and internationally, with a market cap of CA$12.55 billion.

Operations: Revenue segments for Stantec Inc. are as follows: CA$1.32 billion from Canada, CA$1.22 billion from Global operations, and CA$2.88 billion from the United States.

Estimated Discount To Fair Value: 10.3%

Stantec Inc. is trading at CA$107.99, approximately 10% below its estimated fair value of CA$120.4, suggesting it may be undervalued based on cash flows. Despite a high level of debt, earnings have grown 15.8% annually over the past five years and are expected to grow significantly faster than the Canadian market at 20.9% per year over the next three years. Recent client agreements with LADWP further bolster its revenue prospects and strategic positioning in clean energy initiatives.

- In light of our recent growth report, it seems possible that Stantec's financial performance will exceed current levels.

- Dive into the specifics of Stantec here with our thorough financial health report.

Key Takeaways

- Reveal the 29 hidden gems among our Undervalued TSX Stocks Based On Cash Flows screener with a single click here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if NanoXplore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:GRA

NanoXplore

A graphene company, manufactures and supplies graphene powder for use in industrial markets in Australia.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor