Advertisement

- Canada

- /

- Electrical

- /

- TSX:HPS.A

You Might Like Hammond Power Solutions Inc. (TSE:HPS.A) But Do You Like Its Debt?

While small-cap stocks, such as Hammond Power Solutions Inc. (TSE:HPS.A) with its market cap of CA$84m, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Understanding the company's financial health becomes essential, since poor capital management may bring about bankruptcies, which occur at a higher rate for small-caps. The following basic checks can help you get a picture of the company's balance sheet strength. Nevertheless, potential investors would need to take a closer look, and I’d encourage you to dig deeper yourself into HPS.A here.

Does HPS.A Produce Much Cash Relative To Its Debt?

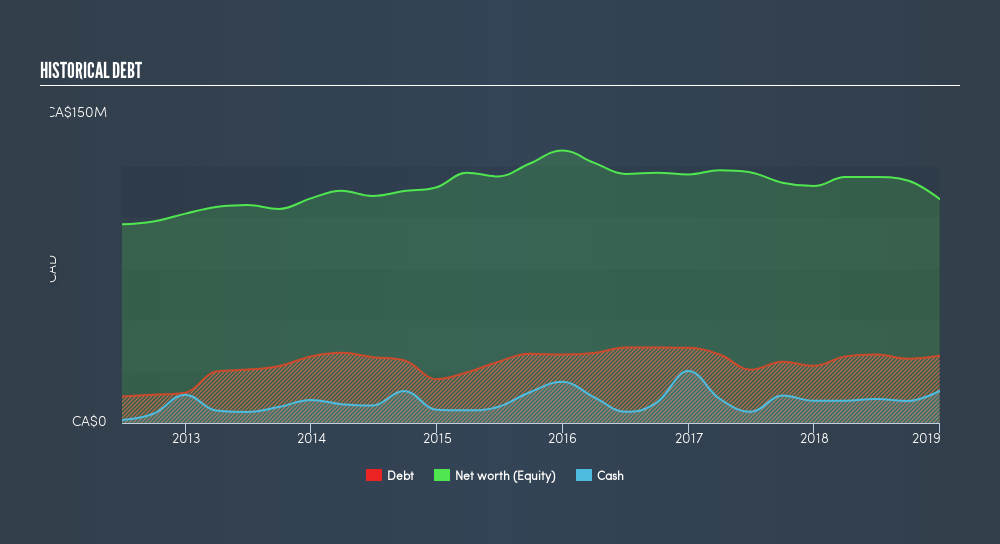

HPS.A has built up its total debt levels in the last twelve months, from CA$28m to CA$33m . With this rise in debt, HPS.A currently has CA$16m remaining in cash and short-term investments , ready to be used for running the business. Moreover, HPS.A has produced CA$6.5m in operating cash flow during the same period of time, leading to an operating cash to total debt ratio of 20%, signalling that HPS.A’s operating cash is less than its debt.

Can HPS.A pay its short-term liabilities?

At the current liabilities level of CA$94m, it seems that the business has been able to meet these commitments with a current assets level of CA$138m, leading to a 1.47x current account ratio. The current ratio is the number you get when you divide current assets by current liabilities. Usually, for Electrical companies, this is a suitable ratio since there is a bit of a cash buffer without leaving too much capital in a low-return environment.

Can HPS.A service its debt comfortably?

With a debt-to-equity ratio of 30%, HPS.A's debt level may be seen as prudent. HPS.A is not taking on too much debt commitment, which can be restrictive and risky for equity-holders. We can test if HPS.A’s debt levels are sustainable by measuring interest payments against earnings of a company. Ideally, earnings before interest and tax (EBIT) should cover net interest by at least three times. For HPS.A, the ratio of 22.44x suggests that interest is comfortably covered, which means that lenders may be inclined to lend more money to the company, as it is seen as safe in terms of payback.

Next Steps:

HPS.A has demonstrated its ability to generate sufficient levels of cash flow, while its debt hovers at an appropriate level. Furthermore, the company exhibits an ability to meet its near term obligations should an adverse event occur. This is only a rough assessment of financial health, and I'm sure HPS.A has company-specific issues impacting its capital structure decisions. I recommend you continue to research Hammond Power Solutions to get a better picture of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for HPS.A’s future growth? Take a look at our free research report of analyst consensus for HPS.A’s outlook.

- Valuation: What is HPS.A worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether HPS.A is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:HPS.A

Hammond Power Solutions

Engages in the design, manufacture, and sale of various transformers in Canada, the United States, Mexico, and India.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

42 followersusers have followed this narrative

6 commentsusers have commented on this narrative

15 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

SC

scm on Text ·

TXT will see revenue grow 26% with a profit margin boost of almost 40%

Fair Value:zł8049.8% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

955 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative