Advertisement

Toronto-Dominion Bank (TSX:TD) Navigates Regulatory Challenges with Strong Q3 Earnings and Market Expansion

Simply Wall St

Reviewed by Simply Wall St

Toronto-Dominion Bank (TSX:TD) is navigating a dynamic environment marked by both opportunities and challenges. Recent highlights include a strong Q3 financial performance and innovative product launches, juxtaposed against regulatory issues and economic volatility. In the discussion that follows, we will explore TD's financial health, operational inefficiencies, strategic growth initiatives, and external threats to provide a comprehensive overview of the bank's current business situation.

Get an in-depth perspective on Toronto-Dominion Bank's performance by reading our analysis here.

Innovative Factors Supporting Toronto-Dominion Bank

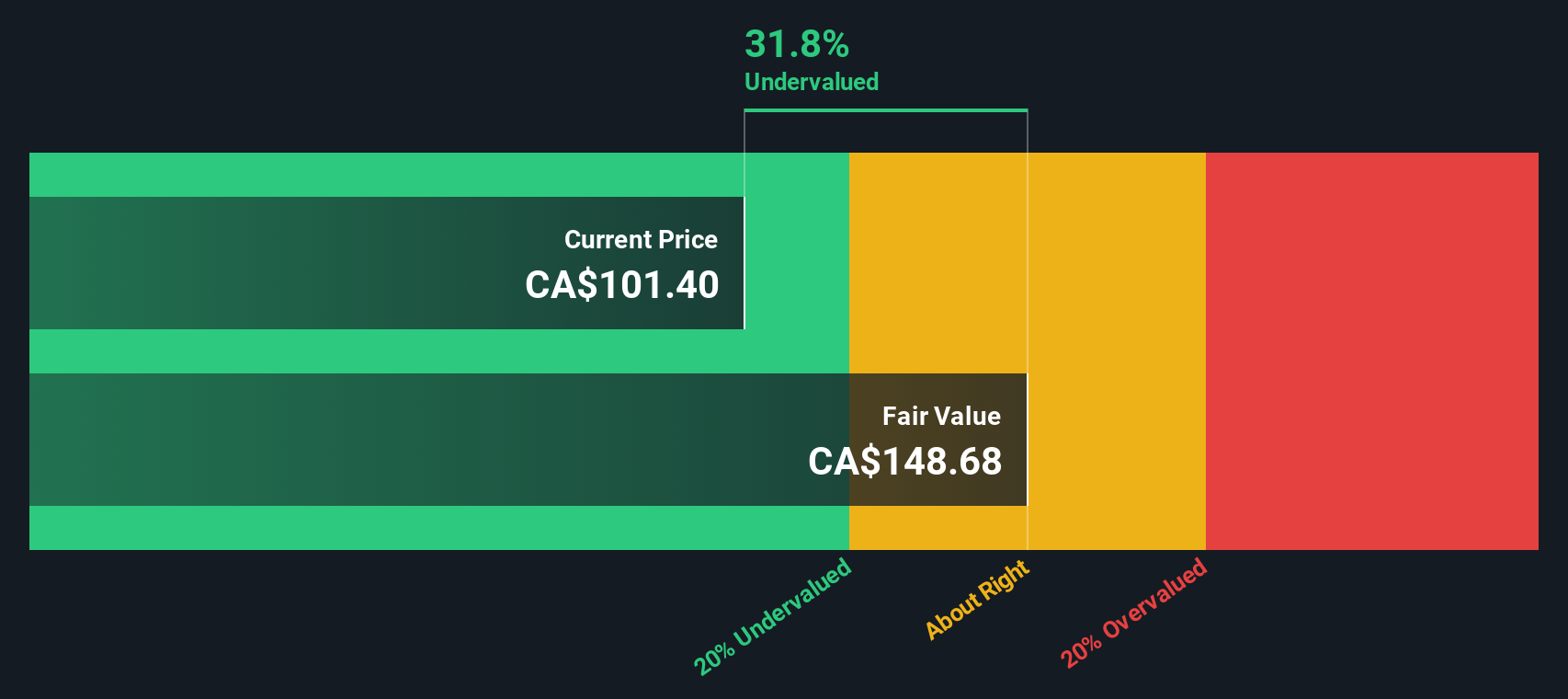

Toronto-Dominion Bank (TD) has demonstrated strong financial performance, with Q3 earnings reaching $3.6 billion and an EPS of $2.05, reflecting solid business fundamentals. The bank's revenue grew by 8% year-over-year, driven by higher fee income and improved deposit margins in Canadian Personal and Commercial Banking. Notably, TD's Canadian Personal and Commercial Banking segment achieved record revenues of $5 billion and a 13% increase in net income. Additionally, TD's customer base expanded significantly, with over 8 million active credit card accounts, reinforcing its market leadership. The bank's innovative edge is highlighted by its recognition as the Best Consumer Digital Bank in Canada for the fourth consecutive year and the Best Transformation and Innovation in North America for the second consecutive year. TD's strong capital position, with ample liquidity, supports its investments in AML remediation and customer experience enhancements. Trading at CA$85.89, TD is significantly below the estimated fair value of CA$159.99, indicating potential undervaluation despite being considered expensive relative to industry and peer price-to-earnings ratios.

Vulnerabilities Impacting Toronto-Dominion Bank

However, TD faces notable challenges, including a substantial USD 2.6 billion provision for AML matters, reflecting ongoing regulatory issues. The bank's expenses have increased year-over-year due to investments in risk and control infrastructure and higher employee-related costs. Additionally, insurance service expenses rose by 20% year-over-year, primarily due to severe weather-related claims. TD's earnings growth has been negative over the past year, with a 44.9% decline, making it difficult to compare to the industry average of 11.2%. The bank's current net profit margins of 14.7% are significantly lower than last year's 27.7%. Despite these challenges, TD's management team, with an average tenure of 2.8 years, and its board of directors, with an average tenure of 9.6 years, bring considerable experience to navigate these issues.

Areas for Expansion and Innovation for Toronto-Dominion Bank

Opportunities for TD include market expansion and product-related announcements. The bank has extended its new-to-Canada packages to include TD Direct Investing and the TD Cash Back Visa Card, enhancing its market position. Additionally, TD's launch of real-time partial shares in Canada makes investing more accessible, showcasing its commitment to innovation. Investments in data and technology to improve transaction monitoring and data analytics capabilities further strengthen TD's competitive edge. Earnings are forecast to grow by 18% per year, outpacing the Canadian market's 14.6% growth rate. These strategic initiatives position TD to capitalize on emerging opportunities and enhance its market presence.

Market Volatility Affecting Toronto-Dominion Bank's Position

Despite these opportunities, TD faces significant threats, including regulatory challenges and economic volatility. The bank must focus on meeting its obligations and responsibilities to build a stronger foundation. The current market environment is characterized by significant volatility, rapidly evolving rate expectations, and heightened geopolitical risks. Additionally, competition remains fierce, with the market being highly competitive. TD's dividend yield of 4.75% is lower than the top 25% of dividend payers in the Canadian market (5.77%), and its high payout ratio of 92.7% indicates that dividend payments are not well covered by earnings. These external factors pose risks to TD's growth and market share, necessitating strategic responses to maintain its competitive position.

To gain deeper insights into Toronto-Dominion Bank's historical performance, explore our detailed analysis of past performance.To dive deeper into how Toronto-Dominion Bank's valuation metrics are shaping its market position, check out our detailed analysis of Toronto-Dominion Bank's Valuation.

Conclusion

Toronto-Dominion Bank's strong financial performance, highlighted by a significant increase in Q3 earnings and record revenues in its Canadian Personal and Commercial Banking segment, underscores its solid business fundamentals and market leadership. However, the bank faces critical challenges, including substantial regulatory provisions and increased operational costs, which have impacted its earnings growth and profit margins. Despite these vulnerabilities, TD's strategic initiatives in market expansion and technology investments position it well for future growth, with earnings forecast to outpace the Canadian market. Trading at CA$85.89, significantly below its estimated fair value of CA$159.99, the bank presents a compelling opportunity for investors, provided it can navigate the economic volatility and regulatory pressures effectively.

Where To Now?

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Valuation is complex, but we're here to simplify it.

Discover if Toronto-Dominion Bank might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About TSX:TD

Toronto-Dominion Bank

Provides various financial products and services in Canada, the United States, and internationally.

Flawless balance sheet, undervalued and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor