- Canada

- /

- Oil and Gas

- /

- TSX:PEY

3 Canadian Dividend Stocks On TSX Yielding Up To 8.4%

Reviewed by Simply Wall St

As the Canadian market rides a wave of optimism, buoyed by recent rate cuts from the U.S. Federal Reserve and enthusiasm around AI, the TSX has reached all-time highs, reflecting strong performance even amidst looming election uncertainties in the U.S. This backdrop provides an opportune moment to explore dividend stocks on the TSX that offer attractive yields, as they can provide steady income and potential growth in a market focused on economic expansion and rising corporate earnings.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Whitecap Resources (TSX:WCP) | 6.93% | ★★★★★★ |

| Secure Energy Services (TSX:SES) | 3.29% | ★★★★★☆ |

| Labrador Iron Ore Royalty (TSX:LIF) | 7.77% | ★★★★★☆ |

| Power Corporation of Canada (TSX:POW) | 5.24% | ★★★★★☆ |

| Enghouse Systems (TSX:ENGH) | 3.09% | ★★★★★☆ |

| Firm Capital Mortgage Investment (TSX:FC) | 8.65% | ★★★★★☆ |

| Russel Metals (TSX:RUS) | 4.16% | ★★★★★☆ |

| Sun Life Financial (TSX:SLF) | 4.14% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.42% | ★★★★★☆ |

| Canadian Natural Resources (TSX:CNQ) | 4.49% | ★★★★★☆ |

Click here to see the full list of 31 stocks from our Top TSX Dividend Stocks screener.

Here we highlight a subset of our preferred stocks from the screener.

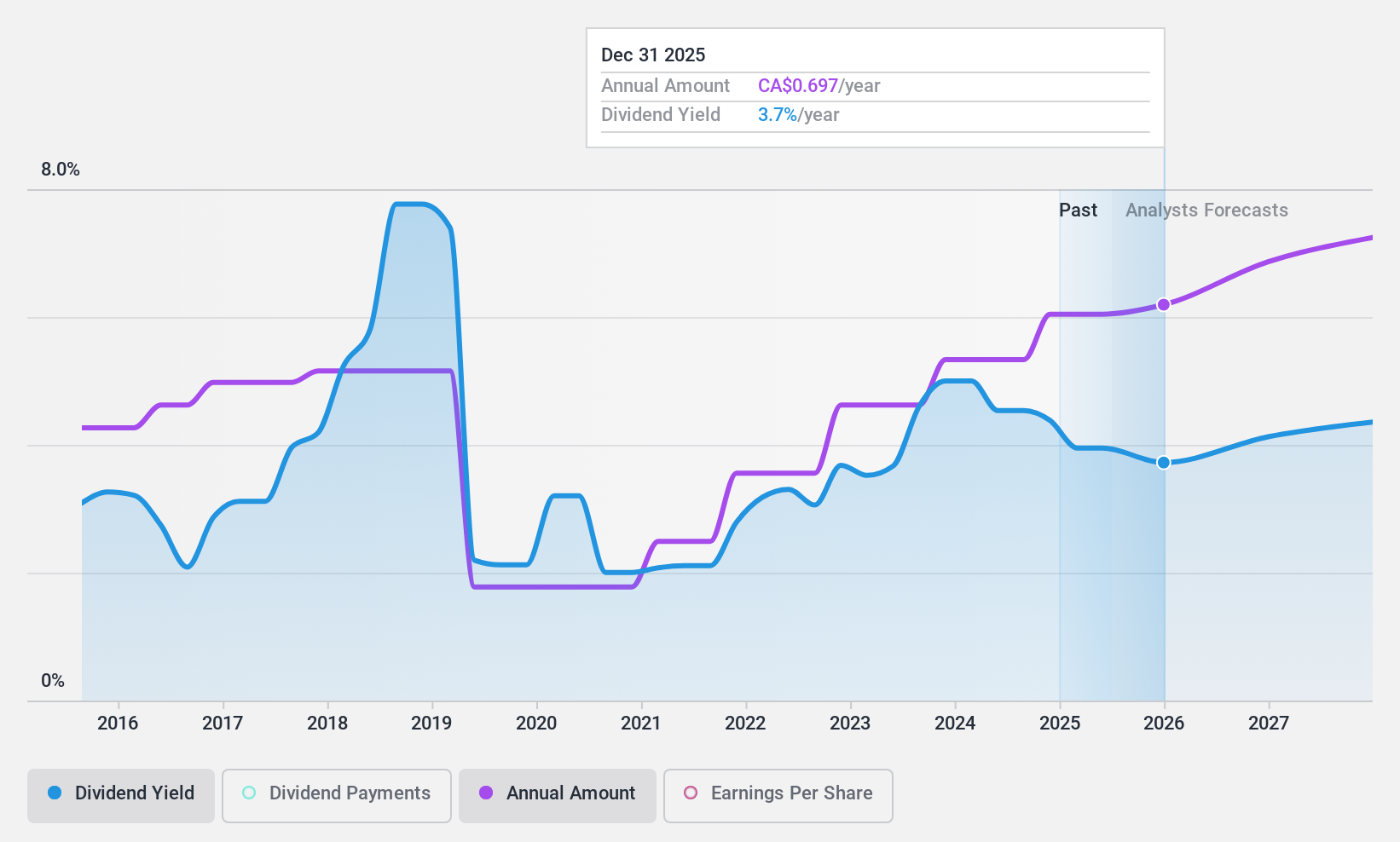

High Liner Foods (TSX:HLF)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: High Liner Foods Incorporated processes and markets frozen seafood products in North America, with a market cap of CA$373.04 million.

Operations: High Liner Foods generates revenue of $992.12 million from the manufacturing and marketing of prepared and packaged frozen seafood.

Dividend Yield: 4.7%

High Liner Foods recently reported strong earnings growth, with net income rising significantly despite a decline in sales. The company affirmed a quarterly dividend of C$0.15 per share, supported by a low payout ratio and robust cash flow coverage, though its historical dividend stability has been volatile. Recent debt refinancing is expected to reduce interest expenses, potentially benefiting future dividend sustainability. Share buybacks totaling 1.99% indicate confidence in its financial position despite high debt levels.

- Take a closer look at High Liner Foods' potential here in our dividend report.

- Our valuation report here indicates High Liner Foods may be undervalued.

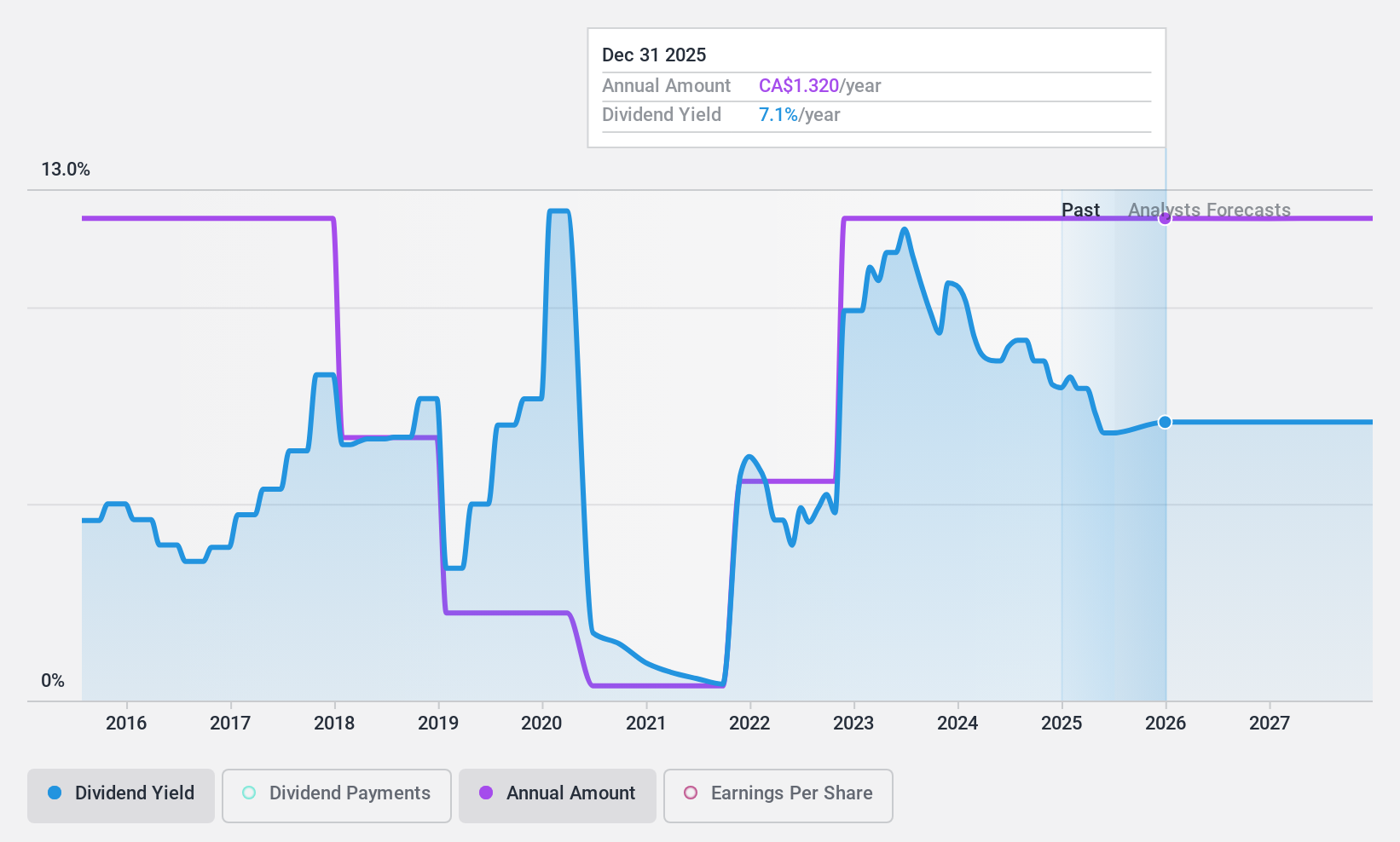

Peyto Exploration & Development (TSX:PEY)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Peyto Exploration & Development Corp. is an energy company focused on the exploration, development, and production of natural gas, oil, and natural gas liquids in Alberta's Deep Basin with a market cap of CA$3.08 billion.

Operations: Peyto Exploration & Development Corp. generates its revenue from the exploration and production of oil and gas, amounting to CA$901.99 million.

Dividend Yield: 8.4%

Peyto Exploration & Development confirmed a monthly dividend of C$0.11 per share, reflecting its top-tier yield of 8.4% in Canada. Despite this, the dividend's sustainability is questionable due to a high cash payout ratio of 113.6% and significant debt levels. Although earnings cover the current payout ratio of 84.1%, historical volatility and shareholder dilution raise concerns about reliability and long-term stability, despite trading at a perceived discount to fair value.

- Dive into the specifics of Peyto Exploration & Development here with our thorough dividend report.

- Our valuation report unveils the possibility Peyto Exploration & Development's shares may be trading at a discount.

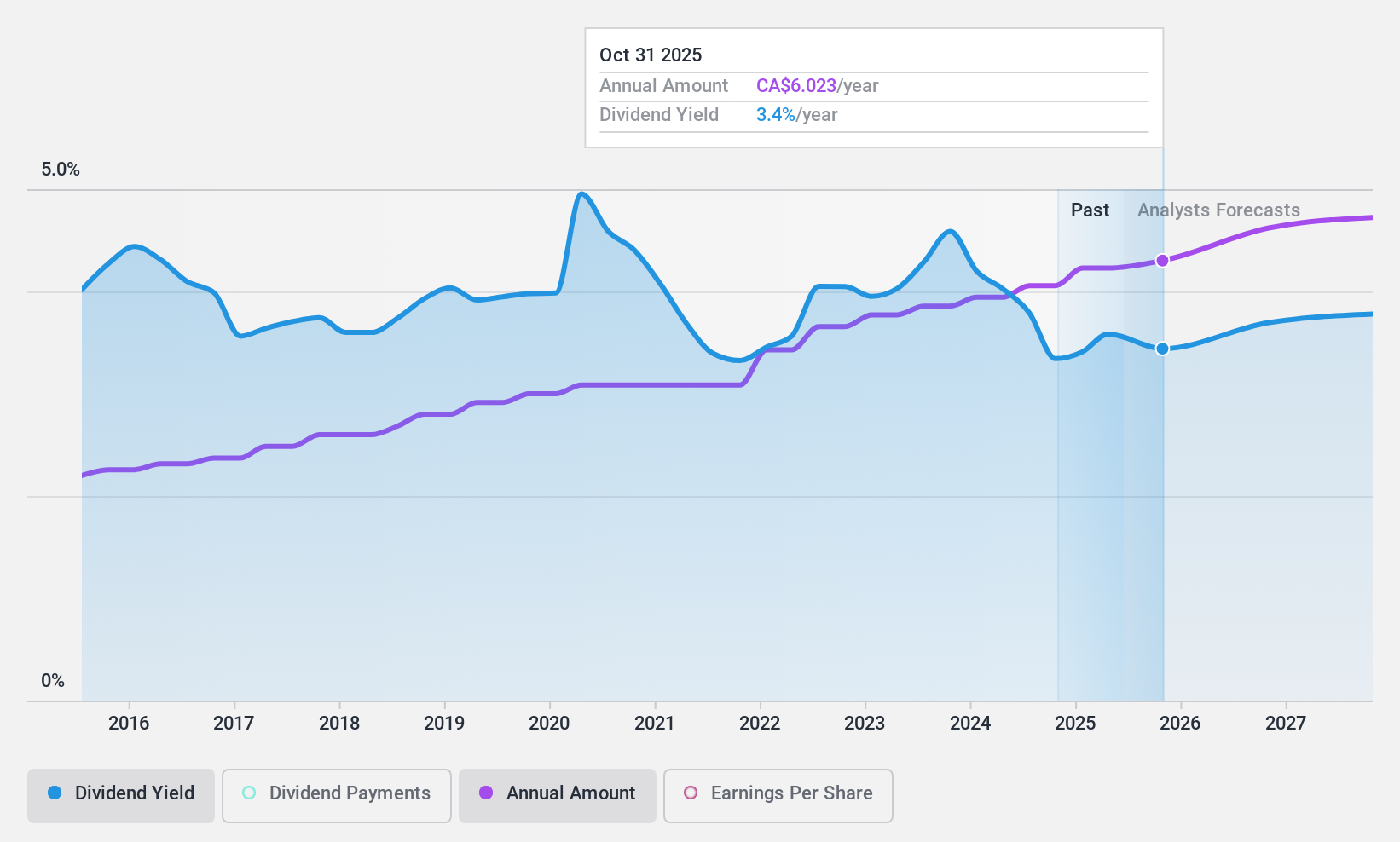

Royal Bank of Canada (TSX:RY)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Royal Bank of Canada operates as a diversified financial services company worldwide with a market cap of CA$236.33 billion.

Operations: Royal Bank of Canada's revenue is primarily derived from Personal & Commercial Banking (CA$21.78 billion), Wealth Management (CA$17.92 billion), Capital Markets (CA$11.19 billion), and Insurance (CA$5.86 billion).

Dividend Yield: 3.4%

Royal Bank of Canada maintains a stable dividend with a reliable history over the past decade, supported by a low payout ratio of 49%, indicating sustainability. While its yield of 3.42% is below the top Canadian dividend payers, it trades at a discount to estimated fair value. Recent fixed-income offerings suggest strategic financial maneuvers to support growth and stability. The appointment of Katherine Gibson as CFO may further enhance financial oversight and strategic direction amid ongoing growth initiatives.

- Click here and access our complete dividend analysis report to understand the dynamics of Royal Bank of Canada.

- Upon reviewing our latest valuation report, Royal Bank of Canada's share price might be too optimistic.

Key Takeaways

- Unlock more gems! Our Top TSX Dividend Stocks screener has unearthed 28 more companies for you to explore.Click here to unveil our expertly curated list of 31 Top TSX Dividend Stocks.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:PEY

Peyto Exploration & Development

An energy company, engages in the exploration, development, and production of natural gas, oil, and natural gas liquids in Deep Basin of Alberta.

Undervalued with reasonable growth potential and pays a dividend.