Bank of Montreal's (TSE:BMO) Shareholders Will Receive A Bigger Dividend Than Last Year

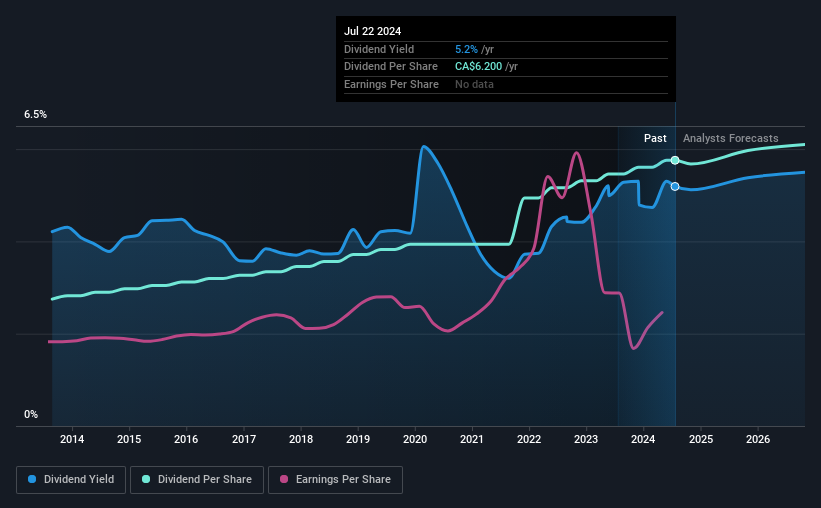

Bank of Montreal (TSE:BMO) has announced that it will be increasing its dividend from last year's comparable payment on the 27th of August to CA$1.55. This takes the annual payment to 5.2% of the current stock price, which is about average for the industry.

See our latest analysis for Bank of Montreal

Bank of Montreal's Earnings Will Easily Cover The Distributions

Solid dividend yields are great, but they only really help us if the payment is sustainable.

Having distributed dividends for at least 10 years, Bank of Montreal has a long history of paying out a part of its earnings to shareholders. Past distributions do not necessarily guarantee future ones, but Bank of Montreal's payout ratio of 72% is a good sign as this means that earnings decently cover dividends.

The next 3 years are set to see EPS grow by 54.2%. Analysts estimate the future payout ratio will be 53% over the same time period, which is in the range that makes us comfortable with the sustainability of the dividend.

Bank of Montreal Has A Solid Track Record

The company has an extended history of paying stable dividends. The annual payment during the last 10 years was CA$2.96 in 2014, and the most recent fiscal year payment was CA$6.20. This implies that the company grew its distributions at a yearly rate of about 7.7% over that duration. The growth of the dividend has been pretty reliable, so we think this can offer investors some nice additional income in their portfolio.

The Dividend's Growth Prospects Are Limited

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. Unfortunately things aren't as good as they seem. It's not great to see that Bank of Montreal's earnings per share has fallen at approximately 2.7% per year over the past five years. Declining earnings will inevitably lead to the company paying a lower dividend in line with lower profits. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this can turn into a longer term trend.

Our Thoughts On Bank of Montreal's Dividend

Overall, this is a reasonable dividend, and it being raised is an added bonus. While the payments look sustainable for now, earnings have been shrinking so the dividend could come under pressure in the future. The dividend looks okay, but there have been some issues in the past, so we would be a little bit cautious.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Given that earnings are not growing, the dividend does not look nearly so attractive. Very few businesses see earnings consistently shrink year after year in perpetuity though, and so it might be worth seeing what the 12 analysts we track are forecasting for the future. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Bank of Montreal might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:BMO

Bank of Montreal

Provides diversified financial services primarily in North America.

Solid track record with excellent balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives