- Brazil

- /

- Renewable Energy

- /

- BOVESPA:EGIE3

These 4 Measures Indicate That Engie Brasil Energia (BVMF:EGIE3) Is Using Debt Extensively

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Engie Brasil Energia S.A. (BVMF:EGIE3) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Engie Brasil Energia

What Is Engie Brasil Energia's Debt?

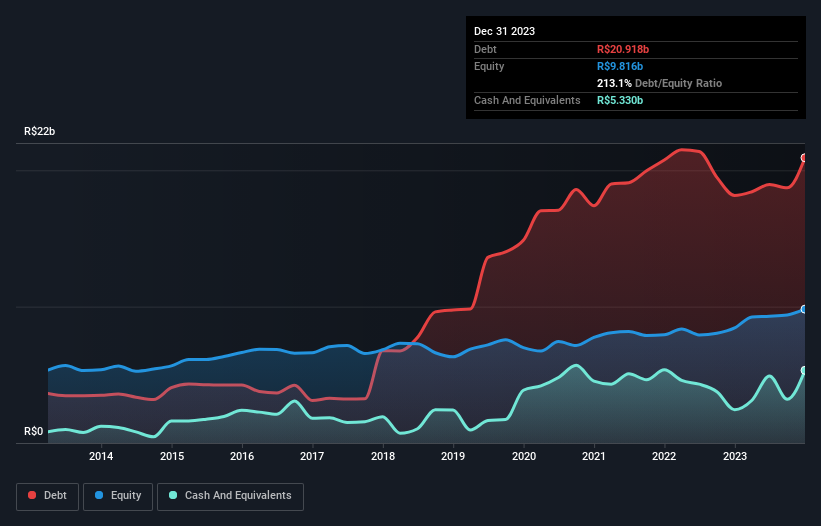

You can click the graphic below for the historical numbers, but it shows that as of December 2023 Engie Brasil Energia had R$20.9b of debt, an increase on R$18.2b, over one year. However, because it has a cash reserve of R$5.33b, its net debt is less, at about R$15.6b.

How Strong Is Engie Brasil Energia's Balance Sheet?

The latest balance sheet data shows that Engie Brasil Energia had liabilities of R$6.11b due within a year, and liabilities of R$26.3b falling due after that. Offsetting these obligations, it had cash of R$5.33b as well as receivables valued at R$2.32b due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by R$24.8b.

This is a mountain of leverage relative to its market capitalization of R$32.7b. This suggests shareholders would be heavily diluted if the company needed to shore up its balance sheet in a hurry.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Engie Brasil Energia has net debt worth 2.5 times EBITDA, which isn't too much, but its interest cover looks a bit on the low side, with EBIT at only 2.8 times the interest expense. While that doesn't worry us too much, it does suggest the interest payments are somewhat of a burden. We saw Engie Brasil Energia grow its EBIT by 4.8% in the last twelve months. Whilst that hardly knocks our socks off it is a positive when it comes to debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Engie Brasil Energia's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Engie Brasil Energia's free cash flow amounted to 28% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

To be frank both Engie Brasil Energia's level of total liabilities and its track record of covering its interest expense with its EBIT make us rather uncomfortable with its debt levels. Having said that, its ability to grow its EBIT isn't such a worry. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Engie Brasil Energia stock a bit risky. Some people like that sort of risk, but we're mindful of the potential pitfalls, so we'd probably prefer it carry less debt. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 2 warning signs for Engie Brasil Energia (1 can't be ignored) you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Engie Brasil Energia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:EGIE3

Engie Brasil Energia

Generates, sells, and trades in electrical energy in Brazil.

Good value slight.

Similar Companies

Market Insights

Community Narratives