Advertisement

- Brazil

- /

- Marine and Shipping

- /

- BOVESPA:HBSA3

Health Check: How Prudently Does Hidrovias do Brasil (BVMF:HBSA3) Use Debt?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Hidrovias do Brasil S.A. (BVMF:HBSA3) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Hidrovias do Brasil

How Much Debt Does Hidrovias do Brasil Carry?

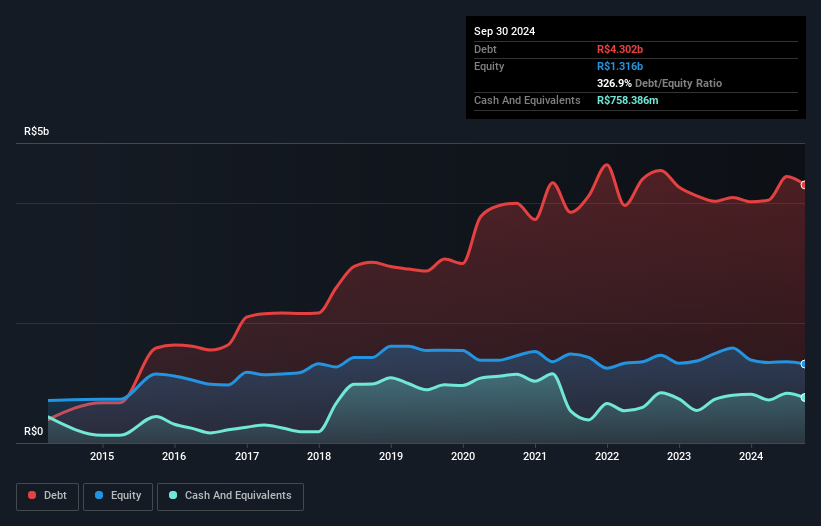

As you can see below, at the end of September 2024, Hidrovias do Brasil had R$4.30b of debt, up from R$4.09b a year ago. Click the image for more detail. However, because it has a cash reserve of R$758.4m, its net debt is less, at about R$3.54b.

A Look At Hidrovias do Brasil's Liabilities

The latest balance sheet data shows that Hidrovias do Brasil had liabilities of R$1.64b due within a year, and liabilities of R$3.55b falling due after that. Offsetting this, it had R$758.4m in cash and R$375.5m in receivables that were due within 12 months. So its liabilities total R$4.05b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the R$2.28b company, like a colossus towering over mere mortals. So we definitely think shareholders need to watch this one closely. After all, Hidrovias do Brasil would likely require a major re-capitalisation if it had to pay its creditors today. There's no doubt that we learn most about debt from the balance sheet. But it is future earnings, more than anything, that will determine Hidrovias do Brasil's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Hidrovias do Brasil had a loss before interest and tax, and actually shrunk its revenue by 18%, to R$1.7b. That's not what we would hope to see.

Caveat Emptor

Not only did Hidrovias do Brasil's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). To be specific the EBIT loss came in at R$40m. Considering that alongside the liabilities mentioned above make us nervous about the company. It would need to improve its operations quickly for us to be interested in it. It's fair to say the loss of R$367m didn't encourage us either; we'd like to see a profit. In the meantime, we consider the stock to be risky. For riskier companies like Hidrovias do Brasil I always like to keep an eye on the long term profit and revenue trends. Fortunately, you can click to see our interactive graph of its profit, revenue, and operating cashflow.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Hidrovias do Brasil might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:HBSA3

Hidrovias do Brasil

An integrated logistics solutions company in Brazil and internationally.

High growth potential and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|20.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|87.5% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor