Advertisement

- Brazil

- /

- Specialty Stores

- /

- BOVESPA:WEST3

Analyst Forecasts Just Became More Bearish On Westwing Comércio Varejista S.A. (BVMF:WEST3)

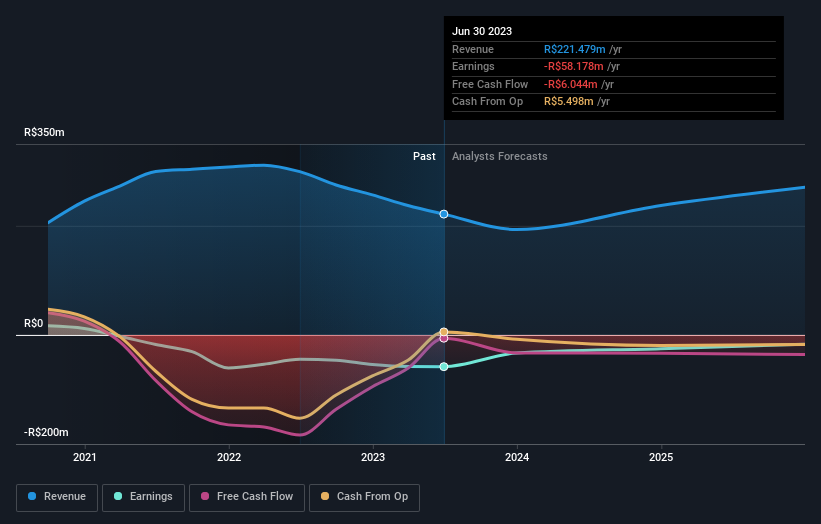

Today is shaping up negative for Westwing Comércio Varejista S.A. (BVMF:WEST3) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. This report focused on revenue estimates, and it looks as though the consensus view of the business has become substantially more conservative.

After the downgrade, the consensus from Westwing Comércio Varejista's three analysts is for revenues of R$193m in 2023, which would reflect an uncomfortable 13% decline in sales compared to the last year of performance. Before the latest update, the analysts were foreseeing R$227m of revenue in 2023. The consensus view seems to have become more pessimistic on Westwing Comércio Varejista, noting the substantial drop in revenue estimates in this update.

Check out our latest analysis for Westwing Comércio Varejista

The consensus price target rose 27% to R$2.10, with the analysts clearly more optimistic about Westwing Comércio Varejista's prospects following this update.

Of course, another way to look at these forecasts is to place them into context against the industry itself. Over the past three years, revenues have declined around 0.7% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 24% decline in revenue until the end of 2023. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 4.7% per year. So while a broad number of companies are forecast to grow, unfortunately Westwing Comércio Varejista is expected to see its sales affected worse than other companies in the industry.

The Bottom Line

The clear low-light was that analysts slashing their revenue forecasts for Westwing Comércio Varejista this year. They're also anticipating slower revenue growth than the wider market. There was also an increase in the price target, suggesting that there is more optimism baked into the forecasts than there was previously. Given the stark change in sentiment, we'd understand if investors became more cautious on Westwing Comércio Varejista after today.

But wait - there's more! We have estimates for Westwing Comércio Varejista from its three analysts out until 2025, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Westwing Comércio Varejista might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:WEST3

Westwing Comércio Varejista

Operates as a shopping e-commerce company in Brazil.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor