Advertisement

Analyst Forecasts Just Became More Bearish On Wiz Soluções e Corretagem de Seguros S.A. (BVMF:WIZS3)

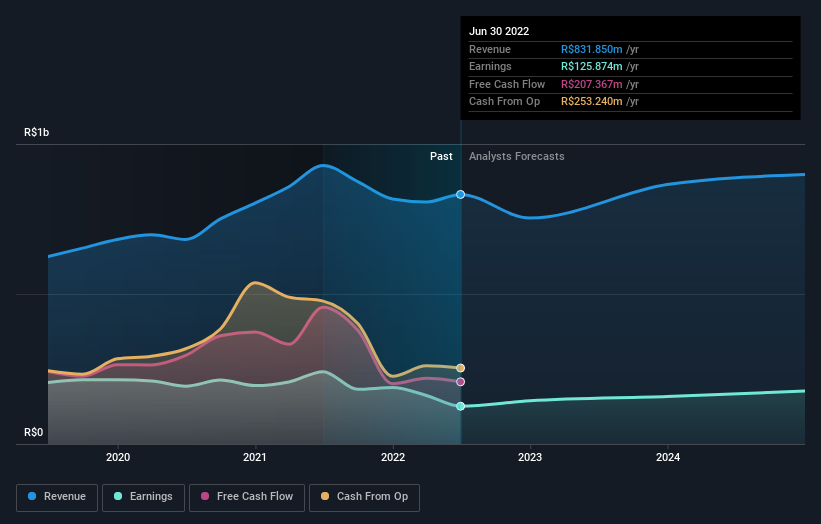

Today is shaping up negative for Wiz Soluções e Corretagem de Seguros S.A. (BVMF:WIZS3) shareholders, with the analysts delivering a substantial negative revision to this year's forecasts. Revenue estimates were cut sharply as the analysts signalled a weaker outlook - perhaps a sign that investors should temper their expectations as well.

After the downgrade, the consensus from Wiz Soluções e Corretagem de Seguros' two analysts is for revenues of R$780m in 2022, which would reflect a noticeable 6.2% decline in sales compared to the last year of performance. Before the latest update, the analysts were foreseeing R$865m of revenue in 2022. It looks like the analysts have become a bit less bullish on Wiz Soluções e Corretagem de Seguros, given the modest decline in revenue estimates after the latest consensus updates.

Check out our latest analysis for Wiz Soluções e Corretagem de Seguros

The consensus price target rose 5.3% to R$15.17, with the analysts clearly more optimistic about Wiz Soluções e Corretagem de Seguros' prospects following this update. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Wiz Soluções e Corretagem de Seguros, with the most bullish analyst valuing it at R$23.00 and the most bearish at R$11.00 per share. This is a fairly broad spread of estimates, suggesting that the analysts are forecasting a wide range of possible outcomes for the business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. These estimates imply that sales are expected to slow, with a forecast annualised revenue decline of 12% by the end of 2022. This indicates a significant reduction from annual growth of 12% over the last five years. Compare this with our data, which suggests that other companies in the same industry are, in aggregate, expected to see their revenue grow 9.3% per year. So although its revenues are forecast to shrink, this cloud does not come with a silver lining - Wiz Soluções e Corretagem de Seguros is expected to lag the wider industry.

The Bottom Line

The most important thing to take away is that analysts cut their revenue estimates for this year. They also expect company revenue to perform worse than the wider market. There was also a nice increase in the price target, with analysts apparently feeling that the intrinsic value of the business is improving. Often, one downgrade can set off a daisy-chain of cuts, especially if an industry is in decline. So we wouldn't be surprised if the market became a lot more cautious on Wiz Soluções e Corretagem de Seguros after today.

Of course, there's always more to the story. At least one of Wiz Soluções e Corretagem de Seguros' two analysts has provided estimates out to 2024, which can be seen for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Wiz Co Participações e Corretagem de Seguros might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:WIZC3

Wiz Co Participações e Corretagem de Seguros

Wiz Co Participações e Corretagem de Seguros S.A.

Adequate balance sheet and fair value.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor