- Brazil

- /

- Healthcare Services

- /

- BOVESPA:VVEO3

CM Hospitalar S/A (BVMF:VVEO3) Posted Healthy Earnings But There Are Some Other Factors To Be Aware Of

Despite announcing strong earnings, CM Hospitalar S/A's (BVMF:VVEO3) stock was sluggish. We think that the market might be paying attention to some underlying factors that they find to be concerning.

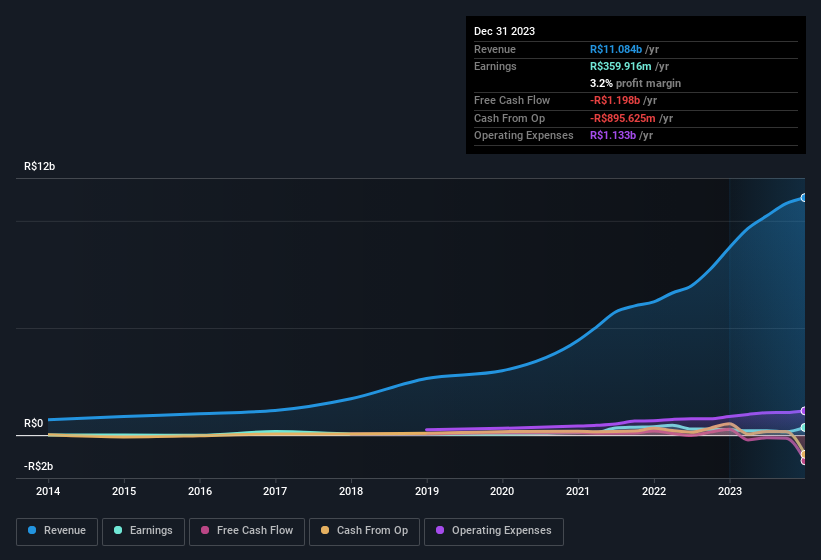

See our latest analysis for CM Hospitalar S/A

Zooming In On CM Hospitalar S/A's Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While it's not a problem to have a positive accrual ratio, indicating a certain level of non-cash profits, a high accrual ratio is arguably a bad thing, because it indicates paper profits are not matched by cash flow. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

For the year to December 2023, CM Hospitalar S/A had an accrual ratio of 0.34. We can therefore deduce that its free cash flow fell well short of covering its statutory profit, suggesting we might want to think twice before putting a lot of weight on the latter. Over the last year it actually had negative free cash flow of R$1.2b, in contrast to the aforementioned profit of R$359.9m. It's worth noting that CM Hospitalar S/A generated positive FCF of R$273m a year ago, so at least they've done it in the past. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings. One positive for CM Hospitalar S/A shareholders is that it's accrual ratio was significantly better last year, providing reason to believe that it may return to stronger cash conversion in the future. Shareholders should look for improved cashflow relative to profit in the current year, if that is indeed the case.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

In order to understand the potential for per share returns, it is essential to consider how much a company is diluting shareholders. In fact, CM Hospitalar S/A increased the number of shares on issue by 13% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. Per share metrics like EPS help us understand how much actual shareholders are benefitting from the company's profits, while the net income level gives us a better view of the company's absolute size. Check out CM Hospitalar S/A's historical EPS growth by clicking on this link.

A Look At The Impact Of CM Hospitalar S/A's Dilution On Its Earnings Per Share (EPS)

As you can see above, CM Hospitalar S/A has been growing its net income over the last few years, with an annualized gain of 196% over three years. But EPS was only up 121% per year, in the exact same period. And the 39% profit boost in the last year certainly seems impressive at first glance. On the other hand, earnings per share are only up 31% in that time. So you can see that the dilution has had a bit of an impact on shareholders.

In the long term, earnings per share growth should beget share price growth. So it will certainly be a positive for shareholders if CM Hospitalar S/A can grow EPS persistently. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For the ordinary retail shareholder, EPS is a great measure to check your hypothetical "share" of the company's profit.

Our Take On CM Hospitalar S/A's Profit Performance

In conclusion, CM Hospitalar S/A has weak cashflow relative to earnings, which indicates lower quality earnings, and the dilution means its earnings per share growth is weaker than its profit growth. For the reasons mentioned above, we think that a perfunctory glance at CM Hospitalar S/A's statutory profits might make it look better than it really is on an underlying level. So while earnings quality is important, it's equally important to consider the risks facing CM Hospitalar S/A at this point in time. To that end, you should learn about the 5 warning signs we've spotted with CM Hospitalar S/A (including 3 which are significant).

Our examination of CM Hospitalar S/A has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:VVEO3

CM Hospitalar S/A

Engages in the distribution of hospital materials, medicines, and nutrition products in Brazil.

Undervalued with moderate growth potential.