Is Três Tentos Agroindustrial S/A (BVMF:TTEN3) Using Too Much Debt?

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Três Tentos Agroindustrial S/A (BVMF:TTEN3) does carry debt. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Três Tentos Agroindustrial S/A

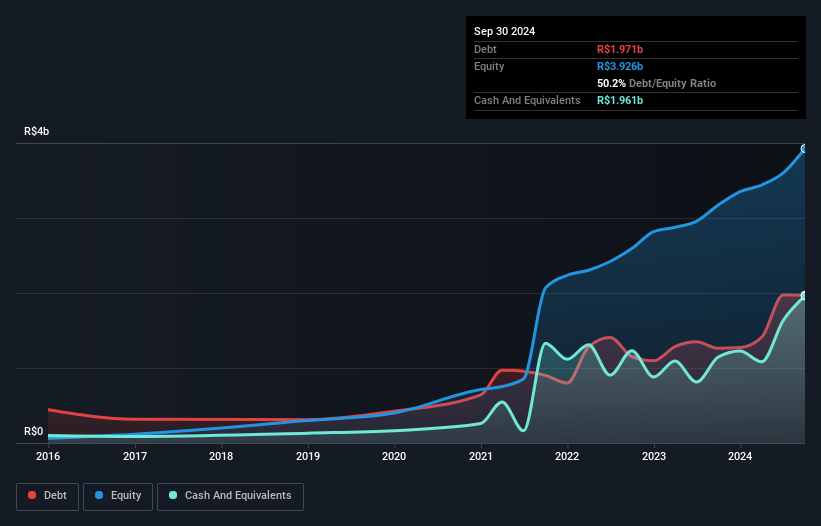

What Is Três Tentos Agroindustrial S/A's Net Debt?

As you can see below, at the end of September 2024, Três Tentos Agroindustrial S/A had R$1.97b of debt, up from R$1.26b a year ago. Click the image for more detail. However, because it has a cash reserve of R$1.96b, its net debt is less, at about R$9.80m.

How Strong Is Três Tentos Agroindustrial S/A's Balance Sheet?

We can see from the most recent balance sheet that Três Tentos Agroindustrial S/A had liabilities of R$3.39b falling due within a year, and liabilities of R$1.22b due beyond that. On the other hand, it had cash of R$1.96b and R$1.16b worth of receivables due within a year. So its liabilities total R$1.49b more than the combination of its cash and short-term receivables.

Since publicly traded Três Tentos Agroindustrial S/A shares are worth a total of R$7.82b, it seems unlikely that this level of liabilities would be a major threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. But either way, Três Tentos Agroindustrial S/A has virtually no net debt, so it's fair to say it does not have a heavy debt load!

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With debt at a measly 0.0088 times EBITDA and EBIT covering interest a whopping 42.6 times, it's clear that Três Tentos Agroindustrial S/A is not a desperate borrower. So relative to past earnings, the debt load seems trivial. In addition to that, we're happy to report that Três Tentos Agroindustrial S/A has boosted its EBIT by 87%, thus reducing the spectre of future debt repayments. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Três Tentos Agroindustrial S/A can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Considering the last three years, Três Tentos Agroindustrial S/A actually recorded a cash outflow, overall. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Our View

Happily, Três Tentos Agroindustrial S/A's impressive interest cover implies it has the upper hand on its debt. But we must concede we find its conversion of EBIT to free cash flow has the opposite effect. Looking at all the aforementioned factors together, it strikes us that Três Tentos Agroindustrial S/A can handle its debt fairly comfortably. On the plus side, this leverage can boost shareholder returns, but the potential downside is more risk of loss, so it's worth monitoring the balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 1 warning sign for Três Tentos Agroindustrial S/A that you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Três Tentos Agroindustrial S/A might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:TTEN3

Três Tentos Agroindustrial S/A

Operates in the agribusiness sector in Brazil.

Flawless balance sheet and fair value.

Market Insights

Community Narratives