- Brazil

- /

- Oil and Gas

- /

- BOVESPA:BRAV3

3R Petroleum Óleo e Gás S.A. Just Missed Earnings - But Analysts Have Updated Their Models

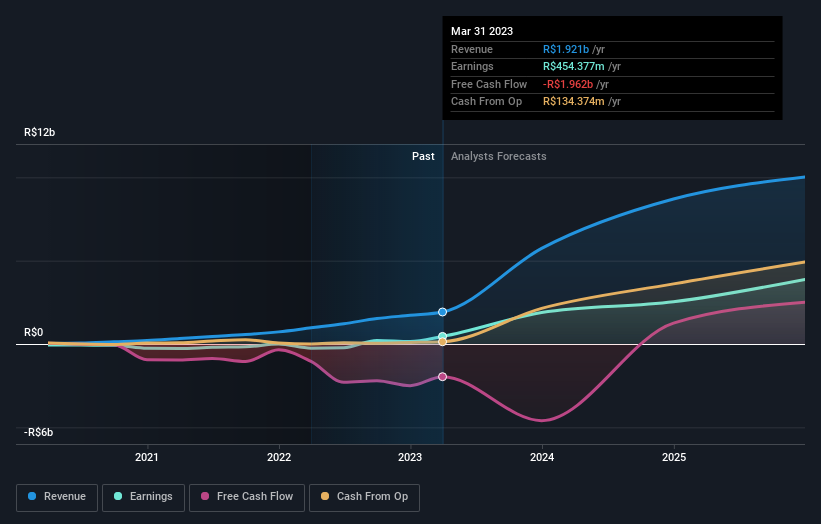

As you might know, 3R Petroleum Óleo e Gás S.A. (BVMF:RRRP3) last week released its latest first-quarter, and things did not turn out so great for shareholders. It wasn't a great result overall - while revenue fell marginally short of analyst estimates at R$574m, statutory earnings missed forecasts by an incredible 82%, coming in at just R$0.06 per share. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

View our latest analysis for 3R Petroleum Óleo e Gás

Following the latest results, 3R Petroleum Óleo e Gás' nine analysts are now forecasting revenues of R$5.73b in 2023. This would be a substantial 198% improvement in sales compared to the last 12 months. Per-share earnings are expected to shoot up 212% to R$6.98. Before this earnings report, the analysts had been forecasting revenues of R$5.75b and earnings per share (EPS) of R$7.89 in 2023. So there's definitely been a decline in sentiment after the latest results, noting the substantial drop in new EPS forecasts.

It might be a surprise to learn that the consensus price target was broadly unchanged at R$75.79, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic 3R Petroleum Óleo e Gás analyst has a price target of R$106 per share, while the most pessimistic values it at R$56.00. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the 3R Petroleum Óleo e Gás' past performance and to peers in the same industry. It's clear from the latest estimates that 3R Petroleum Óleo e Gás' rate of growth is expected to accelerate meaningfully, with the forecast 3x annualised revenue growth to the end of 2023 noticeably faster than its historical growth of 87% p.a. over the past three years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue shrink 2.7% per year. It seems obvious that as part of the brighter growth outlook, 3R Petroleum Óleo e Gás is expected to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for 3R Petroleum Óleo e Gás. Fortunately, they also reconfirmed their revenue estimates, suggesting sales are tracking in line with expectations. Their estimates also suggest that 3R Petroleum Óleo e Gás' revenues are expected to perform better than the wider industry. The consensus price target held steady at R$75.79, with the latest estimates not enough to have an impact on their price targets.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. We have forecasts for 3R Petroleum Óleo e Gás going out to 2025, and you can see them free on our platform here.

You still need to take note of risks, for example - 3R Petroleum Óleo e Gás has 2 warning signs (and 1 which is a bit concerning) we think you should know about.

Valuation is complex, but we're here to simplify it.

Discover if Brava Energia might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:BRAV3

Brava Energia

Engages in the exploration and production of oil and natural gas in Brazil.

High growth potential and fair value.

Market Insights

Community Narratives