Advertisement

- Brazil

- /

- Oil and Gas

- /

- BOVESPA:ENAT3

These Analysts Think Enauta Participações S.A.'s (BVMF:ENAT3) Sales Are Under Threat

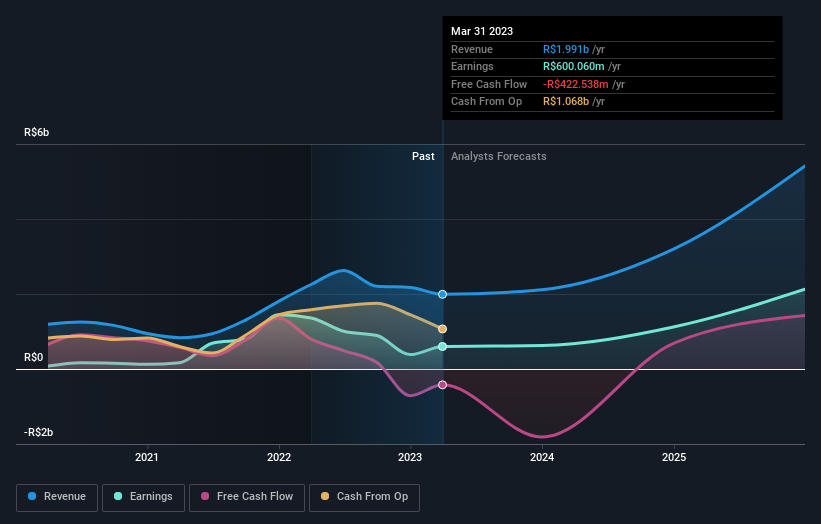

The analysts covering Enauta Participações S.A. (BVMF:ENAT3) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for this year. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic.

Following the downgrade, the most recent consensus for Enauta Participações from its five analysts is for revenues of R$2.1b in 2023 which, if met, would be an okay 6.2% increase on its sales over the past 12 months. Before the latest update, the analysts were foreseeing R$2.5b of revenue in 2023. The consensus view seems to have become more pessimistic on Enauta Participações, noting the substantial drop in revenue estimates in this update.

View our latest analysis for Enauta Participações

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Enauta Participações' revenue growth will slow down substantially, with revenues to the end of 2023 expected to display 8.3% growth on an annualised basis. This is compared to a historical growth rate of 27% over the past five years. Compare this with other companies in the same industry, which are forecast to see a revenue decline of 2.9% annually. So it's clear that despite the slowdown in growth, Enauta Participações is still expected to grow meaningfully faster than the wider industry.

The Bottom Line

The clear low-light was that analysts slashing their revenue forecasts for Enauta Participações this year. They're also forecasting for revenues to perform better than companies in the wider market. Given the stark change in sentiment, we'd understand if investors became more cautious on Enauta Participações after today.

So things certainly aren't looking great, and you should also know that we've spotted some potential warning signs with Enauta Participações, including its declining profit margins. For more information, you can click here to discover this and the 1 other risk we've identified.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Enauta Participações might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:ENAT3

Enauta Participações

Engages in the exploration, production, and sale of oil and natural gas in Brazil.

High growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative