Advertisement

- Brazil

- /

- Diversified Financial

- /

- BOVESPA:CSUD3

If EPS Growth Is Important To You, CSU Digital (BVMF:CSUD3) Presents An Opportunity

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But the reality is that when a company loses money each year, for long enough, its investors will usually take their share of those losses. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

In contrast to all that, many investors prefer to focus on companies like CSU Digital (BVMF:CSUD3), which has not only revenues, but also profits. Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

See our latest analysis for CSU Digital

How Quickly Is CSU Digital Increasing Earnings Per Share?

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. So it makes sense that experienced investors pay close attention to company EPS when undertaking investment research. It certainly is nice to see that CSU Digital has managed to grow EPS by 28% per year over three years. If growth like this continues on into the future, then shareholders will have plenty to smile about.

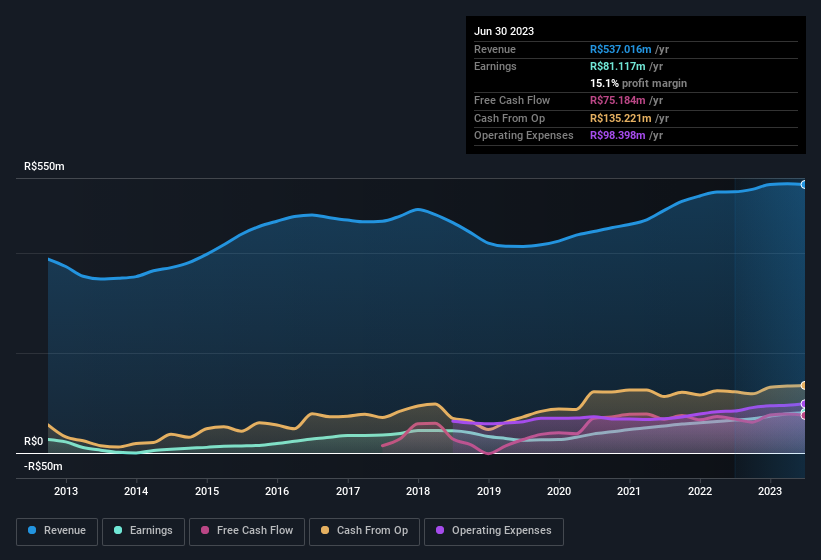

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. While we note CSU Digital achieved similar EBIT margins to last year, revenue grew by a solid 2.8% to R$537m. That's progress.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

Since CSU Digital is no giant, with a market capitalisation of R$705m, you should definitely check its cash and debt before getting too excited about its prospects.

Are CSU Digital Insiders Aligned With All Shareholders?

Seeing insiders owning a large portion of the shares on issue is often a good sign. Their incentives will be aligned with the investors and there's less of a probability in a sudden sell-off that would impact the share price. So we're pleased to report that CSU Digital insiders own a meaningful share of the business. To be exact, company insiders hold 55% of the company, so their decisions have a significant impact on their investments. This should be seen as a good thing, as it means insiders have a personal interest in delivering the best outcomes for shareholders. With that sort of holding, insiders have about R$387m riding on the stock, at current prices. That's nothing to sneeze at!

Does CSU Digital Deserve A Spot On Your Watchlist?

You can't deny that CSU Digital has grown its earnings per share at a very impressive rate. That's attractive. This EPS growth rate is something the company should be proud of, and so it's no surprise that insiders are holding on to a considerable chunk of shares. The growth and insider confidence is looked upon well and so it's worthwhile to investigate further with a view to discern the stock's true value. It is worth noting though that we have found 1 warning sign for CSU Digital that you need to take into consideration.

Although CSU Digital certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see insider buying, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:CSUD3

CSU Digital

A technology company for financial services, provides digital solutions for payments, embedded finance, customer experience, and loyalty and incentive programs in Brazil.

Flawless balance sheet average dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor