Advertisement

- Brazil

- /

- Capital Markets

- /

- BOVESPA:B3SA3

Investor Optimism Abounds B3 S.A. - Brasil, Bolsa, Balcão (BVMF:B3SA3) But Growth Is Lacking

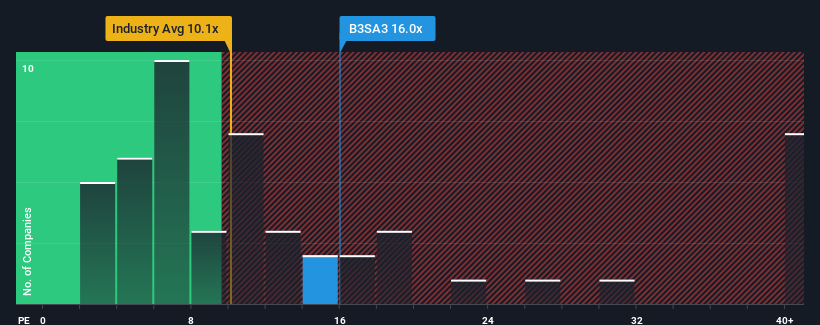

B3 S.A. - Brasil, Bolsa, Balcão's (BVMF:B3SA3) price-to-earnings (or "P/E") ratio of 16x might make it look like a strong sell right now compared to the market in Brazil, where around half of the companies have P/E ratios below 10x and even P/E's below 7x are quite common. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly elevated P/E.

Recent times haven't been advantageous for B3 - Brasil Bolsa Balcão as its earnings have been rising slower than most other companies. It might be that many expect the uninspiring earnings performance to recover significantly, which has kept the P/E from collapsing. If not, then existing shareholders may be very nervous about the viability of the share price.

Check out our latest analysis for B3 - Brasil Bolsa Balcão

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like B3 - Brasil Bolsa Balcão's to be considered reasonable.

If we review the last year of earnings, the company posted a result that saw barely any deviation from a year ago. Fortunately, a few good years before that means that it was still able to grow EPS by 8.7% in total over the last three years. Accordingly, shareholders probably wouldn't have been overly satisfied with the unstable medium-term growth rates.

Turning to the outlook, the next three years should generate growth of 14% per annum as estimated by the eleven analysts watching the company. That's shaping up to be similar to the 16% per annum growth forecast for the broader market.

In light of this, it's curious that B3 - Brasil Bolsa Balcão's P/E sits above the majority of other companies. Apparently many investors in the company are more bullish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for disappointment if the P/E falls to levels more in line with the growth outlook.

The Final Word

It's argued the price-to-earnings ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

We've established that B3 - Brasil Bolsa Balcão currently trades on a higher than expected P/E since its forecast growth is only in line with the wider market. When we see an average earnings outlook with market-like growth, we suspect the share price is at risk of declining, sending the high P/E lower. This places shareholders' investments at risk and potential investors in danger of paying an unnecessary premium.

Before you take the next step, you should know about the 1 warning sign for B3 - Brasil Bolsa Balcão that we have uncovered.

Of course, you might also be able to find a better stock than B3 - Brasil Bolsa Balcão. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Valuation is complex, but we're here to simplify it.

Discover if B3 - Brasil Bolsa Balcão might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:B3SA3

B3 - Brasil Bolsa Balcão

A financial market infrastructure company, provides trading services in an exchange and OTC environment.

Outstanding track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor