Advertisement

Earnings Miss: Vivara Participações S.A. Missed EPS By 61% And Analysts Are Revising Their Forecasts

It's been a good week for Vivara Participações S.A. (BVMF:VIVA3) shareholders, because the company has just released its latest first-quarter results, and the shares gained 7.7% to R$24.32. It looks like a pretty bad result, all things considered. Although revenues of R$445m were in line with analyst predictions, statutory earnings fell badly short, missing estimates by 61% to hit R$0.15 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Vivara Participações after the latest results.

Check out our latest analysis for Vivara Participações

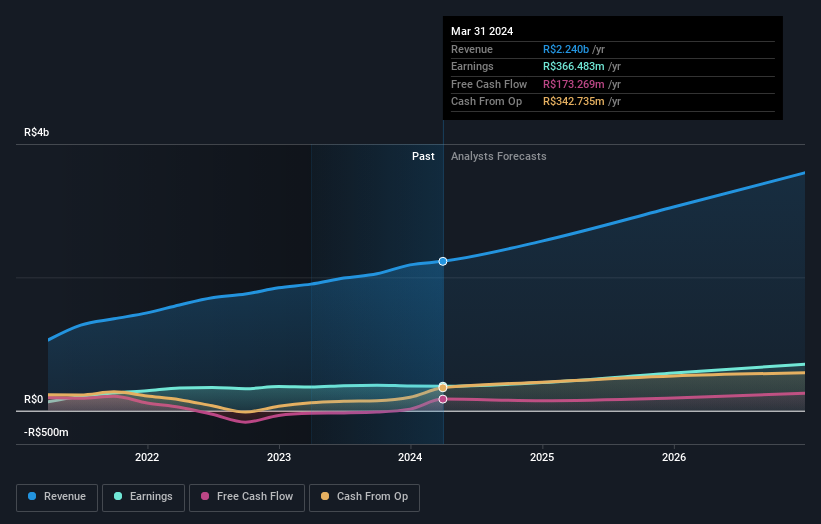

Following the latest results, Vivara Participações' nine analysts are now forecasting revenues of R$2.54b in 2024. This would be a meaningful 14% improvement in revenue compared to the last 12 months. Statutory earnings per share are predicted to climb 14% to R$1.78. Before this earnings report, the analysts had been forecasting revenues of R$2.55b and earnings per share (EPS) of R$1.95 in 2024. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analysts did make a minor downgrade to their earnings per share forecasts.

The average price target fell 5.9% to R$35.14, with reduced earnings forecasts clearly tied to a lower valuation estimate. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values Vivara Participações at R$39.00 per share, while the most bearish prices it at R$30.00. This is a very narrow spread of estimates, implying either that Vivara Participações is an easy company to value, or - more likely - the analysts are relying heavily on some key assumptions.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We can infer from the latest estimates that forecasts expect a continuation of Vivara Participações'historical trends, as the 18% annualised revenue growth to the end of 2024 is roughly in line with the 17% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 10% annually. So although Vivara Participações is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Vivara Participações. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Vivara Participações' future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Vivara Participações going out to 2026, and you can see them free on our platform here..

Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Vivara Participações that you should be aware of.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:VIVA3

Vivara Participações

Engages in the manufacture and sale of jewelry and other articles in Latin America.

Undervalued with solid track record.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor