- Brazil

- /

- Commercial Services

- /

- BOVESPA:AMBP3

Market Participants Recognise Ambipar Participações e Empreendimentos S.A.'s (BVMF:AMBP3) Revenues Pushing Shares 27% Higher

Ambipar Participações e Empreendimentos S.A. (BVMF:AMBP3) shares have continued their recent momentum with a 27% gain in the last month alone. This latest share price bounce rounds out a remarkable 925% gain over the last twelve months.

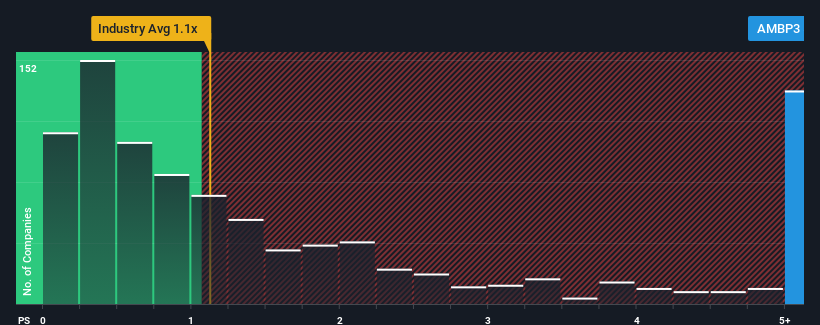

Following the firm bounce in price, given around half the companies in Brazil's Commercial Services industry have price-to-sales ratios (or "P/S") below 0.9x, you may consider Ambipar Participações e Empreendimentos as a stock to avoid entirely with its 5.2x P/S ratio. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

View our latest analysis for Ambipar Participações e Empreendimentos

What Does Ambipar Participações e Empreendimentos' P/S Mean For Shareholders?

Recent times haven't been great for Ambipar Participações e Empreendimentos as its revenue has been rising slower than most other companies. One possibility is that the P/S ratio is high because investors think this lacklustre revenue performance will improve markedly. If not, then existing shareholders may be very nervous about the viability of the share price.

Keen to find out how analysts think Ambipar Participações e Empreendimentos' future stacks up against the industry? In that case, our free report is a great place to start.Is There Enough Revenue Growth Forecasted For Ambipar Participações e Empreendimentos?

In order to justify its P/S ratio, Ambipar Participações e Empreendimentos would need to produce outstanding growth that's well in excess of the industry.

Taking a look back first, we see that the company grew revenue by an impressive 15% last year. This great performance means it was also able to deliver immense revenue growth over the last three years. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 13% per year during the coming three years according to the four analysts following the company. That's shaping up to be materially higher than the 8.9% per year growth forecast for the broader industry.

With this in mind, it's not hard to understand why Ambipar Participações e Empreendimentos' P/S is high relative to its industry peers. It seems most investors are expecting this strong future growth and are willing to pay more for the stock.

The Bottom Line On Ambipar Participações e Empreendimentos' P/S

Shares in Ambipar Participações e Empreendimentos have seen a strong upwards swing lately, which has really helped boost its P/S figure. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our look into Ambipar Participações e Empreendimentos shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. It's hard to see the share price falling strongly in the near future under these circumstances.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Ambipar Participações e Empreendimentos you should know about.

If these risks are making you reconsider your opinion on Ambipar Participações e Empreendimentos, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:AMBP3

Ambipar Participações e Empreendimentos

Ambipar Participações e Empreendimentos S.A.

Mediocre balance sheet and slightly overvalued.

Market Insights

Community Narratives