Advertisement

- Brazil

- /

- Aerospace & Defense

- /

- BOVESPA:EMBR3

Results: Embraer S.A. Exceeded Expectations And The Consensus Has Updated Its Estimates

Embraer S.A. (BVMF:EMBR3) investors will be delighted, with the company turning in some strong numbers with its latest results. The company beat forecasts, with revenue of R$9.2b, some 4.8% above estimates, and statutory earnings per share (EPS) coming in at R$1.33, 293% ahead of expectations. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for Embraer

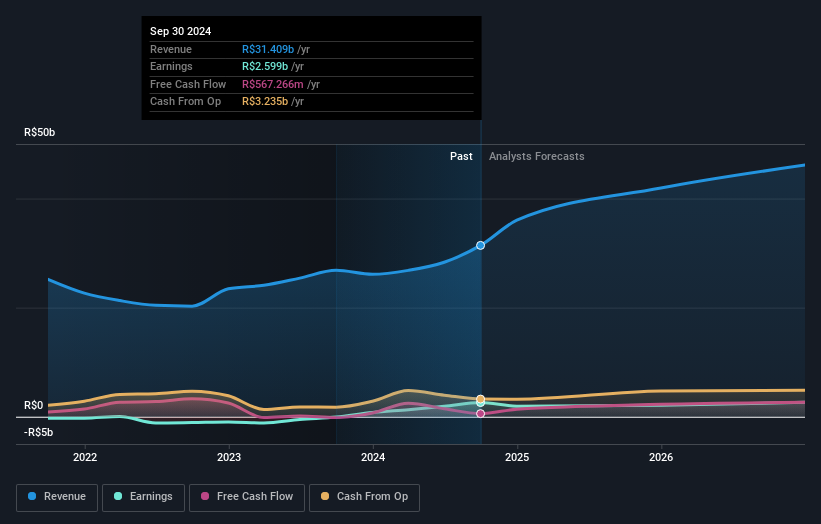

Taking into account the latest results, the consensus forecast from Embraer's 14 analysts is for revenues of R$41.9b in 2025. This reflects a sizeable 33% improvement in revenue compared to the last 12 months. Before this earnings report, the analysts had been forecasting revenues of R$42.1b and earnings per share (EPS) of R$2.95 in 2025. So we can see that while the consensus made no real change to its revenue estimates, it also no longer provides an earnings per share estimate. This suggests that revenues are what the market is focusing on after the latest results.

We'd also point out that thatthe analysts have made no major changes to their price target of R$52.14. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. There are some variant perceptions on Embraer, with the most bullish analyst valuing it at R$66.50 and the most bearish at R$39.89 per share. We would probably assign less value to the analyst forecasts in this situation, because such a wide range of estimates could imply that the future of this business is difficult to value accurately. With this in mind, we wouldn't rely too heavily the consensus price target, as it is just an average and analysts clearly have some deeply divergent views on the business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. The analysts are definitely expecting Embraer's growth to accelerate, with the forecast 26% annualised growth to the end of 2025 ranking favourably alongside historical growth of 8.6% per annum over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 8.5% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Embraer to grow faster than the wider industry.

The Bottom Line

The clear take away from these updates is that the analysts made no change to their revenue estimates for next year, with the business apparently performing in line with their models. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

At least one of Embraer's 14 analysts has provided estimates out to 2026, which can be seen for free on our platform here.

You can also see whether Embraer is carrying too much debt, and whether its balance sheet is healthy, for free on our platform here.

Valuation is complex, but we're here to simplify it.

Discover if Embraer might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BOVESPA:EMBR3

Embraer

Designs, develops, manufactures, and sells aircraft and systems worldwide.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|27.6% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.1% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.0% undervalued

ME

Community Contributor