Advertisement

If we want to find a stock that could multiply over the long term, what are the underlying trends we should look for? Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, we've noticed some promising trends at Tupy (BVMF:TUPY3) so let's look a bit deeper.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Tupy, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

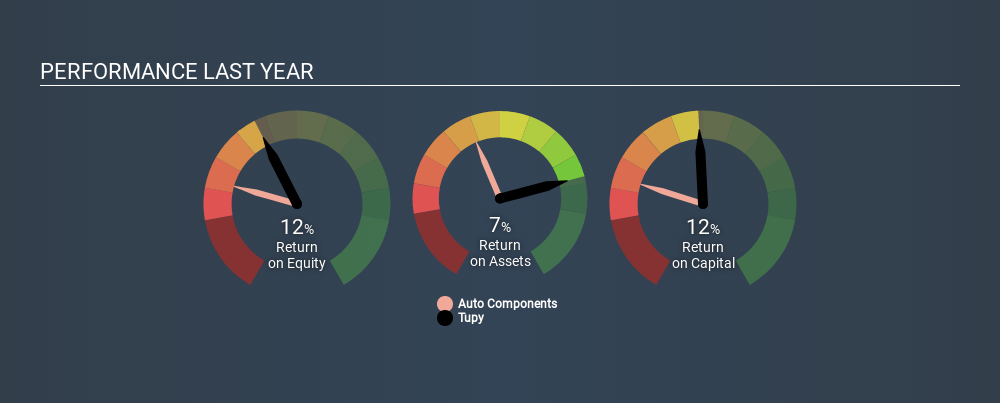

0.12 = R$466m ÷ (R$5.1b - R$1.1b) (Based on the trailing twelve months to December 2019).

Thus, Tupy has an ROCE of 12%. On its own, that's a standard return, however it's much better than the 8.6% generated by the Auto Components industry.

Check out our latest analysis for Tupy

Above you can the how the current ROCE for Tupy's compares to it's prior returns on capital, but you can only tell so much from the past. If you'd like, you can check out the forecasts from the analysts covering Tupy here for free.

So How Is Tupy's ROCE Trending?

Tupy has not disappointed with their ROCE growth. Looking at the data, we can see that even though capital employed in the business has remained relatively flat, the ROCE generated has risen by 62% over the last five years. So our take on this is that the business has increased efficiencies to generate these higher returns, all the while not needing to make any additional investments. It's worth looking deeper into this though because while it's great that the business is more efficient, it might also mean that going forward the areas to invest internally for the organic growth are lacking.

The Bottom Line

To sum it up, Tupy is collecting higher returns from the same amount of capital, and that's impressive. And investors seem to expect more of this going forward, since the stock has rewarded shareholders with a 59% return over the last five years. With that being said, we still think the promising fundamentals mean the company deserves some further due diligence.

One final note, you should learn about the 4 warning signs we've spotted with Tupy (including 1 which is is significant) .

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

When trading Tupy or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account.Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tupy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About BOVESPA:TUPY3

Tupy

Engages in the development, manufacture, and sale of cast and compacted graphite iron structural components in North America, South and Central Americas, Europe, Asia, Africa, Oceania, and internationally.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|35.7% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|20.5% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|25.2% overvalued

DA

Community Contributor