bpost SA/NV (EBR:BPOST), is not the largest company out there, but it saw a decent share price growth in the teens level on the ENXTBR over the last few months. As a mid-cap stock with high coverage by analysts, you could assume any recent changes in the company’s outlook is already priced into the stock. But what if there is still an opportunity to buy? Let’s examine bpost’s valuation and outlook in more detail to determine if there’s still a bargain opportunity.

See our latest analysis for bpost

Is bpost still cheap?

Good news, investors! bpost is still a bargain right now according to my price multiple model, which compares the company's price-to-earnings ratio to the industry average. In this instance, I’ve used the price-to-earnings (PE) ratio given that there is not enough information to reliably forecast the stock’s cash flows. I find that bpost’s ratio of 10.27x is below its peer average of 19.4x, which indicates the stock is trading at a lower price compared to the Logistics industry. What’s more interesting is that, bpost’s share price is quite volatile, which gives us more chances to buy since the share price could sink lower (or rise higher) in the future. This is based on its high beta, which is a good indicator for how much the stock moves relative to the rest of the market.

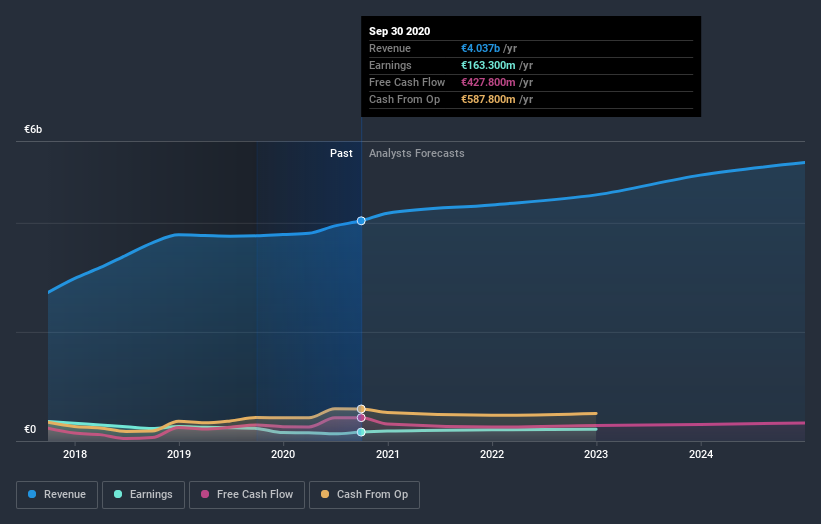

What does the future of bpost look like?

Future outlook is an important aspect when you’re looking at buying a stock, especially if you are an investor looking for growth in your portfolio. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. With profit expected to grow by 30% over the next couple of years, the future seems bright for bpost. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What this means for you:

Are you a shareholder? Since BPOST is currently trading below the industry PE ratio, it may be a great time to increase your holdings in the stock. With an optimistic profit outlook on the horizon, it seems like this growth has not yet been fully factored into the share price. However, there are also other factors such as capital structure to consider, which could explain the current price multiple.

Are you a potential investor? If you’ve been keeping an eye on BPOST for a while, now might be the time to enter the stock. Its buoyant future profit outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy BPOST. But before you make any investment decisions, consider other factors such as the track record of its management team, in order to make a well-informed assessment.

So while earnings quality is important, it's equally important to consider the risks facing bpost at this point in time. For example - bpost has 2 warning signs we think you should be aware of.

If you are no longer interested in bpost, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

If you’re looking to trade bpost, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ENXTBR:BPOST

bpost/SA

Provides mail and parcel services to individuals, businesses, and public institutions in Belgium, rest of Europe, the United States, and internationally.

Good value with moderate growth potential.

Similar Companies

Market Insights

Community Narratives