If you have been keeping an eye on UCB (ENXTBR:UCB), the recent movements in its share price might have raised some questions. Without a big headline event or a significant shift in company operations, you might be wondering whether this momentum is simply a reaction to changing investor sentiment or signals that something deeper is going on. Sometimes a move like this can be a sign the market is anticipating growth or reassessing risk.

Looking at the broader picture, UCB’s stock has not moved in isolation. Over the past year, shares have climbed 30%, and gains have been even more pronounced recently, with a 27% rise in the past three months and strong momentum over the past month as well. The company’s positive revenue and net income growth year over year adds fuel to the conversation, especially for investors paying close attention to the pharmaceutical and biotech space.

So after this extended period of gains, is UCB trading at a bargain, or is the market already factoring future growth into the price?

Advertisement

Most Popular Narrative: 6.5% Undervalued

According to the most widely followed analysis, UCB is currently trading at a notable discount to its fair value estimate. This suggests some upside potential from today’s prices.

“UCB’s deep and advancing innovation pipeline, along with its focus on differentiated products in neurology and immunology, supports the ability to launch multiple new indications, address rare/orphan diseases, and leverage advances in personalized medicine. All of these factors underpin sustained long-term revenue growth and margin expansion.”

Can UCB deliver breakthrough returns and outperform the market? The leading narrative is built around an ambitious sequence of projected earnings growth, margin expansion, and confidence in the company's innovation engine. Want to see which aggressive assumptions are driving the fair value calculation? Explore the narrative's bold blueprint for UCB’s future.

However, significant risks remain, including potential pricing pressure in the U.S. market and looming patent expiries. These factors could impact UCB's long-term growth outlook.

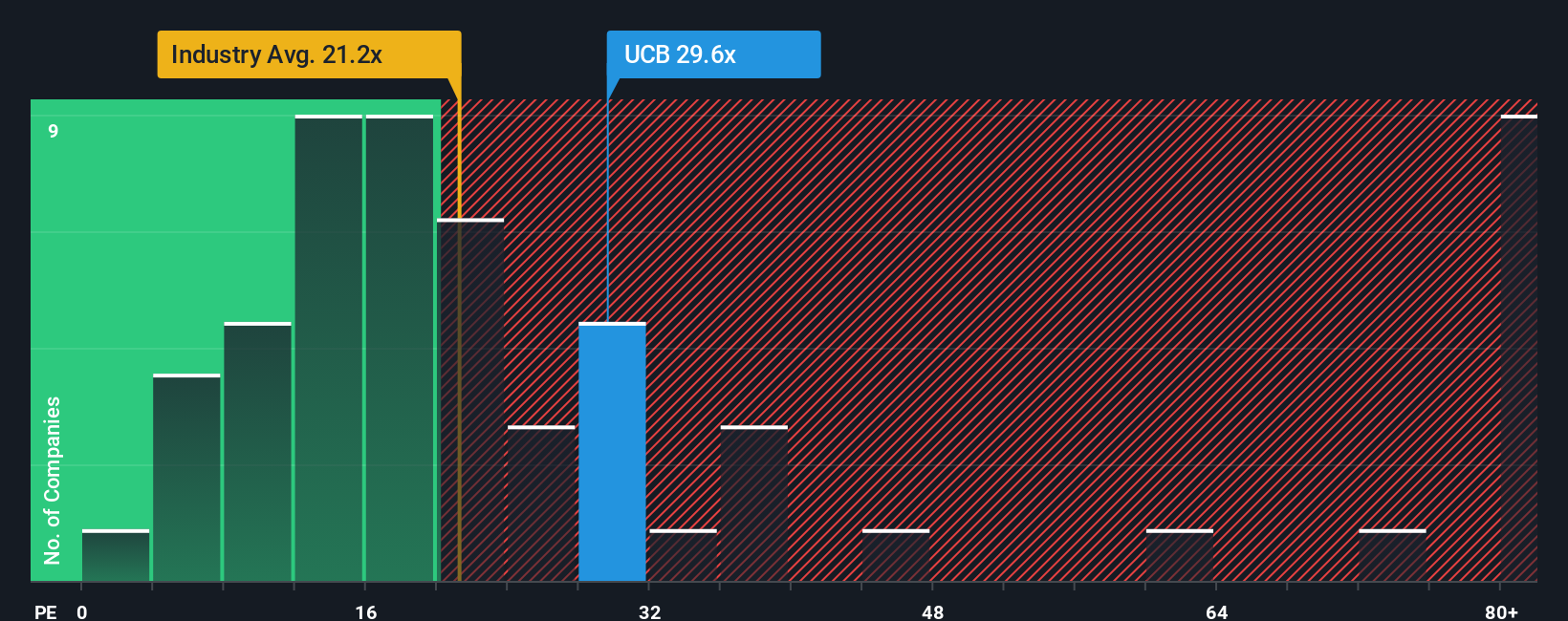

While our first look painted UCB as undervalued, another common approach reveals a different story. Compared to others in its sector, UCB’s current share price appears more expensive. Which narrative will prove right?

Stay updated when valuation signals shift by adding UCB to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own UCB Narrative

For those who want to dig into the numbers and shape their own story, the tools are available to piece together a complete perspective in just a few minutes. Do it your way

Why settle for one strong idea when you could put your capital to work in other promising themes? The market's most exciting opportunities are just a click away.

Boost your income focus, and find shares with consistently high payouts by using our selection of dividend stocks with yields > 3%.

Ride the AI wave and tap into companies set to benefit from emerging technology. See this handpicked group of AI penny stocks.

Unearth hidden gems trading below their worth by checking stocks that stand out for value with our tailored list of undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield) • Undervalued Small Caps with Insider Buying • High growth Tech and AI Companies

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.