Advertisement

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. With that in mind, we've noticed some promising trends at Duxton Water (ASX:D2O) so let's look a bit deeper.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for Duxton Water:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

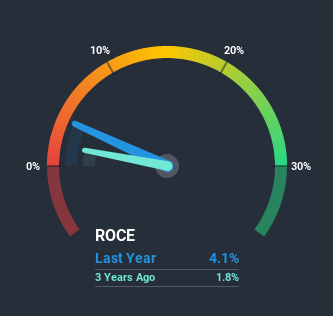

0.041 = AU$9.7m ÷ (AU$245m - AU$8.8m) (Based on the trailing twelve months to June 2020).

So, Duxton Water has an ROCE of 4.1%. In absolute terms, that's a low return and it also under-performs the Water Utilities industry average of 6.1%.

See our latest analysis for Duxton Water

In the above chart we have measured Duxton Water's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Duxton Water.

What Does the ROCE Trend For Duxton Water Tell Us?

Even though ROCE is still low in absolute terms, it's good to see it's heading in the right direction. The data shows that returns on capital have increased substantially over the last three years to 4.1%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 219%. So we're very much inspired by what we're seeing at Duxton Water thanks to its ability to profitably reinvest capital.

The Bottom Line On Duxton Water's ROCE

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what Duxton Water has. And with a respectable 42% awarded to those who held the stock over the last three years, you could argue that these developments are starting to get the attention they deserve. In light of that, we think it's worth looking further into this stock because if Duxton Water can keep these trends up, it could have a bright future ahead.

Duxton Water does have some risks, we noticed 4 warning signs (and 2 which are concerning) we think you should know about.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you’re looking to trade Duxton Water, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About ASX:RIV

Rivco Australia

Provides water supply solutions to Australian irrigators.

Undervalued with solid track record.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

63 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PicaCoder on Microsoft ·

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value:US$42015.0% overvalued

61 followersusers have followed this narrative

12 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

63 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative