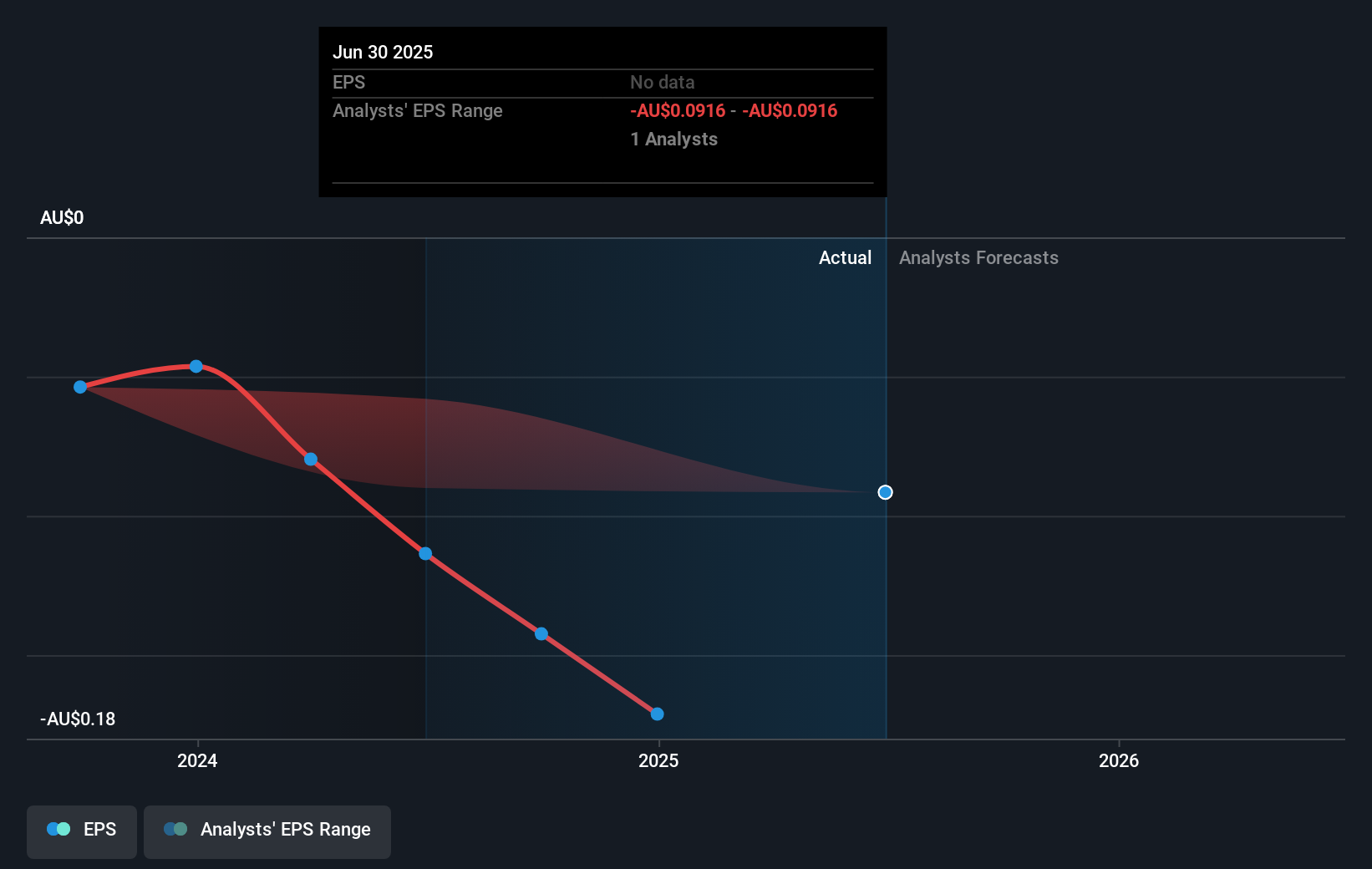

Camplify Holdings Limited (ASX:CHL) is possibly approaching a major achievement in its business, so we would like to shine some light on the company. Camplify Holdings Limited, together with its subsidiaries, operates peer-to-peer digital marketplace platforms to connect recreational vehicle (RV) owners to hirers in Australia, New Zealand, Spain, United Kingdom, Germany, Austria and the Netherlands. On 30 June 2025, the AU$24m market-cap company posted a loss of AU$16m for its most recent financial year. Many investors are wondering about the rate at which Camplify Holdings will turn a profit, with the big question being “when will the company breakeven?” Below we will provide a high-level summary of the industry analysts’ expectations for the company.

Consensus from 2 of the Australian Transportation analysts is that Camplify Holdings is on the verge of breakeven. They anticipate the company to incur a final loss in 2026, before generating positive profits of AU$1.4m in 2027. The company is therefore projected to breakeven around 2 years from today. How fast will the company have to grow each year in order to reach the breakeven point by 2027? Working backwards from analyst estimates, it turns out that they expect the company to grow 117% year-on-year, on average, which is rather optimistic! If this rate turns out to be too aggressive, the company may become profitable much later than analysts predict.

Underlying developments driving Camplify Holdings' growth isn’t the focus of this broad overview, but, bear in mind that typically a high growth rate is not out of the ordinary, particularly when a company is in a period of investment.

View our latest analysis for Camplify Holdings

Before we wrap up, there’s one aspect worth mentioning. Camplify Holdings currently has no debt on its balance sheet, which is rare for a loss-making growth company, which typically has high debt relative to its equity. This means that the company has been operating purely on its equity investment and has no debt burden. This aspect reduces the risk around investing in the loss-making company.

Next Steps:

This article is not intended to be a comprehensive analysis on Camplify Holdings, so if you are interested in understanding the company at a deeper level, take a look at Camplify Holdings' company page on Simply Wall St. We've also put together a list of key aspects you should further examine:

- Valuation: What is Camplify Holdings worth today? Has the future growth potential already been factored into the price? The intrinsic value infographic in our free research report helps visualize whether Camplify Holdings is currently mispriced by the market.

- Management Team: An experienced management team on the helm increases our confidence in the business – take a look at who sits on Camplify Holdings’s board and the CEO’s background.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:CHL

Camplify Holdings

Operates peer-to-peer digital marketplace platforms to connect recreational vehicle (RV) owners to hirers in Australia, New Zealand, Spain, United Kingdom, Germany, Austria and the Netherlands.

Undervalued with reasonable growth potential.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion