Advertisement

We Think Tuas (ASX:TUA) Can Easily Afford To Drive Business Growth

We can readily understand why investors are attracted to unprofitable companies. Indeed, Tuas (ASX:TUA) stock is up 149% in the last year, providing strong gains for shareholders. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

Given its strong share price performance, we think it's worthwhile for Tuas shareholders to consider whether its cash burn is concerning. In this report, we will consider the company's annual negative free cash flow, henceforth referring to it as the 'cash burn'. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

View our latest analysis for Tuas

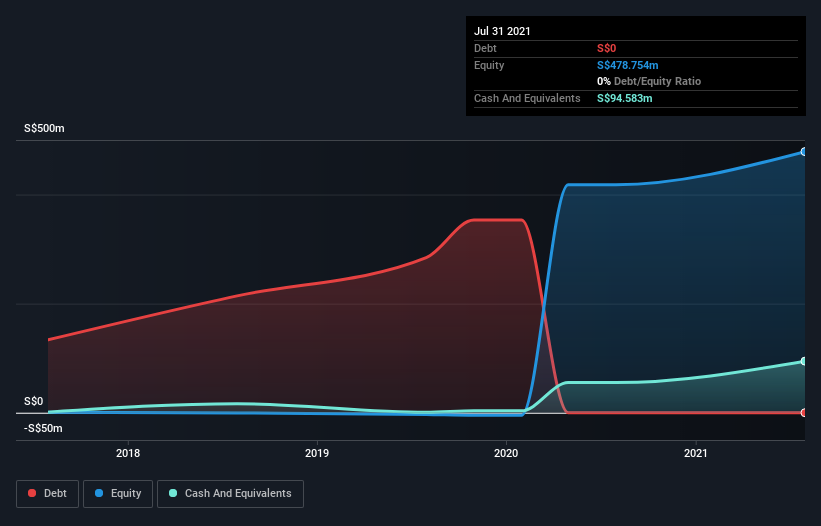

When Might Tuas Run Out Of Money?

A company's cash runway is calculated by dividing its cash hoard by its cash burn. As at July 2021, Tuas had cash of S$95m and no debt. In the last year, its cash burn was S$25m. So it had a cash runway of about 3.7 years from July 2021. There's no doubt that this is a reassuringly long runway. The image below shows how its cash balance has been changing over the last few years.

How Well Is Tuas Growing?

Tuas managed to reduce its cash burn by 74% over the last twelve months, which suggests it's on the right flight path. But its revenue is better yet, flying higher than Elon Musk and his rocket, with growth of 506% in the last year. Overall, we'd say its growth is rather impressive. Of course, we've only taken a quick look at the stock's growth metrics, here. This graph of historic revenue growth shows how Tuas is building its business over time.

Can Tuas Raise More Cash Easily?

While Tuas seems to be in a decent position, we reckon it is still worth thinking about how easily it could raise more cash, if that proved desirable. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash and drive growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Tuas has a market capitalisation of S$682m and burnt through S$25m last year, which is 3.7% of the company's market value. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

Is Tuas' Cash Burn A Worry?

It may already be apparent to you that we're relatively comfortable with the way Tuas is burning through its cash. For example, we think its revenue growth suggests that the company is on a good path. But it's fair to say that its cash burn relative to its market cap was also very reassuring. After considering a range of factors in this article, we're pretty relaxed about its cash burn, since the company seems to be in a good position to continue to fund its growth. On another note, we conducted an in-depth investigation of the company, and identified 3 warning signs for Tuas (2 don't sit too well with us!) that you should be aware of before investing here.

Of course Tuas may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Tuas might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:TUA

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor