Advertisement

Tuas (ASX:TUA) Valuation in Focus After AUD 50 Million Equity Raise

Simply Wall St

Reviewed by Kshitija Bhandaru

Tuas (ASX:TUA) has just wrapped up a follow-on equity offering, bringing in around AUD 50 million by issuing over 9 million new ordinary shares at AUD 5.51 each. Investors are watching closely as this capital injection is likely to shape Tuas’s next steps and how the market perceives its growth strategy.

See our latest analysis for Tuas.

Tuas shares have cooled off in the last month with a 15.5% drop, but when you zoom out, the momentum is still impressive. The past year’s total return stands at nearly 30%, and there is a staggering 376% total return over three years. Investors seem to be recalibrating short-term expectations after the fundraising, even as the longer-term growth narrative remains strong.

If you’re on the lookout for other high-potential companies driven by significant insider belief and momentum, this could be the moment to broaden your search and discover fast growing stocks with high insider ownership

With the share price now sitting well below its analyst target and long-term returns still impressive, the real question is whether Tuas is undervalued, or if the market has already factored in all the growth ahead.

Price-to-Sales of 21x: Is it justified?

Tuas trades at a price-to-sales ratio of 21x, placing the stock far above both its industry peers and the broader market. With a last close price of A$6.90, investors are paying a steep premium for each dollar of Tuas’s sales compared to other telecom names.

The price-to-sales ratio measures what investors are willing to pay for each dollar of the company’s revenue. In the telecom sector, this ratio can highlight either premium growth expectations or an overheating valuation if it strays too far from the norm.

In Tuas’s case, the latest multiple is much higher than the global telecom sector average of 1.4x, the peer average of 2.1x, and the “fair” price-to-sales estimate of 3.6x that regression analysis suggests would be more reasonable. This signals the market may be pricing in very optimistic growth assumptions and any deviation from that script could trigger significant volatility.

Explore the SWS fair ratio for Tuas

Result: Price-to-Sales of 21x (OVERVALUED)

However, slower revenue growth or a sudden change in market sentiment could quickly challenge the lofty expectations that are currently priced into Tuas shares.

Find out about the key risks to this Tuas narrative.

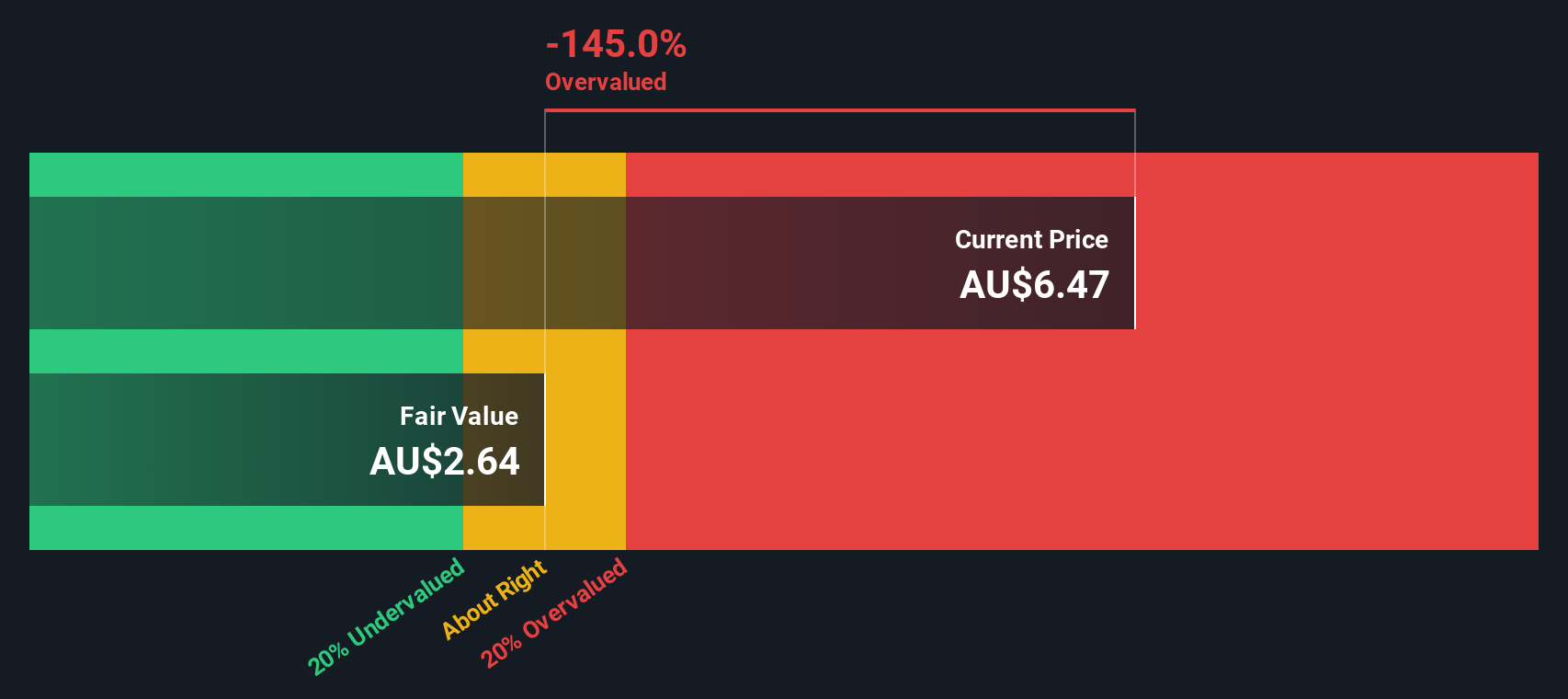

Another View: What Does Our DCF Model Say?

While the price-to-sales ratio shows Tuas as expensive compared to peers, the Simply Wall St DCF model also considers the stock overvalued, with a current share price significantly above our fair value estimate of A$2.64. This perspective raises questions about how much upside remains, or whether investors may be relying too heavily on growth projections.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Tuas for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Tuas Narrative

Whether you want to dig deeper, challenge these findings, or uncover your own perspective, you can craft your own narrative in just a few minutes: Do it your way

A great starting point for your Tuas research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

You don't have to settle for the usual picks. Let your next smart move start with our handpicked screens that spotlight standout opportunities you might have missed.

- Tap into tomorrow’s technology and see which companies are shaping artificial intelligence by checking out these 25 AI penny stocks.

- Strengthen your portfolio with potential bargain buys. Find market standouts that could be undervalued right now through these 894 undervalued stocks based on cash flows.

- Boost your passive income plan and access a range of top-yield opportunities over 3% by reviewing these 18 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Tuas might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:TUA

Flawless balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor