Advertisement

- Australia

- /

- Wireless Telecom

- /

- ASX:HTA

Shareholders in Hutchison Telecommunications (Australia) (ASX:HTA) have lost 87%, as stock drops 29% this past week

Some stocks are best avoided. We really hate to see fellow investors lose their hard-earned money. Anyone who held Hutchison Telecommunications (Australia) Limited (ASX:HTA) for five years would be nursing their metaphorical wounds since the share price dropped 87% in that time. And some of the more recent buyers are probably worried, too, with the stock falling 35% in the last year. On top of that, the share price is down 29% in the last week. We really feel for shareholders in this scenario. It's a good reminder of the importance of diversification, and it's worth keeping in mind there's more to life than money, anyway.

After losing 29% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

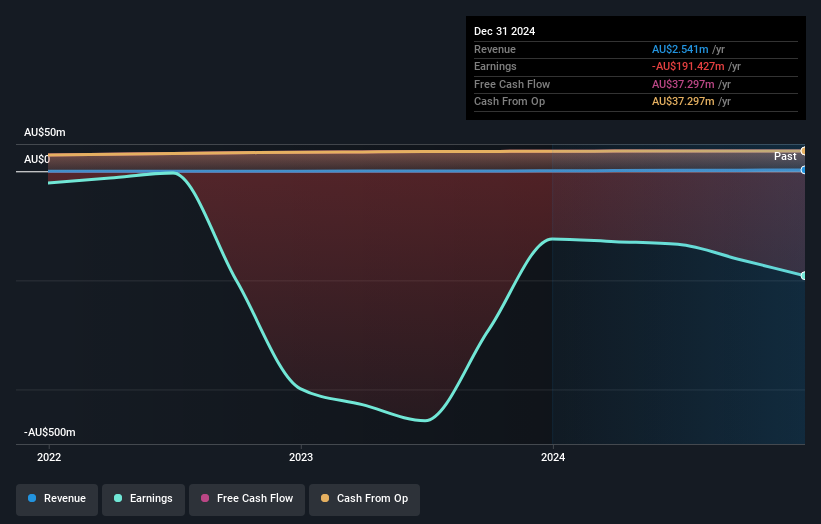

We've discovered 3 warning signs about Hutchison Telecommunications (Australia). View them for free.Because Hutchison Telecommunications (Australia) made a loss in the last twelve months, we think the market is probably more focussed on revenue and revenue growth, at least for now. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. That's because fast revenue growth can be easily extrapolated to forecast profits, often of considerable size.

In the last five years Hutchison Telecommunications (Australia) saw its revenue shrink by 30% per year. That's definitely a weaker result than most pre-profit companies report. So it's not altogether surprising to see the share price down 13% per year in the same time period. This kind of price performance makes us very wary, especially when combined with falling revenue. Of course, the poor performance could mean the market has been too severe selling down. That can happen.

You can see below how earnings and revenue have changed over time (discover the exact values by clicking on the image).

Balance sheet strength is crucial. It might be well worthwhile taking a look at our free report on how its financial position has changed over time.

A Different Perspective

While the broader market gained around 9.5% in the last year, Hutchison Telecommunications (Australia) shareholders lost 35%. However, keep in mind that even the best stocks will sometimes underperform the market over a twelve month period. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 13% per year over five years. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. It's always interesting to track share price performance over the longer term. But to understand Hutchison Telecommunications (Australia) better, we need to consider many other factors. Like risks, for instance. Every company has them, and we've spotted 3 warning signs for Hutchison Telecommunications (Australia) (of which 2 are significant!) you should know about.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

Valuation is complex, but we're here to simplify it.

Discover if Hutchison Telecommunications (Australia) might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:HTA

Hutchison Telecommunications (Australia)

Provides telecommunications services in Australia.

Flawless balance sheet low.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.2% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|20.5% undervalued

CH

Community Contributor