Advertisement

Here's Why We Think Flexiroam Limited's (ASX:FRX) CEO Compensation Looks Fair for the time being

Key Insights

- Flexiroam to hold its Annual General Meeting on 31st of October

- Total pay for CEO Marc Barnett includes AU$126.6k salary

- The total compensation is similar to the average for the industry

- Flexiroam's total shareholder return over the past three years was 50% while its EPS grew by 8.1% over the past three years

Under the guidance of CEO Marc Barnett, Flexiroam Limited (ASX:FRX) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 31st of October. Here is our take on why we think the CEO compensation looks appropriate.

View our latest analysis for Flexiroam

How Does Total Compensation For Marc Barnett Compare With Other Companies In The Industry?

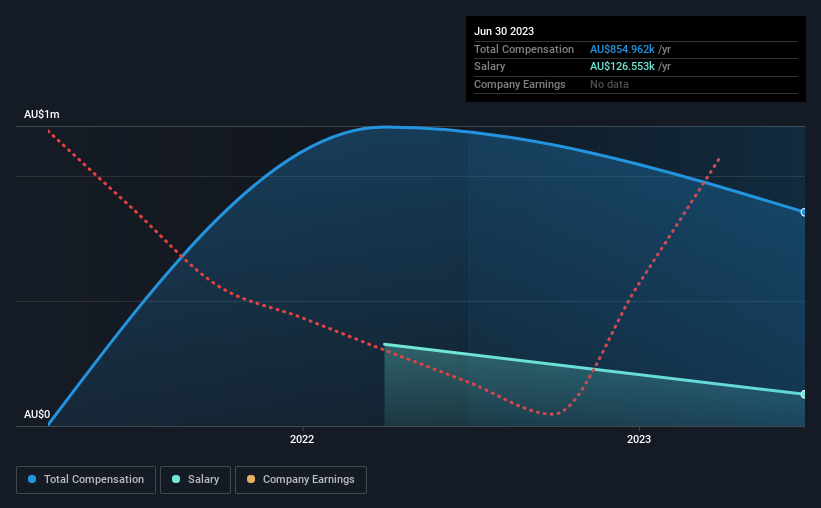

Our data indicates that Flexiroam Limited has a market capitalization of AU$22m, and total annual CEO compensation was reported as AU$855k for the year to June 2023. That's a notable decrease of 29% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at AU$127k.

In comparison with other companies in the Australian Telecom industry with market capitalizations under AU$315m, the reported median total CEO compensation was AU$676k. This suggests that Flexiroam remunerates its CEO largely in line with the industry average. Moreover, Marc Barnett also holds AU$1.3m worth of Flexiroam stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | AU$127k | AU$327k | 15% |

| Other | AU$728k | AU$868k | 85% |

| Total Compensation | AU$855k | AU$1.2m | 100% |

On an industry level, around 45% of total compensation represents salary and 55% is other remuneration. Flexiroam sets aside a smaller share of compensation for salary, in comparison to the overall industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at Flexiroam Limited's Growth Numbers

Over the past three years, Flexiroam Limited has seen its earnings per share (EPS) grow by 8.1% per year. Its revenue is up 143% over the last year.

It's great to see that revenue growth is strong. And in that context, the modest EPS improvement certainly isn't shabby. So while we'd stop short of saying growth is absolutely outstanding, there are definitely some clear positives! Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Flexiroam Limited Been A Good Investment?

Most shareholders would probably be pleased with Flexiroam Limited for providing a total return of 50% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. In saying that, any proposed increase to CEO compensation will still be assessed on how reasonable it is based on performance and industry benchmarks.

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. We identified 5 warning signs for Flexiroam (3 are concerning!) that you should be aware of before investing here.

Switching gears from Flexiroam, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:FRX

FlexiRoam

Engages in the telecommunications and Internet of Things (IoT) connectivity business worldwide.

Slight risk with imperfect balance sheet.

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$121.2% undervalued

13 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$245.0% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15081.9% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RedhawkCC on Prime Medicine ·

PRME remains a long shot but publication in the New England Journal of Medicine helps.

Fair Value:US$0.0469.1k% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3925.9% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative