Brokers Are Upgrading Their Views On Audinate Group Limited (ASX:AD8) With These New Forecasts

Celebrations may be in order for Audinate Group Limited (ASX:AD8) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. Consensus estimates suggest investors could expect greatly increased statutory revenues and earnings per share, with the analysts modelling a real improvement in business performance. The market may be pricing in some blue sky too, with the share price gaining 19% to AU$9.84 in the last 7 days. We'll be curious to see if these new estimates convince the market to lift the stock price higher still.

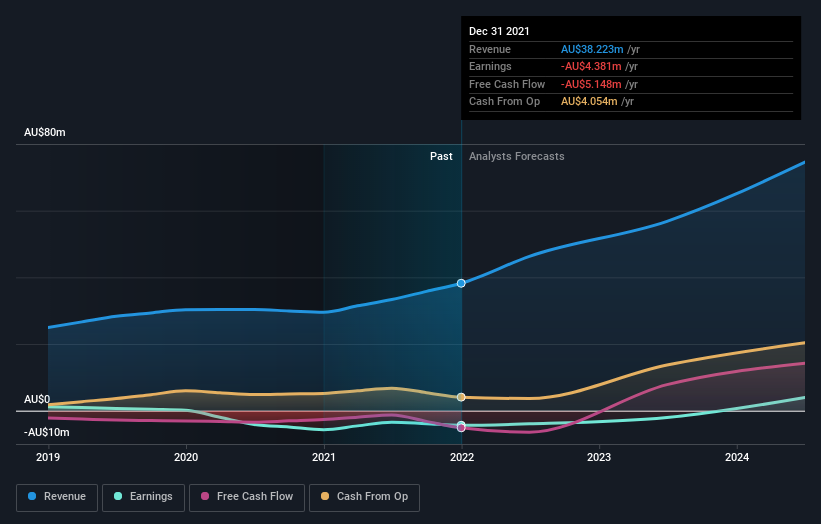

After the upgrade, the four analysts covering Audinate Group are now predicting revenues of AU$46m in 2022. If met, this would reflect a huge 21% improvement in sales compared to the last 12 months. The loss per share is expected to ameliorate slightly, reducing to AU$0.052. Yet before this consensus update, the analysts had been forecasting revenues of AU$41m and losses of AU$0.072 per share in 2022. We can see there's definitely been a change in sentiment in this update, with the analysts administering a sizeable upgrade to this year's revenue estimates, while at the same time reducing their loss estimates.

View our latest analysis for Audinate Group

The consensus price target rose 5.2% to AU$10.15, with the analysts encouraged by the higher revenue and lower forecast losses for this year. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Audinate Group at AU$11.75 per share, while the most bearish prices it at AU$9.00. Still, with such a tight range of estimates, it suggests the analysts have a pretty good idea of what they think the company is worth.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that Audinate Group's rate of growth is expected to accelerate meaningfully, with the forecast 47% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 19% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 22% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Audinate Group to grow faster than the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses this year, perhaps suggesting Audinate Group is moving incrementally towards profitability. Fortunately, analysts also upgraded their revenue estimates, and our data indicates sales are expected to perform better than the wider market. Given that the consensus looks almost universally bullish, with a substantial increase to forecasts and a higher price target, Audinate Group could be worth investigating further.

That's a pretty serious upgrade, but shareholders might be even more pleased to know that forecasts expect Audinate Group to be able to reach break-even within the next few years. You can learn more about these forecasts, for free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:AD8

Audinate Group

Engages in develops and sells digital audio visual (AV) networking solutions Australia and internationally.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion