- Australia

- /

- Retail Distributors

- /

- ASX:NTD

Is It Smart To Buy National Tyre & Wheel Limited (ASX:NTD) Before It Goes Ex-Dividend?

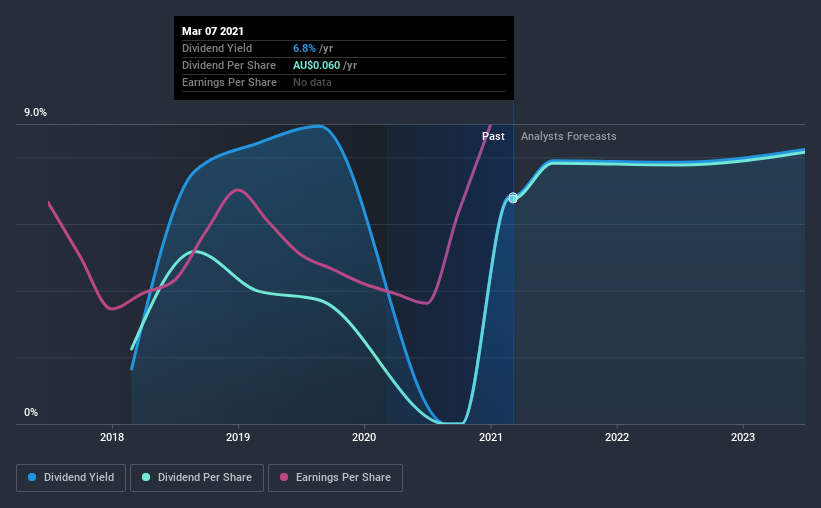

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that National Tyre & Wheel Limited (ASX:NTD) is about to go ex-dividend in just four days. If you purchase the stock on or after the 12th of March, you won't be eligible to receive this dividend, when it is paid on the 9th of April.

National Tyre & Wheel's next dividend payment will be AU$0.03 per share, on the back of last year when the company paid a total of AU$0.06 to shareholders. Based on the last year's worth of payments, National Tyre & Wheel stock has a trailing yield of around 6.8% on the current share price of A$0.88. If you buy this business for its dividend, you should have an idea of whether National Tyre & Wheel's dividend is reliable and sustainable. So we need to investigate whether National Tyre & Wheel can afford its dividend, and if the dividend could grow.

View our latest analysis for National Tyre & Wheel

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. National Tyre & Wheel paid out a comfortable 27% of its profit last year. Yet cash flows are even more important than profits for assessing a dividend, so we need to see if the company generated enough cash to pay its distribution. It paid out 6.6% of its free cash flow as dividends last year, which is conservatively low.

It's encouraging to see that the dividend is covered by both profit and cash flow. This generally suggests the dividend is sustainable, as long as earnings don't drop precipitously.

Click here to see how much of its profit National Tyre & Wheel paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. For this reason, we're glad to see National Tyre & Wheel's earnings per share have risen 10% per annum over the last five years. The company has managed to grow earnings at a rapid rate, while reinvesting most of the profits within the business. This will make it easier to fund future growth efforts and we think this is an attractive combination - plus the dividend can always be increased later.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the past three years, National Tyre & Wheel has increased its dividend at approximately 44% a year on average. It's great to see earnings per share growing rapidly over several years, and dividends per share growing right along with it.

Final Takeaway

Should investors buy National Tyre & Wheel for the upcoming dividend? National Tyre & Wheel has grown its earnings per share while simultaneously reinvesting in the business. Unfortunately it's cut the dividend at least once in the past three years, but the conservative payout ratio makes the current dividend look sustainable. It's a promising combination that should mark this company worthy of closer attention.

In light of that, while National Tyre & Wheel has an appealing dividend, it's worth knowing the risks involved with this stock. For example, we've found 4 warning signs for National Tyre & Wheel that we recommend you consider before investing in the business.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade National Tyre & Wheel, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade NTAW Holdings, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NTAW Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:NTD

NTAW Holdings

NTAW Holdings Limited, together with its subsidiaries, markets and distributes motor vehicle tires, wheels, tubes, and related products in Australia, New Zealand, and South Africa.

Moderate and good value.