Advertisement

- Australia

- /

- Specialty Stores

- /

- ASX:NCK

3 ASX Stocks Estimated To Be Trading At Discounts Of Up To 48.7%

Simply Wall St

Reviewed by Simply Wall St

After a challenging period in Week 11, the Australian market is poised for a rebound, fueled by Wall Street's significant rally and China's new stimulus measures aimed at boosting consumption. In this environment, identifying undervalued stocks can be particularly rewarding as investors seek opportunities that may benefit from improving market conditions and economic stimuli.

Top 10 Undervalued Stocks Based On Cash Flows In Australia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Acrow (ASX:ACF) | A$1.03 | A$2.00 | 48.5% |

| Domino's Pizza Enterprises (ASX:DMP) | A$26.81 | A$52.27 | 48.7% |

| Nido Education (ASX:NDO) | A$0.88 | A$1.62 | 45.8% |

| Capricorn Metals (ASX:CMM) | A$8.22 | A$15.00 | 45.2% |

| Charter Hall Group (ASX:CHC) | A$16.34 | A$31.91 | 48.8% |

| SciDev (ASX:SDV) | A$0.445 | A$0.82 | 45.4% |

| Polymetals Resources (ASX:POL) | A$0.84 | A$1.68 | 49.9% |

| ReadyTech Holdings (ASX:RDY) | A$2.68 | A$5.13 | 47.8% |

| Superloop (ASX:SLC) | A$2.09 | A$3.74 | 44.1% |

| Adriatic Metals (ASX:ADT) | A$4.46 | A$8.11 | 45% |

Let's take a closer look at a couple of our picks from the screened companies.

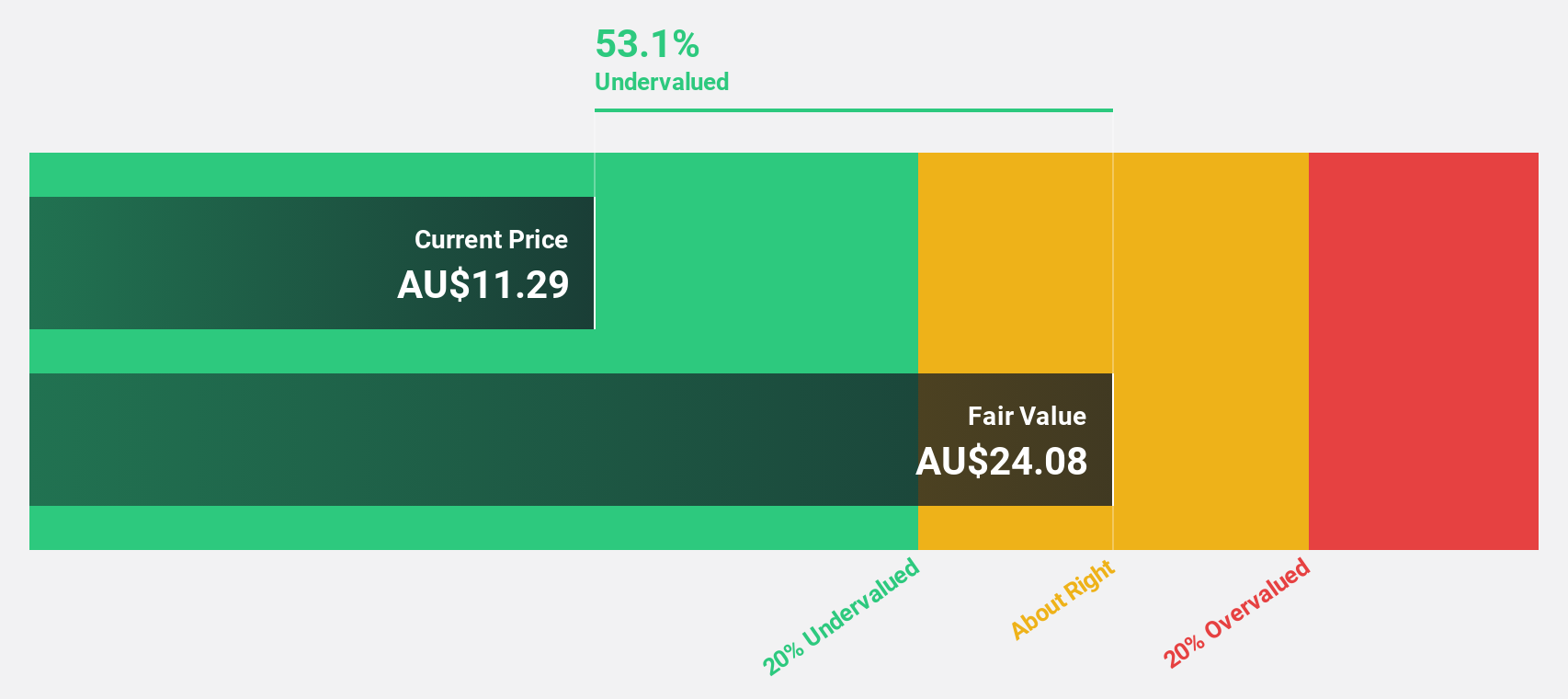

Domino's Pizza Enterprises (ASX:DMP)

Overview: Domino's Pizza Enterprises Limited operates retail food outlets and has a market cap of A$2.48 billion.

Operations: The company generates revenue primarily through its restaurant operations, amounting to A$2.30 billion.

Estimated Discount To Fair Value: 48.7%

Domino's Pizza Enterprises is trading at A$26.81, significantly below its estimated fair value of A$52.27, suggesting potential undervaluation based on cash flows. Despite recent challenges with a net loss of A$22.17 million for the half-year ended December 2024 and high debt levels, earnings are forecast to grow significantly at 43.3% annually over the next three years, outpacing the broader Australian market growth rate of 12.2%.

- Insights from our recent growth report point to a promising forecast for Domino's Pizza Enterprises' business outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Domino's Pizza Enterprises.

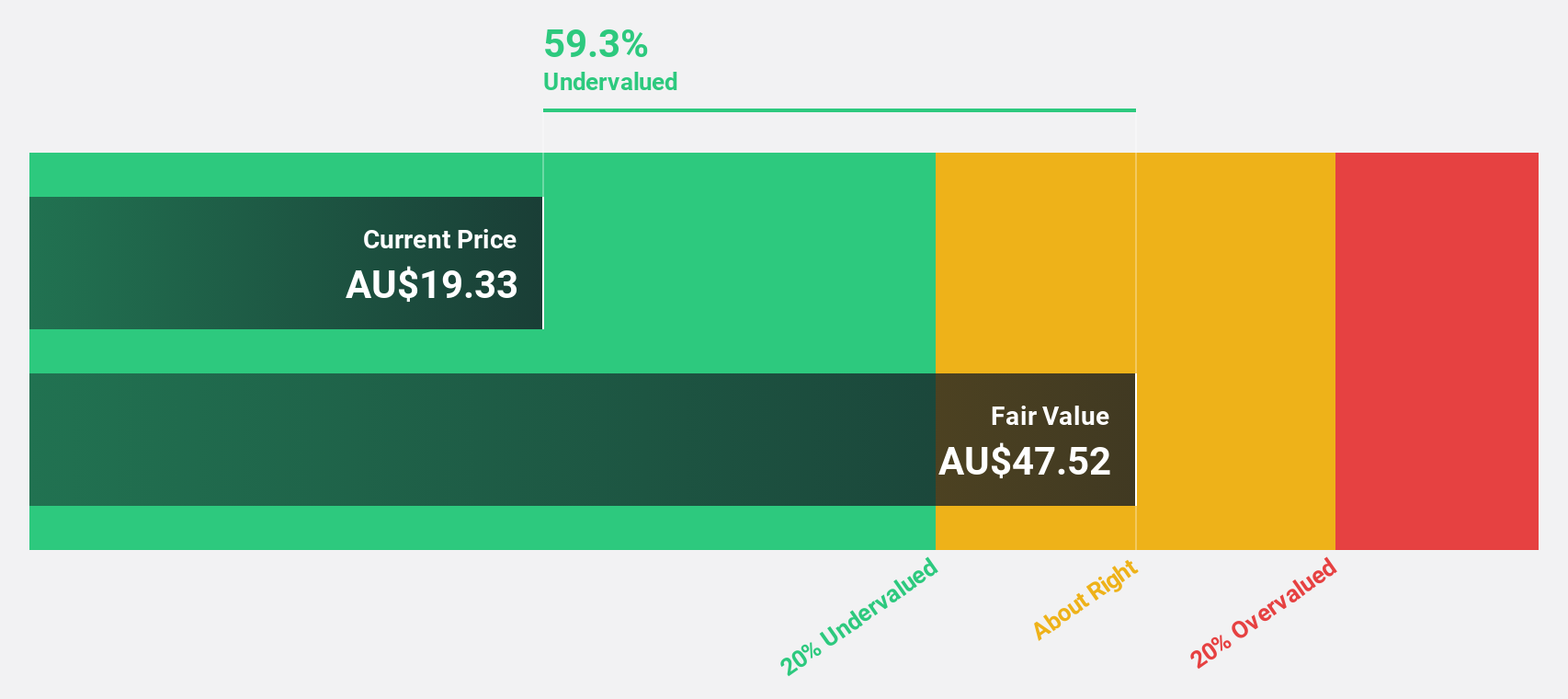

Nick Scali (ASX:NCK)

Overview: Nick Scali Limited, with a market cap of A$1.34 billion, is involved in sourcing and retailing household furniture and related accessories across Australia, the United Kingdom, and New Zealand.

Operations: The company's revenue comes primarily from the retailing of furniture, amounting to A$492.63 million.

Estimated Discount To Fair Value: 43.5%

Nick Scali is trading at A$15.69, significantly below its estimated fair value of A$27.77, highlighting potential undervaluation based on cash flows. Earnings are forecast to grow 12.3% annually, outpacing the Australian market's growth rate of 12.2%. Recent earnings show sales increased to A$251.07 million from A$226.63 million year-over-year, though net income decreased to A$30.04 million from A$43.01 million, and dividends were reduced from last year’s payout.

- Our earnings growth report unveils the potential for significant increases in Nick Scali's future results.

- Navigate through the intricacies of Nick Scali with our comprehensive financial health report here.

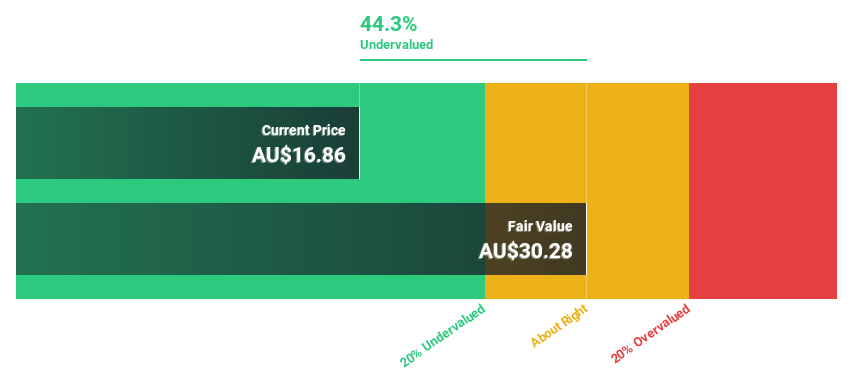

Sandfire Resources (ASX:SFR)

Overview: Sandfire Resources Limited is a mining company focused on the exploration, evaluation, and development of mineral tenements and projects, with a market capitalization of A$5.07 billion.

Operations: Sandfire Resources Limited generates revenue primarily from its MATSA Copper Operations ($604.43 million), Motheo Copper Project ($482.04 million), and Degrussa Copper Operations ($2.89 million).

Estimated Discount To Fair Value: 41.6%

Sandfire Resources, trading at A$11.06, is notably undervalued with an estimated fair value of A$18.95. The company's earnings are forecast to grow significantly at 32% annually, surpassing the Australian market's growth rate of 12.2%. Recent results for the half-year ended December 31, 2024, show sales increased to US$572.26 million from US$417.94 million year-over-year and net income reached US$51.5 million from a previous net loss of US$53.14 million.

- Upon reviewing our latest growth report, Sandfire Resources' projected financial performance appears quite optimistic.

- Dive into the specifics of Sandfire Resources here with our thorough financial health report.

Turning Ideas Into Actions

- Unlock more gems! Our Undervalued ASX Stocks Based On Cash Flows screener has unearthed 40 more companies for you to explore.Click here to unveil our expertly curated list of 43 Undervalued ASX Stocks Based On Cash Flows.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nick Scali might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:NCK

Nick Scali

Engages in sourcing and retailing of household furniture and related accessories in Australia, the United Kingdom, and New Zealand.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor