Advertisement

- Australia

- /

- Office REITs

- /

- ASX:CMW

3 Undervalued ASX Small Caps With Insider Buying In Australia

Simply Wall St

Reviewed by Simply Wall St

As the Australian market continues to navigate the complexities of global trade dynamics, with the ASX200 climbing 0.36% amid a favorable tariff outcome, small-cap stocks are garnering attention for their potential resilience and growth opportunities. In this environment, identifying promising small-cap companies often involves looking at factors such as insider buying trends and valuation metrics that suggest these stocks may be currently undervalued.

Top 10 Undervalued Small Caps With Insider Buying In Australia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Rural Funds Group | 7.7x | 5.7x | 38.28% | ★★★★★★ |

| Infomedia | 40.9x | 3.7x | 37.43% | ★★★★★☆ |

| Collins Foods | 16.8x | 0.6x | 13.48% | ★★★★★☆ |

| SHAPE Australia | 15.1x | 0.3x | 26.49% | ★★★★☆☆ |

| Dicker Data | 19.4x | 0.7x | -62.98% | ★★★★☆☆ |

| Centuria Capital Group | 20.7x | 4.6x | 48.80% | ★★★★☆☆ |

| Abacus Group | NA | 5.3x | 29.25% | ★★★★☆☆ |

| Cromwell Property Group | NA | 4.8x | 25.38% | ★★★★☆☆ |

| Healius | NA | 0.6x | 7.19% | ★★★★☆☆ |

| Eureka Group Holdings | 19.3x | 6.2x | 27.57% | ★★★☆☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

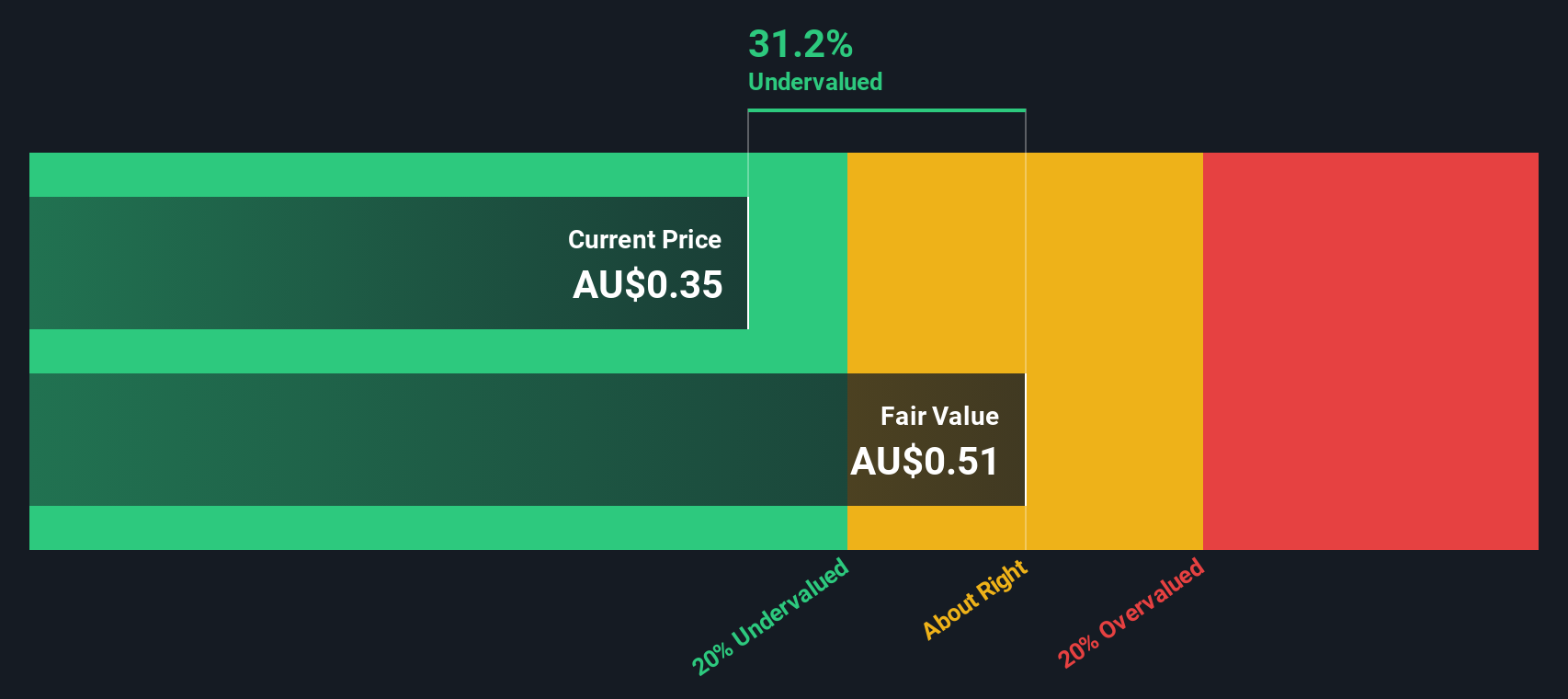

Abacus Storage King (ASX:ASK)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Abacus Storage King operates in the self-storage industry, focusing on rental and merchandising services, with a market cap of A$1.34 billion.

Operations: ASK generates revenue primarily from rental and merchandising, with a gross profit margin reaching 80.50% in recent periods. The company has experienced fluctuations in net income margin, peaking at 62.67% before stabilizing around lower levels. Operating expenses have shown an upward trend, impacting net income despite consistent revenue growth over time.

PE: 10.9x

Abacus Storage King, a player in the self-storage sector, presents an intriguing opportunity among Australia's undervalued stocks. Despite facing challenges like debt not being well-covered by operating cash flow and earnings forecasted to decline by 2.5% annually over the next three years, revenue is expected to grow at 7.3% per year. Insider confidence is evident with recent share purchases in December 2024, suggesting belief in potential future growth despite current financial hurdles.

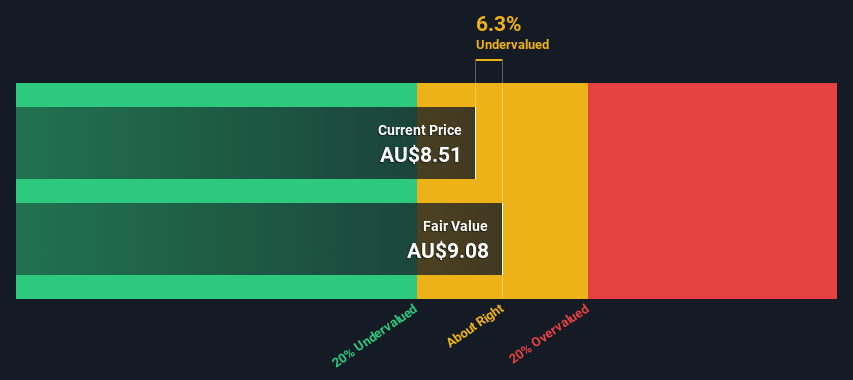

Collins Foods (ASX:CKF)

Simply Wall St Value Rating: ★★★★★☆

Overview: Collins Foods operates a network of fast-food restaurants, primarily under the KFC and Taco Bell brands in Australia and Europe, with a market capitalization of A$1.51 billion.

Operations: The company generates revenue primarily from KFC Restaurants in Australia and Europe, along with Taco Bell operations in Australia. Over recent periods, the gross profit margin has shown a slight decline from 52.88% to 50.42%. Operating expenses are significant, with sales and marketing being a notable component.

PE: 16.8x

Collins Foods, an Australian company expanding its restaurant footprint with plans for seven new locations in 2025, presents a compelling case among smaller companies. Despite a dip in net income to A$24.12 million for the half-year ending October 2024 from A$50.45 million previously, earnings are projected to grow annually by 18%. Insider confidence is evident as they have increased their shareholdings recently. While reliant on external borrowing, Collins Foods' strategic growth initiatives could enhance future prospects.

- Unlock comprehensive insights into our analysis of Collins Foods stock in this valuation report.

Gain insights into Collins Foods' past trends and performance with our Past report.

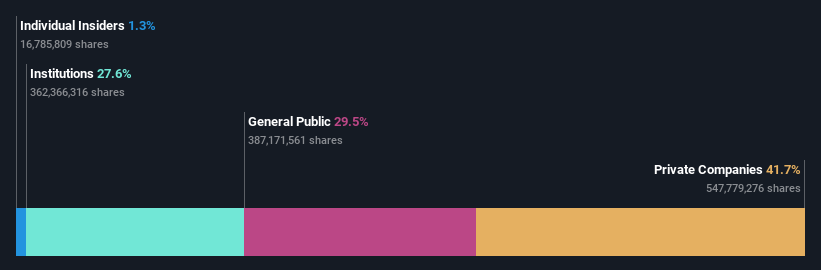

Cromwell Property Group (ASX:CMW)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Cromwell Property Group is a real estate investment and funds management company with operations focused on property investment, co-investments, and asset management, boasting a market capitalization of approximately A$2.26 billion.

Operations: The company generates revenue primarily from its Co-Investments, Investment Portfolio, and Funds and Asset Management segments. The net income margin has shown significant fluctuations, with recent periods reflecting negative margins reaching as low as -1.71%. Operating expenses have varied over time but have remained a notable component of the cost structure.

PE: -3.7x

Cromwell Property Group, a smaller player in the Australian market, has seen insider confidence with recent share purchases. Despite challenges like declining earnings over the past five years and reliance on external borrowing for funding, Cromwell remains attractive due to its potential for growth. A cash dividend of A$0.0075 is set for December 30, 2024. While financial stability is under scrutiny, insiders' actions suggest optimism about future prospects in the property sector.

Seize The Opportunity

- Reveal the 22 hidden gems among our Undervalued ASX Small Caps With Insider Buying screener with a single click here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:CMW

Cromwell Property Group

Cromwell Property Group (ASX:CMW) is a real estate investor and fund manager with operations on three continents and a global investor base.

Average dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.9% undervalued

TO

Community Contributor