As the Australian market experiences a mixed performance with the ASX200 closing slightly down and sectors like Information Technology showing strong gains, investors are keenly awaiting the upcoming Quarterly CPI data to gauge future economic conditions. In this environment, identifying promising small-cap stocks requires a focus on companies that demonstrate resilience and potential for growth amid sector-specific shifts and broader market sentiment.

Top 10 Undiscovered Gems With Strong Fundamentals In Australia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Schaffer | 24.98% | 2.97% | -6.23% | ★★★★★★ |

| Fiducian Group | NA | 9.94% | 6.48% | ★★★★★★ |

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Lycopodium | NA | 17.22% | 33.85% | ★★★★★★ |

| Red Hill Minerals | NA | 75.05% | 36.74% | ★★★★★★ |

| Steamships Trading | 33.60% | 4.17% | 3.90% | ★★★★★☆ |

| AMCIL | NA | 5.16% | 5.31% | ★★★★★☆ |

| Hearts and Minds Investments | 1.00% | 18.81% | 20.95% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Boart Longyear Group | 71.20% | 9.71% | 39.19% | ★★★★☆☆ |

We'll examine a selection from our screener results.

K&S (ASX:KSC)

Simply Wall St Value Rating: ★★★★☆☆

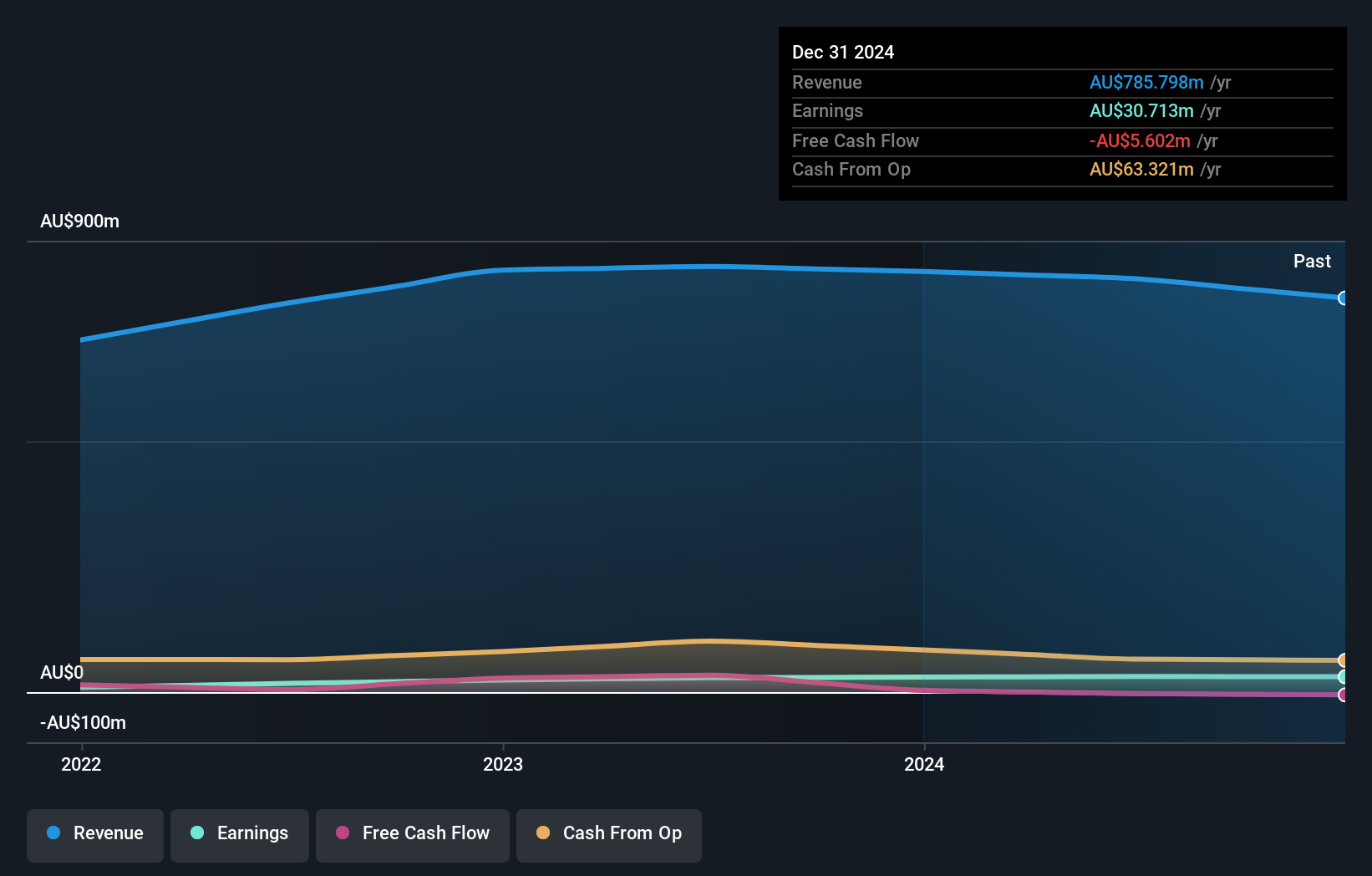

Overview: K&S Corporation Limited operates in transportation and logistics, warehousing, and fuel distribution across Australia and New Zealand, with a market cap of A$472.13 million.

Operations: K&S generates revenue primarily from its Australian Transport segment, contributing A$582.80 million, followed by Fuel at A$230.79 million and New Zealand Transport at A$72.93 million.

K&S, a notable player in the logistics sector, has shown resilience with earnings growth of 9.1% over the past year, outpacing the industry's -7% performance. The company's net income climbed to A$31.23 million from A$28.63 million previously, reflecting its high-quality earnings and robust operations. Despite an increase in debt to equity ratio from 12.5% to 16.1% over five years, interest payments remain well covered by EBIT at 10.2 times coverage, indicating sound financial management. Trading at 17.2% below estimated fair value suggests potential for investors seeking undervalued opportunities in this dynamic industry space.

- Click here to discover the nuances of K&S with our detailed analytical health report.

Review our historical performance report to gain insights into K&S''s past performance.

Mount Gibson Iron (ASX:MGX)

Simply Wall St Value Rating: ★★★★★★

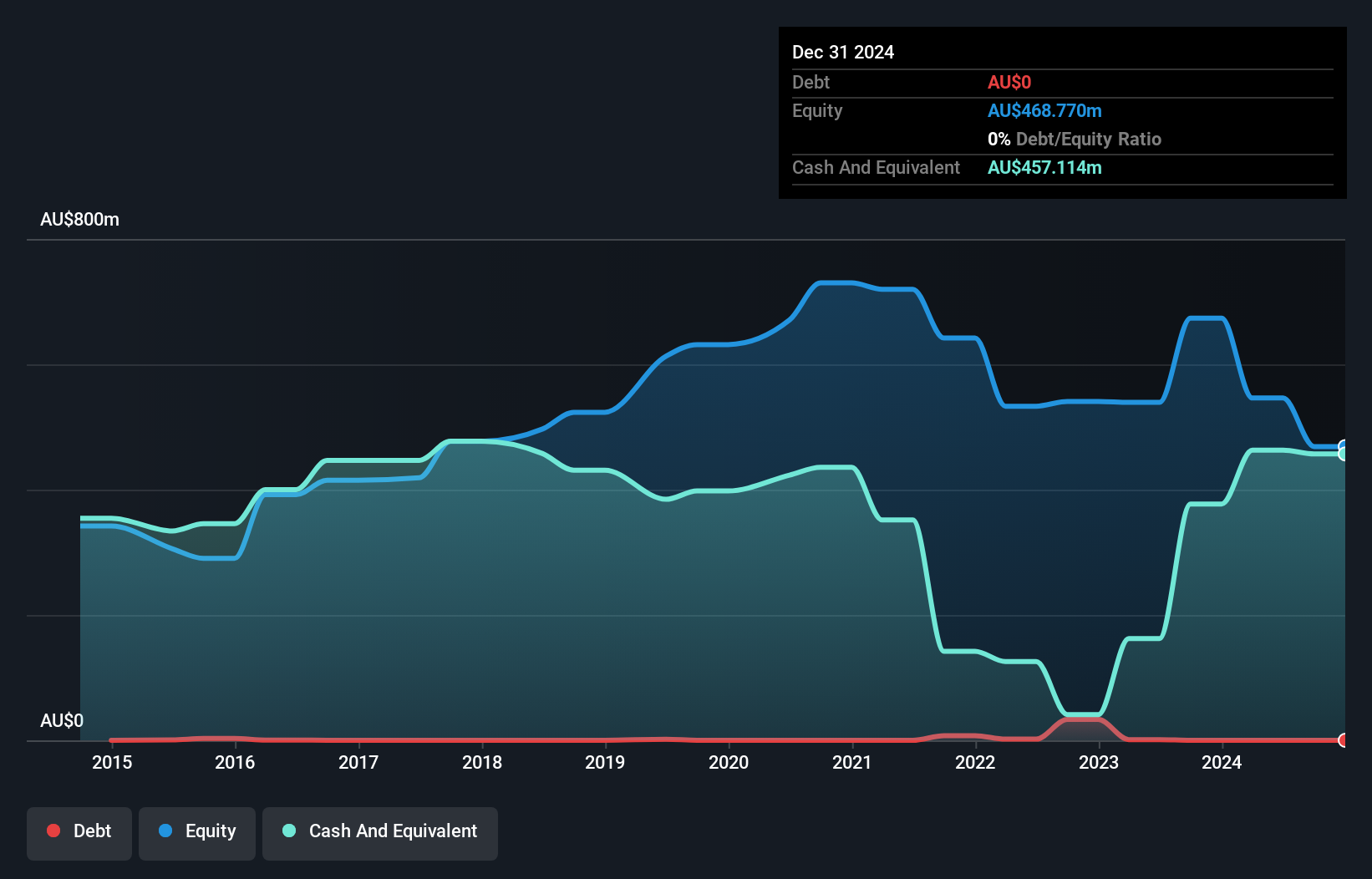

Overview: Mount Gibson Iron Limited is involved in the mining, processing, and export of hematite iron ore primarily to Australia and China, with a market capitalization of approximately A$382.44 million.

Operations: Mount Gibson Iron's primary revenue stream is from its Koolan Island segment, generating A$667.68 million.

Mount Gibson Iron, a notable player in the Australian mining sector, showcases strong financial health with no debt and earnings growth of 24% over the past year, outpacing industry averages. The company is trading at nearly 99% below its estimated fair value, suggesting potential undervaluation. Recent announcements include a share repurchase program targeting up to 60.92 million shares and production guidance aiming for iron ore sales between 2.7 to 3 million wmt in 2025 at operating costs of A$95-A$100 per wmt. With high-quality earnings and positive free cash flow, MGX stands well-positioned amidst industry challenges.

- Click here and access our complete health analysis report to understand the dynamics of Mount Gibson Iron.

Examine Mount Gibson Iron's past performance report to understand how it has performed in the past.

Servcorp (ASX:SRV)

Simply Wall St Value Rating: ★★★★☆☆

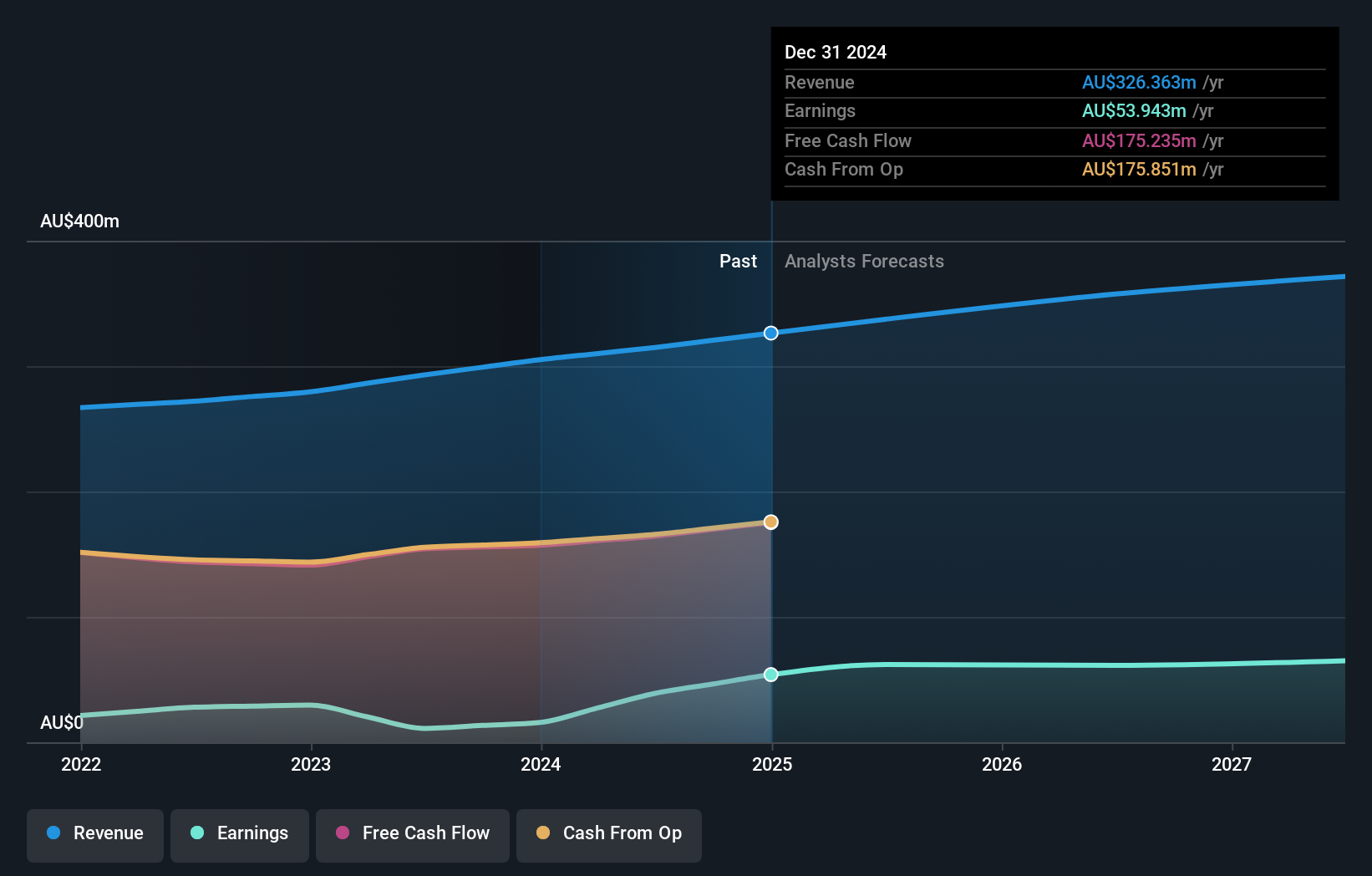

Overview: Servcorp Limited offers executive serviced and virtual offices, coworking spaces, and IT, communications, and secretarial services with a market capitalization of A$503.19 million.

Operations: Revenue for Servcorp Limited primarily comes from real estate rental, amounting to A$314.89 million.

Servcorp, a promising player in the Australian market, has shown remarkable growth with earnings surging by 253% in the past year, outpacing its real estate industry peers. The company is debt-free and boasts high-quality earnings, making it an attractive proposition. Trading at a significant discount of 83% to its estimated fair value, Servcorp seems undervalued compared to competitors. Recent financials reveal net income jumped to A$39 million from A$11 million last year, while revenue increased to A$317 million. The declared dividend for fiscal year 2024 rose by 14%, reflecting robust financial health and shareholder returns.

- Take a closer look at Servcorp's potential here in our health report.

Gain insights into Servcorp's historical performance by reviewing our past performance report.

Summing It All Up

- Reveal the 52 hidden gems among our ASX Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if K&S might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:KSC

K&S

Engages in the transportation and logistics, warehousing and fuel distribution businesses in Australia and New Zealand.

Proven track record with adequate balance sheet.