We Think Shareholders Are Less Likely To Approve A Pay Rise For Recce Pharmaceuticals Ltd's (ASX:RCE) CEO For Now

Key Insights

- Recce Pharmaceuticals' Annual General Meeting to take place on 7th of November

- Total pay for CEO James Graham includes AU$550.8k salary

- Total compensation is similar to the industry average

- Recce Pharmaceuticals' EPS declined by 2.8% over the past three years while total shareholder loss over the past three years was 54%

In the past three years, the share price of Recce Pharmaceuticals Ltd (ASX:RCE) has struggled to grow and now shareholders are sitting on a loss. Per share earnings growth is also lacking, despite revenue growth. In light of this performance, shareholders will have a chance to question the board in the upcoming AGM on 7th of November, where they can impact on future company performance by voting on resolutions, including executive compensation. We think shareholders may be cautious of approving a pay rise for the CEO at the moment, based on our analysis below.

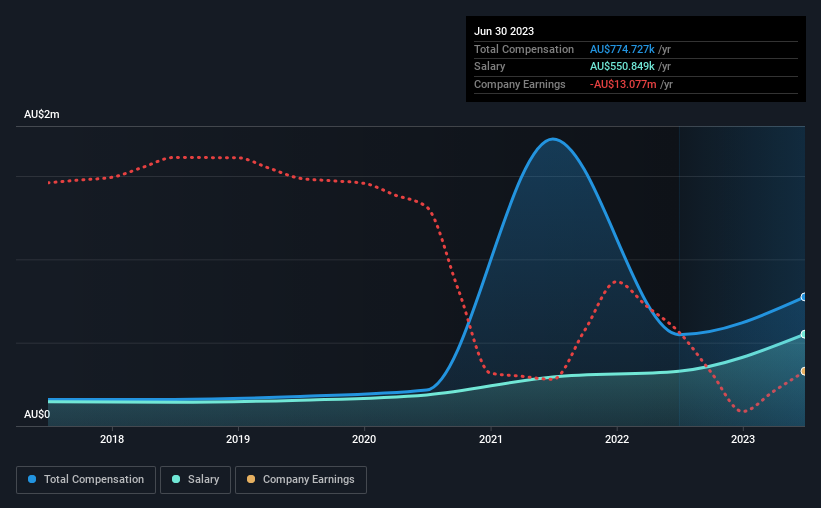

See our latest analysis for Recce Pharmaceuticals

How Does Total Compensation For James Graham Compare With Other Companies In The Industry?

At the time of writing, our data shows that Recce Pharmaceuticals Ltd has a market capitalization of AU$89m, and reported total annual CEO compensation of AU$775k for the year to June 2023. We note that's an increase of 41% above last year. In particular, the salary of AU$550.8k, makes up a huge portion of the total compensation being paid to the CEO.

In comparison with other companies in the Australian Pharmaceuticals industry with market capitalizations under AU$315m, the reported median total CEO compensation was AU$688k. So it looks like Recce Pharmaceuticals compensates James Graham in line with the median for the industry. Moreover, James Graham also holds AU$2.9m worth of Recce Pharmaceuticals stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | AU$551k | AU$328k | 71% |

| Other | AU$224k | AU$220k | 29% |

| Total Compensation | AU$775k | AU$548k | 100% |

On an industry level, roughly 61% of total compensation represents salary and 39% is other remuneration. Recce Pharmaceuticals pays out 71% of remuneration in the form of a salary, significantly higher than the industry average. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Recce Pharmaceuticals Ltd's Growth Numbers

Recce Pharmaceuticals Ltd has reduced its earnings per share by 2.8% a year over the last three years. It achieved revenue growth of 42% over the last year.

The decrease in EPS could be a concern for some investors. But in contrast the revenue growth is strong, suggesting future potential for EPS growth. It's hard to reach a conclusion about business performance right now. This may be one to watch. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Recce Pharmaceuticals Ltd Been A Good Investment?

With a total shareholder return of -54% over three years, Recce Pharmaceuticals Ltd shareholders would by and large be disappointed. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

The loss to shareholders over the past three years is certainly concerning and possibly has something to do with the fact that the company's earnings haven't grown. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We did our research and identified 7 warning signs (and 3 which are a bit unpleasant) in Recce Pharmaceuticals we think you should know about.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:RCE

Recce Pharmaceuticals

Recce Pharmaceuticals Ltd, discovers, develops, and commercializes synthetic anti–infectives in Australia, the United Kingdom, and the United States.

Moderate and slightly overvalued.

Market Insights

Community Narratives