- Australia

- /

- Life Sciences

- /

- ASX:PIQ

Shareholders have faith in loss-making Proteomics International Laboratories (ASX:PIQ) as stock climbs 14% in past week, taking five-year gain to 224%

It hasn't been the best quarter for Proteomics International Laboratories Limited (ASX:PIQ) shareholders, since the share price has fallen 11% in that time. But that scarcely detracts from the really solid long term returns generated by the company over five years. We think most investors would be happy with the 224% return, over that period. So while it's never fun to see a share price fall, it's important to look at a longer time horizon. The more important question is whether the stock is too cheap or too expensive today.

Since the stock has added AU$12m to its market cap in the past week alone, let's see if underlying performance has been driving long-term returns.

View our latest analysis for Proteomics International Laboratories

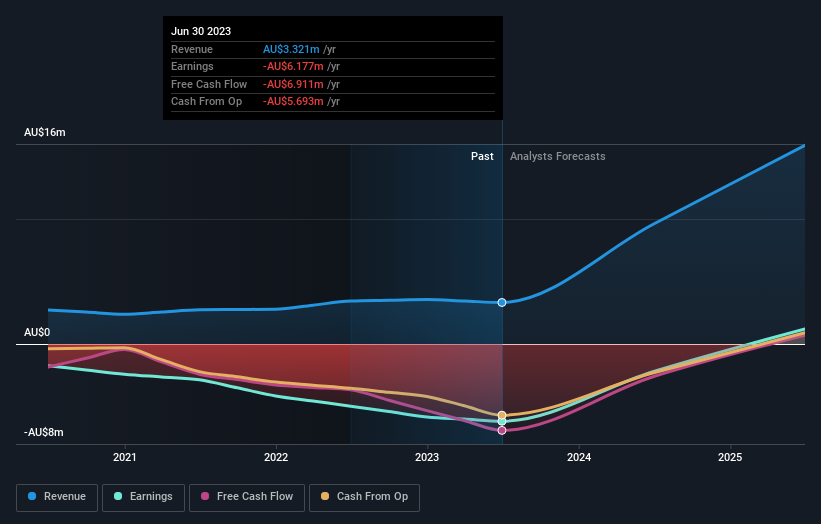

Proteomics International Laboratories isn't currently profitable, so most analysts would look to revenue growth to get an idea of how fast the underlying business is growing. When a company doesn't make profits, we'd generally expect to see good revenue growth. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

In the last 5 years Proteomics International Laboratories saw its revenue grow at 7.9% per year. That's a pretty good long term growth rate. We'd argue this growth has been reflected in the share price which has climbed at a rate of 26% per year over in that time. Given that the business has made good progress on the top line, it would be worth taking a look at the growth trend. Accelerating growth can be a sign of an inflection point - and could indicate profits lie ahead. Worth watching 100%

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

We consider it positive that insiders have made significant purchases in the last year. Having said that, most people consider earnings and revenue growth trends to be a more meaningful guide to the business. If you are thinking of buying or selling Proteomics International Laboratories stock, you should check out this free report showing analyst profit forecasts.

A Different Perspective

Proteomics International Laboratories shareholders are down 10% for the year, but the market itself is up 4.6%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Longer term investors wouldn't be so upset, since they would have made 26%, each year, over five years. It could be that the recent sell-off is an opportunity, so it may be worth checking the fundamental data for signs of a long term growth trend. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider risks, for instance. Every company has them, and we've spotted 4 warning signs for Proteomics International Laboratories you should know about.

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Australian exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:PIQ

Proteomics International Laboratories

Operates as a medical technology company with a focus on the area of proteomics in Australia, New Zealand, the United States, Europe, India, and South East Asia.

Flawless balance sheet low.

Market Insights

Community Narratives