This Is Why Opthea Limited's (ASX:OPT) CEO Compensation Looks Appropriate

Shareholders may be wondering what CEO Megan Baldwin plans to do to improve the less than great performance at Opthea Limited (ASX:OPT) recently. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 18 October 2021. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. In our opinion, CEO compensation does not look excessive and we discuss why.

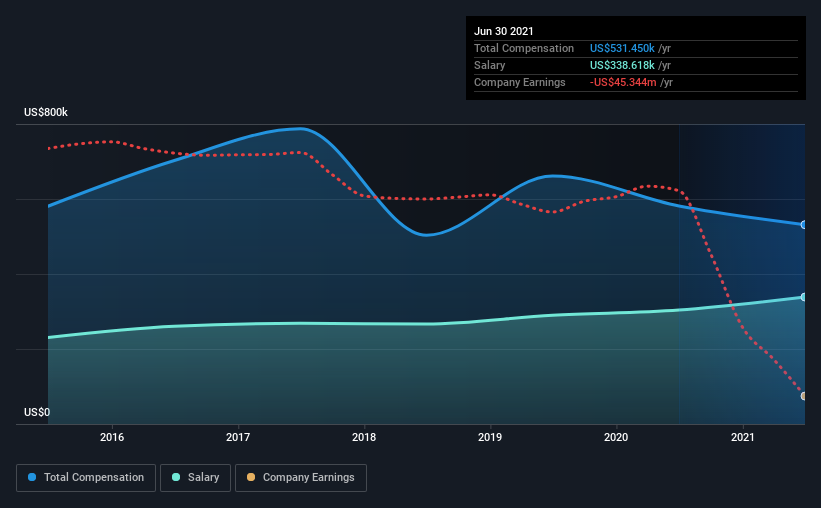

See our latest analysis for Opthea

Comparing Opthea Limited's CEO Compensation With the industry

Our data indicates that Opthea Limited has a market capitalization of AU$446m, and total annual CEO compensation was reported as US$531k for the year to June 2021. Notably, that's a decrease of 8.6% over the year before. We note that the salary portion, which stands at US$338.6k constitutes the majority of total compensation received by the CEO.

On comparing similar companies from the same industry with market caps ranging from AU$272m to AU$1.1b, we found that the median CEO total compensation was US$797k. In other words, Opthea pays its CEO lower than the industry median. What's more, Megan Baldwin holds AU$4.9m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | US$339k | US$304k | 64% |

| Other | US$193k | US$278k | 36% |

| Total Compensation | US$531k | US$581k | 100% |

On an industry level, roughly 57% of total compensation represents salary and 43% is other remuneration. Opthea is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Opthea Limited's Growth Numbers

Over the last three years, Opthea Limited has shrunk its earnings per share by 32% per year. In the last year, its revenue is down 5.1%.

Few shareholders would be pleased to read that EPS have declined. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Opthea Limited Been A Good Investment?

We think that the total shareholder return of 108%, over three years, would leave most Opthea Limited shareholders smiling. This strong performance might mean some shareholders don't mind if the CEO were to be paid more than is normal for a company of its size.

To Conclude...

Despite the strong returns on shareholders' investments, the fact that earnings have failed to grow makes us skeptical about the stock keeping up its current momentum. These are are some concerns that shareholders may want to address the board when they revisit their investment thesis.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We did our research and identified 3 warning signs (and 1 which is potentially serious) in Opthea we think you should know about.

Switching gears from Opthea, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you're looking to trade Opthea, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:OPT

Opthea

A clinical-stage biopharmaceutical company, develops and commercializes drugs for eye diseases in Australia and the United States.

Moderate and slightly overvalued.

Market Insights

Community Narratives