Advertisement

It's Probably Less Likely That Orthocell Limited's (ASX:OCC) CEO Will See A Huge Pay Rise This Year

Key Insights

- Orthocell will host its Annual General Meeting on 31st of October

- CEO Paul Anderson's total compensation includes salary of AU$420.0k

- The total compensation is similar to the average for the industry

- Over the past three years, Orthocell's EPS grew by 3.2% and over the past three years, the total loss to shareholders 8.5%

As many shareholders of Orthocell Limited (ASX:OCC) will be aware, they have not made a gain on their investment in the past three years. However, what is unusual is that EPS growth has been positive, suggesting that the share price has diverged from fundamentals. Shareholders may want to question the board on the future direction of the company at the upcoming AGM on 31st of October. They could also influence management through voting on resolutions such as executive remuneration. We discuss below why we think shareholders should be cautious of approving a raise for the CEO at the moment.

View our latest analysis for Orthocell

How Does Total Compensation For Paul Anderson Compare With Other Companies In The Industry?

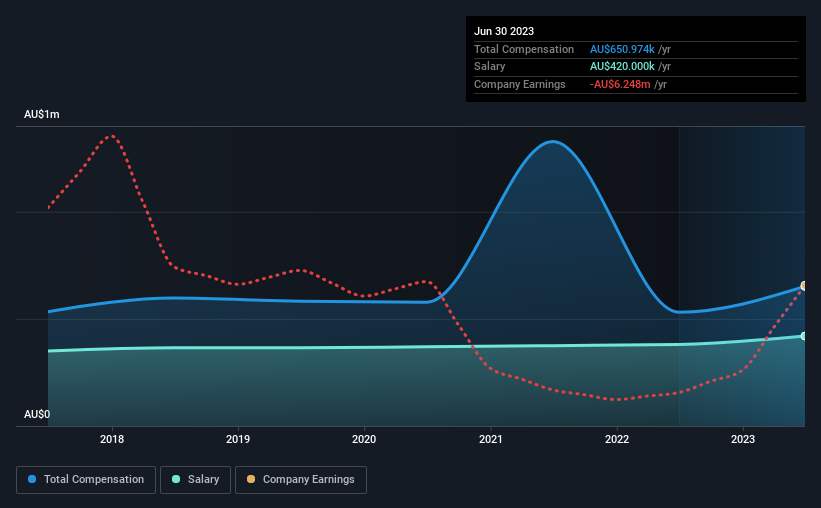

At the time of writing, our data shows that Orthocell Limited has a market capitalization of AU$64m, and reported total annual CEO compensation of AU$651k for the year to June 2023. That's a notable increase of 23% on last year. Notably, the salary which is AU$420.0k, represents most of the total compensation being paid.

For comparison, other companies in the Australian Biotechs industry with market capitalizations below AU$316m, reported a median total CEO compensation of AU$603k. This suggests that Orthocell remunerates its CEO largely in line with the industry average. What's more, Paul Anderson holds AU$1.1m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | AU$420k | AU$380k | 65% |

| Other | AU$231k | AU$151k | 35% |

| Total Compensation | AU$651k | AU$531k | 100% |

On an industry level, roughly 60% of total compensation represents salary and 40% is other remuneration. Although there is a difference in how total compensation is set, Orthocell more or less reflects the market in terms of setting the salary. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Orthocell Limited's Growth Numbers

Orthocell Limited's earnings per share (EPS) grew 3.2% per year over the last three years. Its revenue is up 177% over the last year.

We like the look of the strong year-on-year improvement in revenue. With that in mind, the modestly improving EPS seems positive. So while we'd stop short of saying growth is absolutely outstanding, there are definitely some clear positives! While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has Orthocell Limited Been A Good Investment?

Since shareholders would have lost about 8.5% over three years, some Orthocell Limited investors would surely be feeling negative emotions. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

In Summary...

Despite the growth in its earnings, the share price decline in the past three years is certainly concerning. The stock's movement is disjointed with the company's earnings growth, which ideally should move in the same direction. If there are some unknown variables that are influencing the stock's price, surely shareholders would have some concerns. These concerns should be addressed at the upcoming AGM, where shareholders can question the board and evaluate if their judgement and decision making is still in line with their expectations.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We identified 3 warning signs for Orthocell (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

Switching gears from Orthocell, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:OCC

Orthocell

A regenerative medicine company, develops and commercializes cell therapies and biological medical devices for the repair of various bone and soft tissue injuries in Australia, the United States, the United Kingdom, and the European Union.

Flawless balance sheet very low.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor