The CEO of Orthocell Limited (ASX:OCC) is Paul Anderson, and this article examines the executive's compensation against the backdrop of overall company performance. This analysis will also look to assess whether the CEO is appropriately paid, considering recent earnings growth and investor returns for Orthocell.

Check out our latest analysis for Orthocell

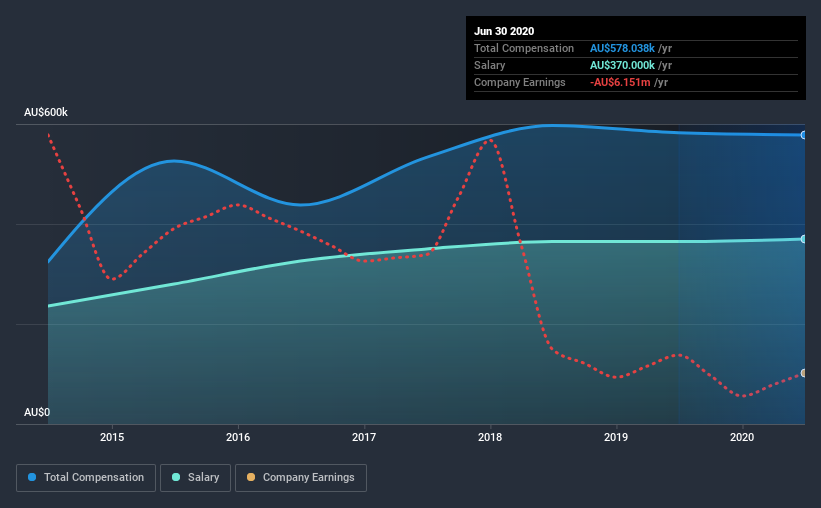

How Does Total Compensation For Paul Anderson Compare With Other Companies In The Industry?

Our data indicates that Orthocell Limited has a market capitalization of AU$81m, and total annual CEO compensation was reported as AU$578k for the year to June 2020. This means that the compensation hasn't changed much from last year. We note that the salary portion, which stands at AU$370.0k constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the industry with market capitalizations below AU$264m, reported a median total CEO compensation of AU$431k. Hence, we can conclude that Paul Anderson is remunerated higher than the industry median. Moreover, Paul Anderson also holds AU$1.7m worth of Orthocell stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | AU$370k | AU$365k | 64% |

| Other | AU$208k | AU$217k | 36% |

| Total Compensation | AU$578k | AU$582k | 100% |

On an industry level, roughly 65% of total compensation represents salary and 35% is other remuneration. Although there is a difference in how total compensation is set, Orthocell more or less reflects the market in terms of setting the salary. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

Orthocell Limited's Growth

Orthocell Limited has reduced its earnings per share by 5.1% a year over the last three years. It saw its revenue drop 24% over the last year.

Few shareholders would be pleased to read that EPS have declined. And the fact that revenue is down year on year arguably paints an ugly picture. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has Orthocell Limited Been A Good Investment?

Orthocell Limited has generated a total shareholder return of 29% over three years, so most shareholders would be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

As we touched on above, Orthocell Limited is currently paying its CEO higher than the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. Unfortunately, EPS has not grown in three years, failing to impress us. And while shareholder returns have been respectable, they have hardly been superb. So you can understand why we do not think CEO compensation is particularly modest!

It is always advisable to analyse CEO pay, along with performing a thorough analysis of the company's key performance areas. That's why we did our research, and identified 3 warning signs for Orthocell (of which 2 are a bit unpleasant!) that you should know about in order to have a holistic understanding of the stock.

Switching gears from Orthocell, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

If you decide to trade Orthocell, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About ASX:OCC

Orthocell

A regenerative medicine company, develops and commercializes cell therapies and biological medical devices for the repair of various bone and soft tissue injuries in Australia, the United States, the United Kingdom, and the European Union.

Flawless balance sheet very low.

Market Insights

Community Narratives