Advertisement

We Think Airtasker (ASX:ART) Can Easily Afford To Drive Business Growth

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So, the natural question for Airtasker (ASX:ART) shareholders is whether they should be concerned by its rate of cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. First, we'll determine its cash runway by comparing its cash burn with its cash reserves.

Check out our latest analysis for Airtasker

Does Airtasker Have A Long Cash Runway?

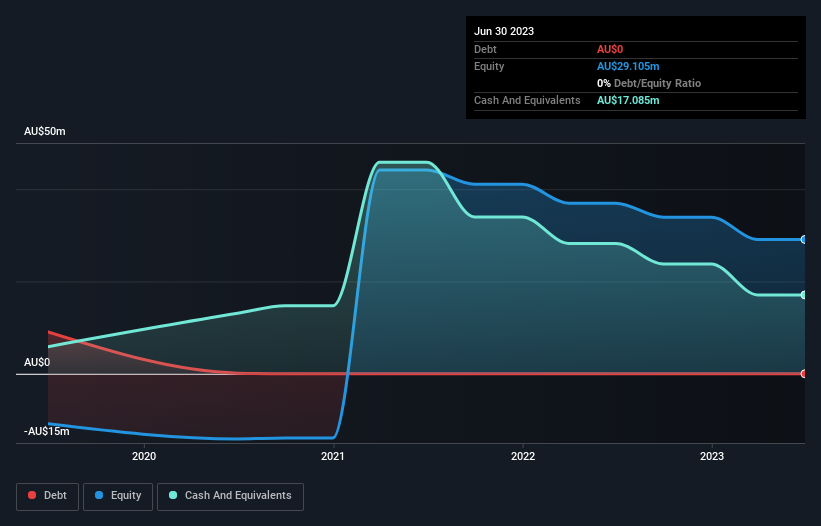

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. In June 2023, Airtasker had AU$17m in cash, and was debt-free. Importantly, its cash burn was AU$14m over the trailing twelve months. That means it had a cash runway of around 14 months as of June 2023. Importantly, though, analysts think that Airtasker will reach cashflow breakeven before then. In that case, it may never reach the end of its cash runway. You can see how its cash balance has changed over time in the image below.

How Well Is Airtasker Growing?

We reckon the fact that Airtasker managed to shrink its cash burn by 22% over the last year is rather encouraging. On top of that, operating revenue was up 40%, making for a heartening combination It seems to be growing nicely. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Can Airtasker Raise More Cash Easily?

Airtasker seems to be in a fairly good position, in terms of cash burn, but we still think it's worthwhile considering how easily it could raise more money if it wanted to. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Airtasker's cash burn of AU$14m is about 13% of its AU$113m market capitalisation. Given that situation, it's fair to say the company wouldn't have much trouble raising more cash for growth, but shareholders would be somewhat diluted.

So, Should We Worry About Airtasker's Cash Burn?

As you can probably tell by now, we're not too worried about Airtasker's cash burn. In particular, we think its revenue growth stands out as evidence that the company is well on top of its spending. Its weak point is its cash runway, but even that wasn't too bad! There's no doubt that shareholders can take a lot of heart from the fact that analysts are forecasting it will reach breakeven before too long. After considering a range of factors in this article, we're pretty relaxed about its cash burn, since the company seems to be in a good position to continue to fund its growth. Taking an in-depth view of risks, we've identified 1 warning sign for Airtasker that you should be aware of before investing.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:ART

Airtasker

Engages in the provision of technology-enabled online marketplaces for local services in Australia.

Excellent balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

8 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

22 followersusers have followed this narrative

1 commentusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

OP

OpenHorizons on Channel Vas Investments ·

Growing between 25-50% for the next 3-5 years

Fair Value:R12.1161.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

NO

Norms70 on Standard Lithium ·

SLI is share to watch next 5 years

Fair Value:€4.57.6% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DA

davidlsander on Beam Therapeutics ·

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value:US$15082.3% undervalued

62 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

962 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

75 followersusers have followed this narrative

7 commentsusers have commented on this narrative

21 likesusers have liked this narrative