Advertisement

- Australia

- /

- Metals and Mining

- /

- ASX:AMI

3 ASX Growth Stocks With High Insider Ownership And Up To 78% Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

The Australian market is poised for a positive start, with the ASX200 expected to rise over one percent, reflecting a broader trend of cautious optimism amid mixed signals from Wall Street. In this environment, growth companies with high insider ownership can be particularly appealing as they often signal strong internal confidence and alignment with shareholder interests, making them noteworthy contenders in any investment strategy focused on potential earnings expansion.

Top 10 Growth Companies With High Insider Ownership In Australia

| Name | Insider Ownership | Earnings Growth |

| Alfabs Australia (ASX:AAL) | 10.8% | 41.3% |

| Acrux (ASX:ACR) | 15.5% | 106.9% |

| Cyclopharm (ASX:CYC) | 11.3% | 97.8% |

| Fenix Resources (ASX:FEX) | 21.1% | 53.4% |

| Brightstar Resources (ASX:BTR) | 11.6% | 98.8% |

| Newfield Resources (ASX:NWF) | 31.5% | 72.1% |

| Echo IQ (ASX:EIQ) | 19.8% | 65.9% |

| Plenti Group (ASX:PLT) | 12.7% | 89.6% |

| Image Resources (ASX:IMA) | 20.6% | 79.9% |

| BETR Entertainment (ASX:BBT) | 38.6% | 121.8% |

We're going to check out a few of the best picks from our screener tool.

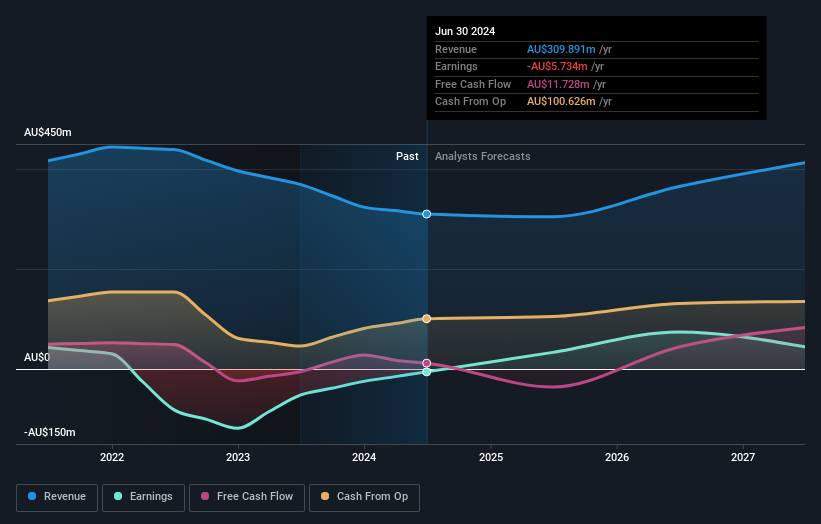

Aurelia Metals (ASX:AMI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Aurelia Metals Limited is involved in the exploration and production of mineral properties in Australia, with a market capitalization of A$533.16 million.

Operations: The company's revenue is primarily derived from its operations at the Peak Mine (A$245.13 million), followed by the Dargues Mine (A$73.90 million) and the Hera Mine (A$5.98 million).

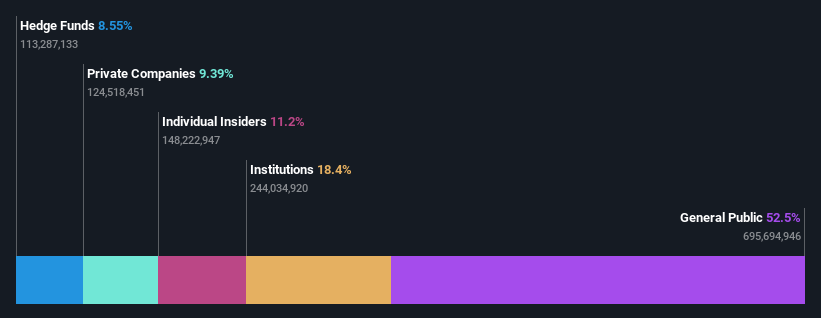

Insider Ownership: 23.9%

Earnings Growth Forecast: 45.3% p.a.

Aurelia Metals' earnings are forecast to grow significantly at 45.3% annually, outpacing the Australian market's 11.7%. The company's revenue is expected to increase by 14.6% per year, surpassing the market average of 5.5%. Trading at a substantial discount to its estimated fair value, Aurelia recently became profitable and reported A$17.95 million in net income for H1 2024-25, reversing a prior loss. Insider buying has been substantial with no significant selling recently noted.

- Click to explore a detailed breakdown of our findings in Aurelia Metals' earnings growth report.

- Our comprehensive valuation report raises the possibility that Aurelia Metals is priced higher than what may be justified by its financials.

IperionX (ASX:IPX)

Simply Wall St Growth Rating: ★★★★★★

Overview: IperionX Limited focuses on the exploration and development of mineral properties in the United States, with a market capitalization of A$1.02 billion.

Operations: IperionX Limited does not currently report any revenue segments.

Insider Ownership: 19.3%

Earnings Growth Forecast: 78.1% p.a.

IperionX is poised for significant growth with a forecasted revenue increase of 86.2% annually, surpassing the Australian market's average. Despite currently generating less than US$1 million in revenue, insider buying has been substantial without notable selling. Recent U.S. government funding supports its Titan Project and titanium production expansion, enhancing its strategic position in critical minerals supply chains. Although shareholders experienced dilution last year, IperionX trades significantly below estimated fair value and aims for profitability within three years.

- Navigate through the intricacies of IperionX with our comprehensive analyst estimates report here.

- According our valuation report, there's an indication that IperionX's share price might be on the expensive side.

Titomic (ASX:TTT)

Simply Wall St Growth Rating: ★★★★★★

Overview: Titomic Limited provides manufacturing and technology solutions for high-performance metal additive manufacturing across Australia, the United States, and Europe, with a market cap of A$410.99 million.

Operations: The company's revenue segment is primarily from the development and sale of additive manufacturing technology, amounting to A$7.44 million.

Insider Ownership: 11.2%

Earnings Growth Forecast: 77.2% p.a.

Titomic is set for substantial growth, with revenue forecasted to increase by 52.3% annually, outpacing the Australian market. Despite a volatile share price and past shareholder dilution, Titomic's insider ownership remains stable without significant recent trading activity. Recent strategic appointments in the U.S., particularly Kirk Pysher as SVP of Manufacturing, aim to bolster its capabilities in key sectors like aerospace and defense. The company anticipates profitability within three years, driven by advanced manufacturing technologies.

- Click here to discover the nuances of Titomic with our detailed analytical future growth report.

- The analysis detailed in our Titomic valuation report hints at an inflated share price compared to its estimated value.

Taking Advantage

- Take a closer look at our Fast Growing ASX Companies With High Insider Ownership list of 99 companies by clicking here.

- Interested In Other Possibilities? Outshine the giants: these 28 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:AMI

Aurelia Metals

Engages in the exploration and production of mineral properties in Australia.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor