- Australia

- /

- Metals and Mining

- /

- ASX:PRU

Is Perseus Mining Limited's (ASX:PRU) Stock's Recent Performance Being Led By Its Attractive Financial Prospects?

Most readers would already be aware that Perseus Mining's (ASX:PRU) stock increased significantly by 15% over the past three months. Given the company's impressive performance, we decided to study its financial indicators more closely as a company's financial health over the long-term usually dictates market outcomes. Specifically, we decided to study Perseus Mining's ROE in this article.

Return on equity or ROE is a key measure used to assess how efficiently a company's management is utilizing the company's capital. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

View our latest analysis for Perseus Mining

How Is ROE Calculated?

Return on equity can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Perseus Mining is:

20% = US$365m ÷ US$1.8b (Based on the trailing twelve months to June 2024).

The 'return' is the income the business earned over the last year. One way to conceptualize this is that for each A$1 of shareholders' capital it has, the company made A$0.20 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Based on how much of its profits the company chooses to reinvest or "retain", we are then able to evaluate a company's future ability to generate profits. Generally speaking, other things being equal, firms with a high return on equity and profit retention, have a higher growth rate than firms that don’t share these attributes.

Perseus Mining's Earnings Growth And 20% ROE

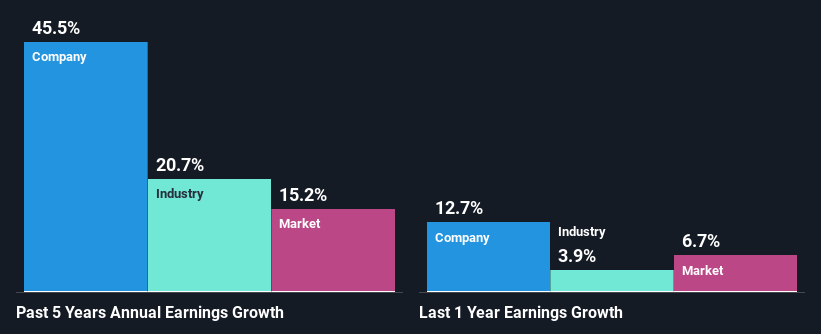

To start with, Perseus Mining's ROE looks acceptable. Especially when compared to the industry average of 11% the company's ROE looks pretty impressive. This certainly adds some context to Perseus Mining's exceptional 46% net income growth seen over the past five years. However, there could also be other causes behind this growth. Such as - high earnings retention or an efficient management in place.

Next, on comparing with the industry net income growth, we found that Perseus Mining's growth is quite high when compared to the industry average growth of 21% in the same period, which is great to see.

Earnings growth is a huge factor in stock valuation. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about Perseus Mining's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Perseus Mining Efficiently Re-investing Its Profits?

Perseus Mining's ' three-year median payout ratio is on the lower side at 10% implying that it is retaining a higher percentage (90%) of its profits. So it seems like the management is reinvesting profits heavily to grow its business and this reflects in its earnings growth number.

Besides, Perseus Mining has been paying dividends over a period of three years. This shows that the company is committed to sharing profits with its shareholders. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to rise to 19% over the next three years. Accordingly, the expected increase in the payout ratio explains the expected decline in the company's ROE to 12%, over the same period.

Summary

Overall, we are quite pleased with Perseus Mining's performance. Specifically, we like that the company is reinvesting a huge chunk of its profits at a high rate of return. This of course has caused the company to see substantial growth in its earnings. Having said that, on studying current analyst estimates, we were concerned to see that while the company has grown its earnings in the past, analysts expect its earnings to shrink in the future. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

If you're looking to trade Perseus Mining, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About ASX:PRU

Perseus Mining

Explores, evaluates, develops, and mines for gold properties in West Africa.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Community Narratives