Advertisement

- Philippines

- /

- Banks

- /

- PSE:PNB

Asian Undervalued Small Caps With Insider Action To Watch In July 2025

Simply Wall St

Reviewed by Simply Wall St

As the global markets continue to navigate a complex landscape, Asian small-cap stocks are gaining attention amid fluctuating economic indicators and evolving trade dynamics. With the U.S. smaller-cap indexes showing robust performance, investors are increasingly looking towards Asia for opportunities in small-cap companies that may be poised for growth due to strategic insider actions and favorable market conditions.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| East West Banking | 3.2x | 0.7x | 29.91% | ★★★★★☆ |

| Atturra | 26.9x | 1.1x | 39.82% | ★★★★★☆ |

| Daiwa House Logistics Trust | 11.4x | 6.9x | 27.48% | ★★★★★☆ |

| Strike Energy | NA | 5.7x | 33.07% | ★★★★★☆ |

| Dicker Data | 19.2x | 0.7x | -16.23% | ★★★★☆☆ |

| Build King Holdings | 3.3x | 0.1x | 24.45% | ★★★★☆☆ |

| AInnovation Technology Group | NA | 2.5x | 47.50% | ★★★★☆☆ |

| Fengyinhe Holdings | 13.3x | 5.3x | 23.81% | ★★★☆☆☆ |

| Charter Hall Long WALE REIT | NA | 12.3x | 20.79% | ★★★☆☆☆ |

| Ho Bee Land | 12.1x | 2.4x | 45.86% | ★★★☆☆☆ |

Let's dive into some prime choices out of from the screener.

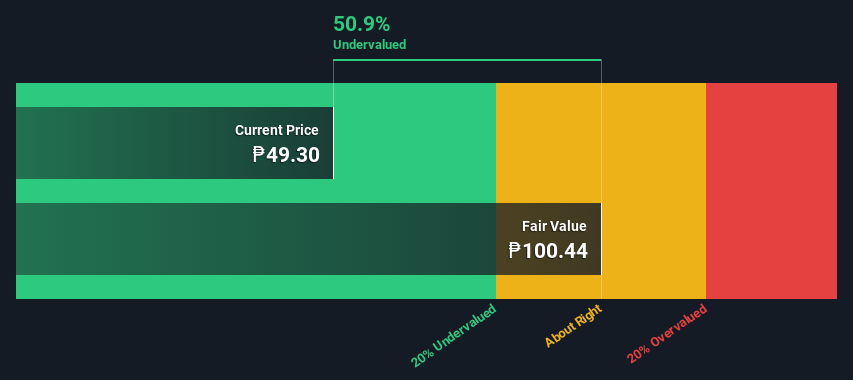

Pantoro Gold (ASX:PNR)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Pantoro Gold is a mining company focused on the exploration and production of gold, primarily through its Norseman Gold Project, with a market cap of A$289.11 million.

Operations: Pantoro Gold's revenue is primarily generated from the Norseman Gold Project, with recent figures showing A$289.11 million in revenue. The company has faced challenges with cost of goods sold (COGS) exceeding revenue, leading to a gross profit margin of 0.71%. Operating expenses and non-operating expenses further impact the bottom line, contributing to a net income loss of A$26.89 million and a net income margin of -9.30%.

PE: -47.2x

Pantoro Gold, a small cap in Asia's mining sector, is gaining attention due to its ongoing growth drilling program at the OK Underground Mine, which began in late 2024. The recent results show promising continuity of gold lodes, supporting potential ore reserve upgrades. Insider confidence is evident with share purchases over the past year. Despite relying on external borrowing for funding, earnings are projected to grow by 58% annually. This positions Pantoro as an intriguing prospect amidst undervalued opportunities in the region.

- Dive into the specifics of Pantoro Gold here with our thorough valuation report.

Explore historical data to track Pantoro Gold's performance over time in our Past section.

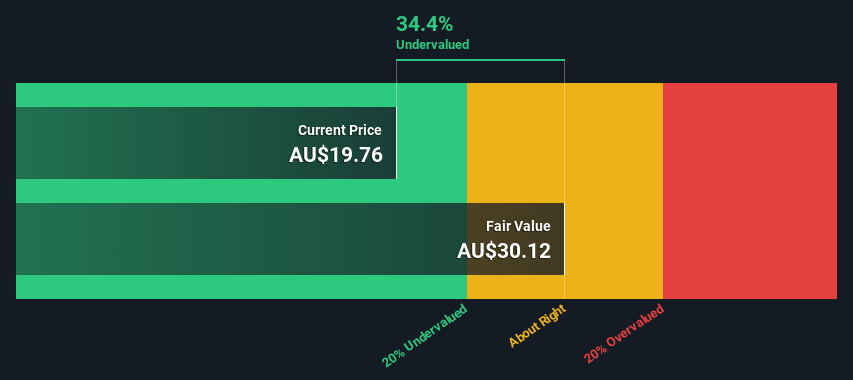

Perpetual (ASX:PPT)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Perpetual is a diversified financial services company primarily engaged in asset management and wealth management, with a market capitalization of A$1.89 billion.

Operations: The company generates revenue primarily from Asset Management and Wealth Management, with Asset Management being the largest contributor. Over recent periods, gross profit margin has shown a downward trend, reaching 39.09% by the end of 2024. Operating expenses have been increasing steadily, impacting net income margins significantly.

PE: -4.7x

Perpetual is navigating a strategic shift, highlighted by insider confidence as Christopher Mark Jones increased their stake by 8,000 shares, valued at approximately A$159,420. The company is selling its wealth management unit to reduce debt from A$569 million. With M&A interest from Bain Capital and Oaktree Capital Management, the sale could fetch between A$500 million and A$1 billion. Suzanne Evans' appointment as CFO marks another change amid these developments. Earnings are projected to grow significantly at 76% annually.

- Click to explore a detailed breakdown of our findings in Perpetual's valuation report.

Understand Perpetual's track record by examining our Past report.

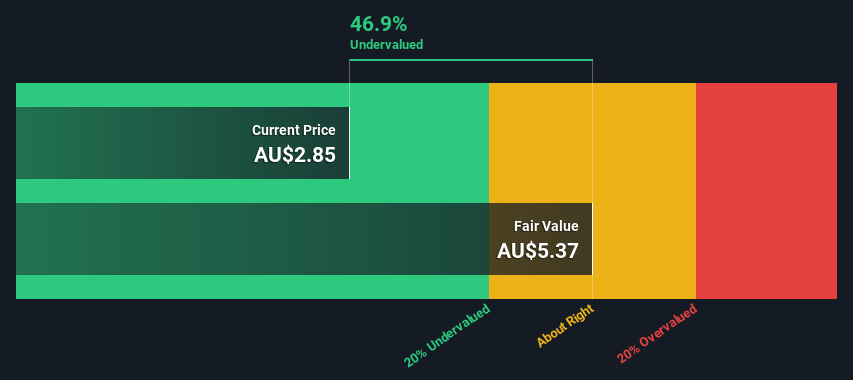

Philippine National Bank (PSE:PNB)

Simply Wall St Value Rating: ★★★★★☆

Overview: Philippine National Bank is a financial institution that primarily operates in retail and corporate banking, treasury, and other financial services, with a market capitalization of ₱60.08 billion.

Operations: The bank's primary revenue streams are derived from retail banking, corporate banking, and treasury operations. Retail banking is the largest contributor with ₱33.79 billion, followed by corporate banking at ₱12.42 billion and treasury operations at ₱11.50 billion. The gross profit margin has shown a high level of efficiency, reaching up to 99.92% in recent periods, indicating minimal cost of goods sold relative to revenue generated. Operating expenses are primarily driven by general and administrative costs and sales & marketing expenses, impacting net income margins which have varied over time but reached as high as 37.52%.

PE: 3.8x

Philippine National Bank, a smaller player in Asia's financial sector, shows potential for growth with an expected annual revenue increase of 8.26%. Despite having a high level of bad loans at 6.9%, insider confidence is evident as their CFO acquired 260,000 shares valued at ₱13.5 million in May 2025. Recent executive changes could bring fresh strategies to the table, potentially enhancing operational dynamics and addressing existing challenges within the bank's structure.

Seize The Opportunity

- Reveal the 52 hidden gems among our Undervalued Asian Small Caps With Insider Buying screener with a single click here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About PSE:PNB

Philippine National Bank

Provides various banking and financial products and services.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor